Shopping for a synthetic intelligence (AI) inventory that is buying and selling at a beautiful valuation and is rising at a formidable tempo might sound troublesome proper now contemplating that corporations ready to benefit from this know-how have witnessed a speedy bounce of their share costs prior to now yr or so.

Nvidia, as an illustration, is buying and selling at 71 instances trailing earnings, although the great half is that the chipmaker has been in a position to justify its premium valuation with excellent development. However, AI software program play Palantir Applied sciences is buying and selling at an costly valuation, however its development hasn’t been sufficient to justify its wealthy multiples.

Nevertheless, traders searching for a mixture of development and worth within the AI area of interest are in luck as there’s one firm — Taiwan Semiconductor Manufacturing (NYSE: TSM), popularly generally known as TSMC — that is not solely low-cost proper now but additionally appears set to ship spectacular development. Let’s take a look at why traders ought to think about shopping for this inventory earlier than it releases its first-quarter 2024 outcomes on April 18.

TSMC is about to ship stronger-than-expected development

When TSMC launched fourth-quarter 2023 ends in January this yr, the corporate guided for first-quarter 2024 income of $18.4 billion on the midpoint of its vary.

Nevertheless, month-to-month income stats for the primary three months of 2024 point out that it’s properly on its approach to exceeding that mark. Extra importantly, income development has accelerated with every passing month.

In January, TSMC’s month-to-month income elevated 8% yr over yr. This was adopted by an 11% improve in February, whereas March was even higher with a year-over-year acquire of 34%. So first-quarter income got here in at $18.86 billion, up nearly 14% yr over yr and forward of the $18.26 billion consensus estimate.

The whole quarterly outcomes will probably be out on April 18, and it will not be stunning to see the inventory surge increased as soon as it reviews. That is as a result of the demand for AI chips throughout numerous purposes is now shifting the needle in a much bigger manner for TSMC, as its March quarterly income tells us.

Secular development of the AI chip market will probably be a tailwind for TSMC

Apple is TSMC’s largest buyer, accounting for 25% of its prime line. However the smartphone maker has been struggling for development, as its current outcomes inform us.

Furthermore, Apple begins ramping up the manufacturing of its iPhones, for which TSMC provides chips, within the second half of the yr. So the sharp acceleration within the chipmaker’s income final month could be attributed to the booming demand from the likes of Nvidia, AMD, Intel, Qualcomm, and Broadcom, that are amongst its prime seven clients.

All these chipmakers are centered on delivering new AI chips, in addition to rising the output of their current merchandise to satisfy the sturdy demand from clients. That is why TSMC has been quickly rising its manufacturing capability. It’s anticipated to double its superior chip packaging capability to 240,000 wafers this yr from 120,000 wafers final yr, pushed primarily by demand from Nvidia, which accounts for an estimated 60% of its superior chip packaging capability.

Intel, alternatively, lately unveiled a brand new AI accelerator known as Gaudi 3 that is based mostly on TSMC’s 5-nanometer manufacturing course of. Intel has already began delivery samples of this chip and expects to maneuver into full manufacturing within the third quarter of 2024. In the meantime, the curiosity in Broadcom’s customized AI processors is rising, and the corporate lately landed a brand new shopper as properly.

Equally, Qualcomm is on monitor to benefit from the rising adoption of AI inside smartphones and private computer systems. In all, TSMC is in a major place to capitalize on the secular development of the AI chip market, particularly contemplating that it’s the world’s main semiconductor foundry with an estimated market share of 61%. That is properly forward of second-place Samsung’s share of 11%.

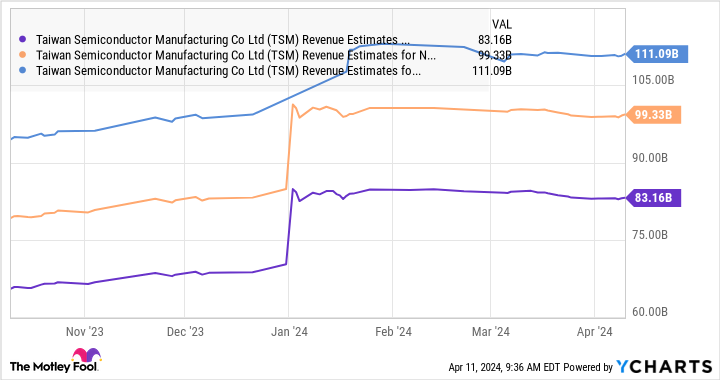

Contemplating that the worldwide AI chip market is forecast to develop at an annual tempo of 38% via 2032, there’s a good likelihood of TSMC sustaining its spectacular momentum. The next chart means that analysts count on sturdy income will increase in 2024 and past from final yr’s prime line of $69.3 billion.

That is why shopping for this semiconductor inventory proper now appears to be like like a no brainer given its enticing valuation. TSMC is buying and selling at 29 instances trailing earnings, a reduction to the Nasdaq 100‘s earnings a number of of 30 (utilizing the index as a proxy for tech shares). The ahead earnings a number of of 24 can be decrease than the Nasdaq 100’s studying.

What’s extra, TSMC inventory is considerably cheaper than Nvidia, which implies it is a cheaper approach to play the AI chip increase.

Additionally, the proof above reveals that TSMC appears constructed for long-term development from its essential function within the AI chip market, which is why traders would do properly to purchase this AI inventory earlier than it jumps increased (and turns into costly) following the 40% good points it has clocked to this point in 2024.

Must you make investments $1,000 in Taiwan Semiconductor Manufacturing proper now?

Before you purchase inventory in Taiwan Semiconductor Manufacturing, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for traders to purchase now… and Taiwan Semiconductor Manufacturing wasn’t considered one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… in case you invested $1,000 on the time of our advice, you’d have $540,321!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of April 8, 2024

Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Units, Apple, Nvidia, Palantir Applied sciences, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Broadcom and Intel and recommends the next choices: lengthy January 2023 $57.50 calls on Intel, lengthy January 2025 $45 calls on Intel, and brief Might 2024 $47 calls on Intel. The Motley Idiot has a disclosure coverage.

1 Cheaply Valued Synthetic Intelligence (AI) Inventory to Purchase Hand Over Fist Earlier than April 18 was initially revealed by The Motley Idiot