Luis Alvarez

Expensive readers/followers,

Oftentimes, you will get companies which have a particular area of interest and attraction in a really specific subject, and since they excel in that particular subject, imagine they’ll excel in different fields simply. Typically this works out – however extra usually, as I’ve skilled, it doesn’t. AMSC ASA (OTCQX:ASCJF), a ship financing firm, has seen a major bounce in its inventory worth and supplied a 16%+ yield – however that is now modified, which we’ll go into on this article. It is also an organization I have been masking for a while, with my newest article concerning the enterprise one which you could find right here.

In my final article, I made a case for why this firm ought to be averted because of elevated danger and a change to its enterprise mannequin that might affect its total attraction in a reasonably main kind of means.

Since that point, the corporate has underperformed the S&P500 on a capital appreciation foundation and barely outperformed on the premise of inclusive of dividends.

One of many main issues that occurred over the last quarter was that the corporate moved away from what I imagine made certainly one of its appeals – specifically the enterprise section with the Jones Act.

On this article, I will be updating you on AMSC ASA, and present you why I nonetheless imagine this firm to not be nice funding potential at the moment.

AMSC ASA – extra uncertainty following 4Q, not much less

So, the corporate already introduced and confirmed the dividend reduce over the last interval. That implies that, not like different high-yield transport investments, AMSC ASA Is now a enterprise that gives a yield of 6.65%.

Now, there are various kinds of buyers. There are buyers which can be searching for yield and buyers which can be thinking about capital appreciation. Totally different shares make sense for various folks at totally different factors of their lives. Somebody in retirement might deal with one thing like a high-income however high-safety portfolio to be sure that sufficient money for payments and bills is all the time there, since they would not be working anymore. Youthful buyers would then as a substitute deal with one thing like a portfolio with extra progress as a result of they nonetheless have loads of time to develop their fortune.

I’ve all the time favored a diversified strategy. I’ve each progress and revenue investments and know sufficient to distinguish between the 2. When you could have an revenue funding, you additionally have to be sure that that revenue funding is smart from a danger perspective; i.e., when you’re taking a rare quantity of danger to get a yield that you might get from far safer sources.

I point out this as a result of I imagine it is related – as a result of I in reality imagine that that is what AMSC represents following the change of course and the dividend reduce.

There was an argument to be made with the corporate when it was Jones-act targeted, and when there was a 16%+ yield. As a result of on the time, the corporate was a transparent revenue funding that outstripped many others. Even from a risk-reward profile, it could possibly be argued that AMSC ASA suited some portfolios, relying on the investor danger tolerance.

It is my view that that is now a troublesome argument to make.

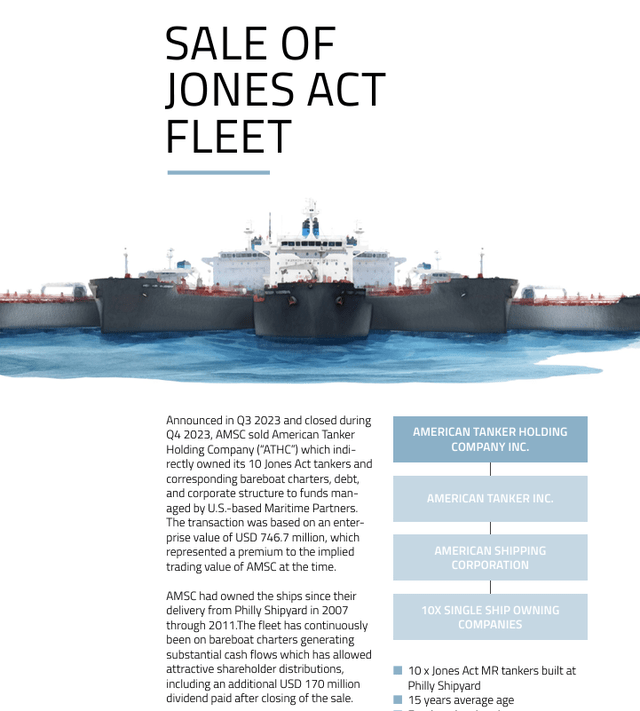

The final report we’ve is the annual one to date, or 4Q. The corporate accredited the brand new dividend of 5 cents quarterly, refinanced some leases, and accomplished a sale totaling nearly 750M USD.

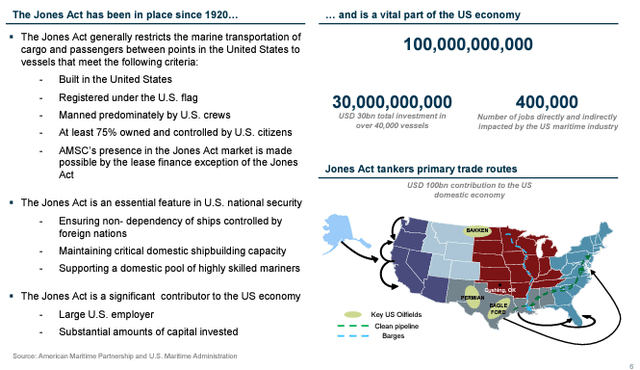

These are solely the final information gadgets, although – not those I imagine that one ought to deal with with the corporate. When you’re to imagine the corporate’s personal materials earlier than this transaction, then the Jones Act was one of many main causes that you simply needed to put money into AMSC ASA.

AMSC IR (AMSC IR)

These restrictions considerably benefitted AMSC, and whereas the rationale behind shifting away from it is smart to some, it does to not me – not if the corporate needed to keep up its attraction as an funding. The sale of the Jones Act tanker fleet, and the sale of the Normand Maximus, all of those mark this transformation from one type of the corporate to a different.

ASMC IR (ASMC IR)

So what stays after this transfer, and the place is the corporate going? For now, the outlook appears to be that AMSC will attempt to develop primarily based on its 21.1% shares of Solstad Maritime (although these shall be diluted but once more with the Solstad Maritime fairness increase later this 12 months), and that AMSC primarily based on present info, shall be making an attempt to “develop by accretive transaction and specializing in distributing dividends to shareholders”.

Shade me considerably unsure of the place this precisely implies that the corporate goes.

The one different info we’ve is that AMSC believes that its funding in Solstad Maritime implies that it may profit from years and years of low funding ranges into offshore oil providers, which presently is anticipated to proceed at a excessive degree, with excessive utilization charges for each offshore oil and offshore wind.

So what you are investing in is an organization that does not actually personal something anymore – besides 21.1% – topic to dilution – of Solstad Maritime.

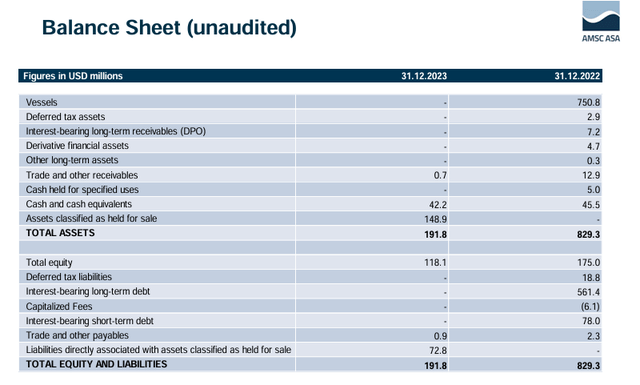

That is additionally expressed within the change within the steadiness sheet.

AMSC IR (AMSC IR)

So – a brand new firm with new targets, and little or no concrete as to what the corporate goes to do, past managing its belongings in Solstad and looking for accretive transactions in what I’d characterize as a really inflated kind of market on an total foundation. One of many causes I keep, at this specific time, over 12.5% in money, the place I’m normally under 6%.

I say the next: AMSC ASA now yields 6.5%. This isn’t a excessive yield nor a beautiful one within the context of danger/reward when you think about what else is out there available on the market right this moment.

What do I imply by this?

I imply that one of many largest Telcos in Sweden, Telia (OTCPK:TLSNF), yields over 7%. I imply that Fortum (OTCPK:FOJCF), a big utility, is at over 9% I imply that British American Tobacco (BTI) is nearly at 10%. I imply that Enbridge (ENB) is at over 7%. I imply that Enel (OTCPK:ENLAY), regardless of huge progress, remains to be at 6.3%.

I imply, collectively there are a lot of corporations with engaging dividends, and since my portfolio yield on an total foundation is presently at 5.1224%, you will know that dividends are essential to me. I stay off my dividends, and I imply to proceed doing so for the remainder of my life. So, a great dividend funding – I am on board.

I don’t imagine AMSC ASA constitutes a great dividend funding or a great or protected funding at this specific time, due to the uncertainty as to what precisely the corporate goes to do on a ahead foundation.

I’ll present you the valuation right here, however a good warning, there’s numerous uncertainty concerning the valuation and prospects of this firm at the moment.

AMSC ASA – A lot to love, however the valuation and uncertainty aren’t a kind of issues.

I used to be truly near, at this text, going to a “SELL” for the corporate right here. The explanation behind that is the huge adjustments within the firm’s fundamentals, with out quite a lot of sentences value of public plan and ambition the place to go from right here, and clearly anticipating buyers to in some way be accepting or tremendous with this on an total foundation.

Effectively, that’s not the case for me. I do not discover the knowledge enough to base a convincing thesis.

Once I beforehand wrote about AMSC as a enterprise, I thought of the corporate a “HOLD”, fulfilling solely 2 out of 5 of my funding standards regardless of a major, 16%+ yield. This was additionally at a considerably costly P/E, however this wasn’t solely the explanation that I went impartial or “HOLD” on this firm. The explanation was additionally that there have been fairly just a few extra engaging transport companies on the market. I additionally thought of the dimensions prohibitive.

Then the corporate did this in 3Q23, and now we’ve 4Q23 and FY outcomes, with not rather more readability than earlier than. What this implies is that it is now arduous to even use the identical metrics to guage the enterprise right here.

Regardless of every little thing, AMSC ASA nonetheless has a adverse 5-year RoR, if not an excessively adverse one – lower than adverse 15%. The extraordinary dividend has actually pushed this up as effectively.

Analysts now, as of Could of 2024, have the corporate at an up to date goal vary of round 20-22 NOK, lowered from round 45-60 NOK again in early 2023. So most analysts would agree with the evaluation that the corporate is value round half now that this newest set of measures has gone by, and that it is prone to undergo.

It is also value noting that as of this information, all however one analyst has now left protection of the corporate behind. (Paywalled Supply, TIKR.com)

This in itself needn’t imply something, however I nonetheless imagine it’s indicative of the chance/reward ratio that analysts contemplate this firm now being working below.

I don’t contemplate AMSC ASA to be a beautiful enterprise to put money into at the moment. I’ll decrease my PT to fifteen NOK as a result of the e-book worth calculations don’t make sense when the corporate’s fairness and belongings are simply stakes in different investments which can be going to be topic to dilution, within the firm’s personal phrases, because of an incoming capital increase.

I due to this fact wouldn’t pay greater than 1x Ebook worth, and I contemplate even that to be a doubtlessly wealthy valuation, given among the danger/reward right here.

I don’t decrease my goal to SELL – however except the corporate reveals some extra concrete plans within the 1Q24 interval, then I’ll accomplish that within the subsequent quarter. Holding right here will not be one thing that I contemplate to be related with what else is out there within the present inventory market setting.

Right here is my up to date AMSC thesis.

Thesis

- AMSC is a lately remodeled firm, as soon as a play on the conservative US-based Jones Act, now your commonplace transport leasing firm with a fleet of probably engaging vessels with a hopeful upside producing a dividend yield of about 6.5%.

- For that cause, I am cautious right here. I would not purchase the corporate at right this moment’s valuation however would wait, if , for a little bit of a drop.

- My PT for the corporate now comes to fifteen NOK/share, which is the place I transfer my 2024E protection right here.

- The chance of the corporate dropping to this degree with out macro impacts is doubtlessly low – however this signifies simply what I am searching for earlier than I’d be prepared to “BUY” a spec inventory like this right here. Particularly one which as of 4Q23 has materially modified its danger/reward issue, and never for the higher, as I presently see it, with no change in ahead readability from the corporate that I can see both as of the AGM or the annual report.

Keep in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital good points and dividends within the meantime.

- If the corporate goes effectively past normalization and goes into overvaluation, I harvest good points and rotate my place into different undervalued shares, repeating #1.

- If the corporate would not go into overvaluation however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is basically protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is presently low-cost.

- This firm has a sensible upside primarily based on earnings progress or a number of growth/reversion.

The corporate fulfills 1 out of my 5 standards, making it a “HOLD” right here, bordering on a “SELL”.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}