pixelfit/E+ through Getty Pictures

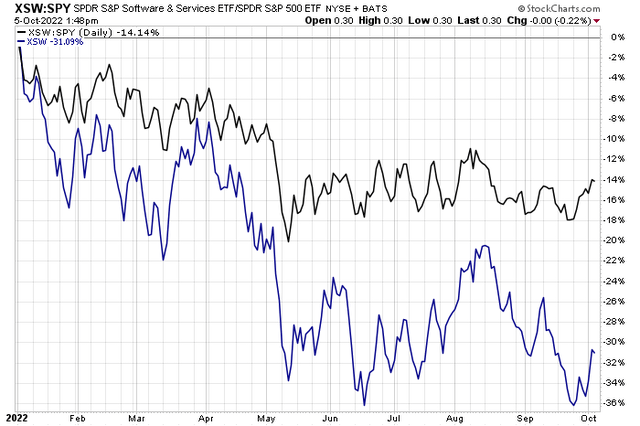

IT providers shares have sharply underperformed the S&P 500 in 2022. The SPDR S&P Software program & Providers ETF (XSW) is down about one-third as rates of interest rise and the U.S. greenback soars. Trying ahead, it’s potential that investments in IT and advisory providers is perhaps minimize as corporations trim the fats and watch their prices. One $8 billion market cap agency with heavy worldwide gross sales publicity has an unsure earnings future, however shares have been resilient. However is it a purchase?

IT Software program & Providers Business Struggling Amid Macro Headwinds

Stockcharts.com

In line with Financial institution of America International Analysis, Genpact (NYSE:G) is the pioneer and largest India-centric Enterprise Course of Administration (BPM) vendor with calendar-year 2019 revenues of $3.5 billion and almost 95,000 staff. Arrange because the captive Normal Electrical (GE) BPM arm in 1997, it turned a third-party vendor in 2005. The corporate derives roughly 83% of income from BPM and roughly 17% from IT providers, and vertically revs are cut up as 35% from monetary providers/insurance coverage, 35% from hi-tech/ manufacturing, and the remaining from diversified industries. GE at the moment accounts for 13% of revenues.

The Bermuda-based IT Providers trade firm, inside the Info Expertise sector, trades at a excessive 25.6 trailing 12-month GAAP price-to-earnings ratio and pays a small 1.1% dividend yield, in line with The Wall Avenue Journal. To get a way of what Genpact does, its rivals are firms equivalent to Accenture PLC and Cognizant Applied sciences.

The corporate has had a pleasant string of worthwhile tasks, however securing new high-margin clients may very well be a problem on this powerful macro surroundings. These offers could be very accretive to earnings via excessive working leverage, however the cyclical IT spending area of interest would possibly come underneath stress as financial development slows. Forex dangers are additionally one thing that would negatively affect income. Nonetheless, administration stated on its most up-to-date earnings name that its gross sales cycle is shortening.

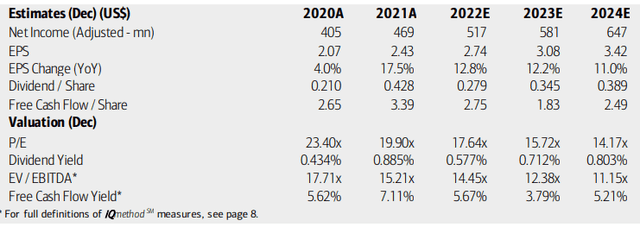

On valuation, BofA analysts see internet earnings climbing at a really regular price via 2024, whereas its dividend ought to observe swimsuit. The agency’s working P/E ratio ought to retreat to extra favorable ranges ought to the share worth be unchanged, however given cyclicality within the enterprise, these earnings estimates are questionable. Furthermore, Genpact’s EV/EBITDA a number of suggests the agency is richly valued. Free money movement is constant however not excessive. Total, the expansion and valuation outlooks are so-so.

Genpact Earnings, Valuation, And Dividend Forecasts

BofA International Analysis

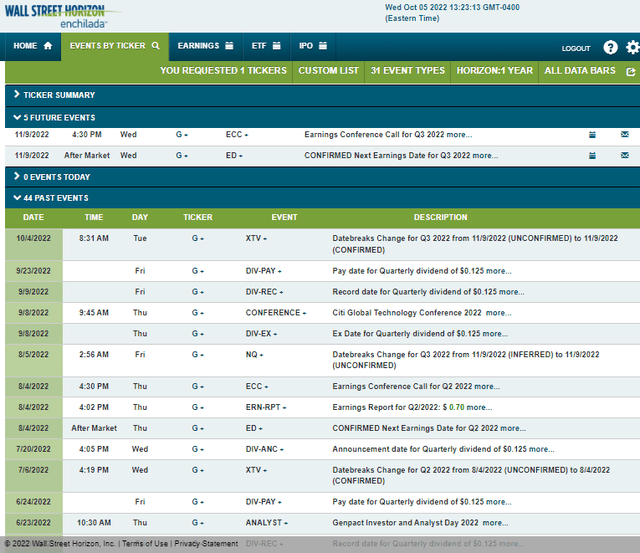

Trying forward, company occasion knowledge offered by Wall Avenue Horizon exhibits a confirmed Q3 earnings date of Wednesday, November 9 with a convention name instantly after outcomes are posted. You possibly can pay attention stay right here. The calendar is mild via then, although.

Company Occasion Calendar

Wall Avenue Horizon

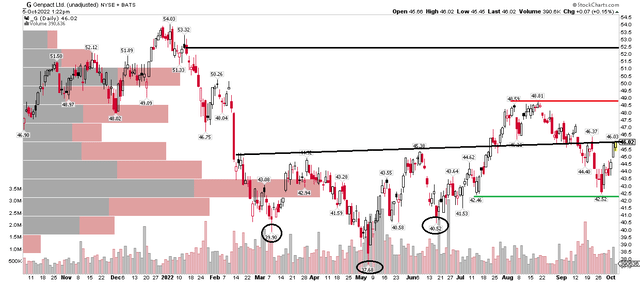

The Technical Take

Genpact has held up effectively after falling arduous in the course of the first few months of 2022. The inventory really bottomed effectively earlier than the S&P 500 hit its June interim low. There are just a few fascinating options I see on the one-year each day chart of G.

First, there’s a bullish inverse head and shoulders sample that’s waffling considerably, nevertheless it’s nonetheless in play. The worth goal utilizing the space from the neckline to the top, added on high of the neckline, is within the $52 to $53 vary – close to the late 2021 highs. Earlier than then, nevertheless, the inventory should climb above an uptrend resistance line close to $46. Extra importantly, the $48 to $49 vary double-top should be recaptured.

On the bullish facet proper now’s that the inventory held $42.50 assist throughout its September pullback. So long because the inventory is above that time, proudly owning shares appears good. Total, the development may very well be reversing to the upside.

G Inventory Seems To Be Bottoming

Stockcharts.com

The Backside Line

Genpact has an unsure elementary outlook whereas the corporate valuation doesn’t scream low-cost. The technical image, although, appears sturdy inside this unstable market surroundings. Combining the lukewarm valuation with a positive chart, I feel G is a purchase right here.

{kind=link}