Kimberly White

What Occurred?

Software program large Adobe (NASDAQ:ADBE) launched pedestrian earnings on September fifteenth, 2022, and dropped a bombshell available on the market. The corporate introduced it was buying on-line design enterprise Figma for $20 billion, about half in money and half in inventory.

Figma is a cloud-based design software program that competes instantly with Adobe XD. Many professionals desire Figma due to its superior collaboration performance. A number of customers can edit in real-time, just like Google Docs (GOOG, GOOGL). For these considering extra element, try this hyperlink.

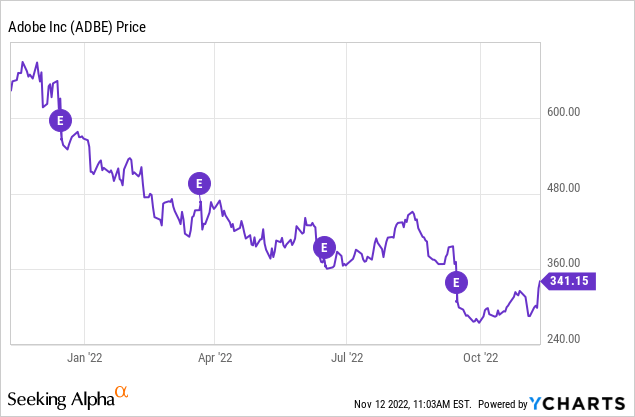

The inventory was already down 35% on the yr earlier than the announcement and cratered on the information, as proven beneath.

Quite a few analysts rushed to cheaper price targets and reduce rankings. In fact, the inventory was already buying and selling underneath $300 per share as these rolled in. The inventory reached its 52-week low of $275 per share in late September.

After researching the inventory’s valuation and the nuances of the Figma acquisition, I averaged right into a near-full place with a median price of $287 per share. This seems to be prescient after final week’s rally; nevertheless, the rally may fizzle rapidly, and it is a long-term play.

One other dip in Adobe inventory ought to be tempting to long-term buyers who perceive the long-term implications of bringing Figma on board. Greenback-cost averaging may be a clever selection as a result of the worth remains to be traditionally low even after the rally.

Listed below are three causes the Figma acquisition and inventory worth look compelling.

Purpose #1: The Microsoft Dilemma

Microsoft (MSFT) and Adobe have loved a wholesome relationship for years. Each are among the many largest software program corporations on this planet by market cap. Whereas they’re rivals, Microsoft is an Adobe buyer, and so they have fashioned strategic partnerships and integrations through the years.

Microsoft staff have been utilizing Figma for years and apparently do not identical to it; they LOVE it. Integration with Microsoft Groups app was additionally just lately added.

The truth is, Figma’s buyer base is a who’s who of company tech corporations, from Netflix (NFLX) to Spotify (SPOT) to Alphabet.

The choice to buy Figma for $20 billion turns into obvious by means of this lens.

- Adobe cannot afford to permit Figma to proceed infringing on its area with its 100% income progress anticipated in 2022.

- Microsoft is not any stranger to huge acquisitions. Its current $69 billion buy of Activision Blizzard (ATVI) is underneath regulatory evaluate. If Adobe does not buy Figma, one other software program large may, and this might considerably have an effect on Adobe’s future earnings.

- Figma may go public. The corporate drew a $10 billion valuation in 2021. It could seemingly appeal to extra throughout an IPO, changing into an extremely well-funded competitor in Adobe’s inventive area.

$20 billion is steep, however it could price far more to do nothing.

Purpose #2: Figma

Figma did not obtain a $10 billion valuation in 2021 for nothing. It’s a unbelievable product by all accounts. It’s anticipated to move $400 million in annual recurring income (ARR) in 2022 on 100% gross sales progress and a 90% gross margin. Its 150% web retention price is unbelievable and signifies that progress will proceed quickly.

Figma can be cash-flow constructive, so it will not be a drain on sources. The $20 billion worth appears ridiculous now, however it could appear to be a cut price in 5 years.

Purpose #3: Purchase Vs. Develop

Firms spend billions researching and growing (R&D) new merchandise. Inside R&D is expensive, and there’s no assure that profitable merchandise will develop. Adobe has spent $8.9 billion on R&D since 2019. Generally buying a ready-made product for a premium worth is the best choice.

Salesforce (CRM) is a primary instance of an organization efficiently constructing out acquisitions. The corporate has acquired Slack, Tableau, MuleSoft, and plenty of others. After making the investments, Salesforce efficiently grew every division’s worth past the preliminary buy worth.

As talked about, the Figma acquisition might be about half in money and half in inventory. Adobe has a robust steadiness sheet with $8.5 billion in present belongings and has produced $5.5 billion money from operations by means of three quarters this yr.

The acquisition might have short-term financing, however will not saddle the corporate with tons of long-term debt. Lastly, Adobe has repurchased $4.8 billion in shares up to now this yr, so shareholders aren’t being frolicked to dry.

Adobe inventory’s valuation

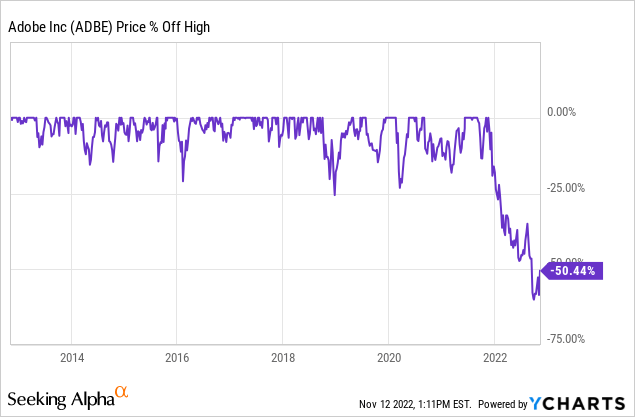

Adverse sentiment has pushed down the worth of Adobe inventory. Pessimism concerning the acquisition and a possible recession could give long-term buyers a chance.

The inventory is at present at its highest percent-off-high decline in ten years, as proven beneath.

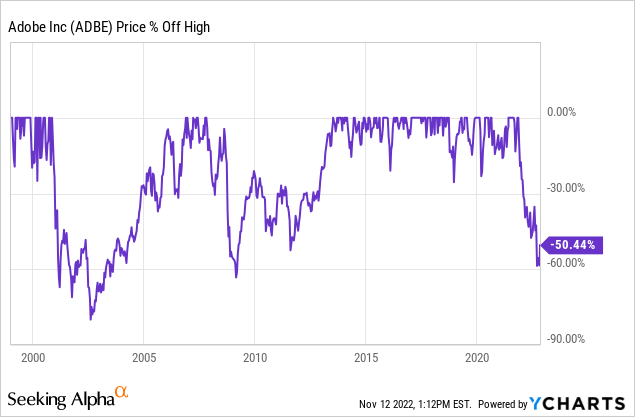

The final time the inventory was this removed from excessive was the monetary disaster, and earlier than that, the dot-com crash. The inventory recovered because the economic system did in each circumstances, as proven beneath.

The restoration is not at all times in a single day, which is why this ought to be a long-term play. We may see new lows earlier than seeing new highs. Greenback-cost averaging is a superb software.

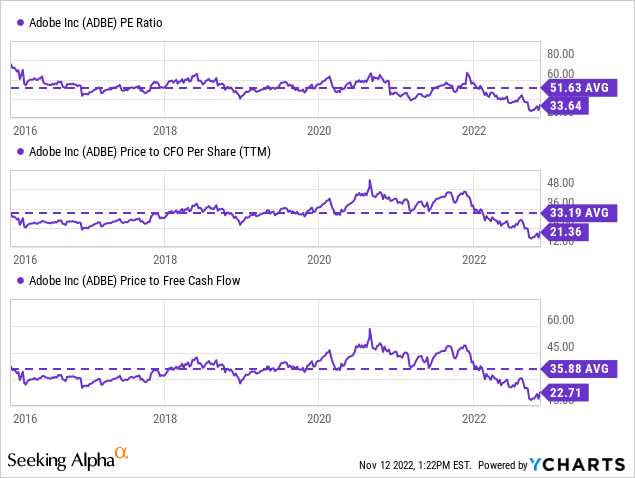

Adobe is discounted based mostly on historic multiples as properly. Its price-to-earnings (P/E) and price-to-cash circulate metrics inform related tales, as proven beneath.

Lastly, greater than $20 billion has been shaved off Adobe’s market cap since proper earlier than the Figma bulletins. New buyers can primarily purchase Adobe with the acquisition worth discounted.

The summation of those metrics factors to a tremendously constructive threat/reward proposition for long-term buyers.

{kind=link}