Monty Rakusen/DigitalVision through Getty Photographs

Thesis

Utilized Supplies, Inc. (NASDAQ:AMAT), a semiconductor firm that manufactures gear that produces chips, OLED shows, and different electronics, has had sturdy and constant value motion over the previous 12 months, up nearly 90%. That is primarily attributable to its constant monetary progress and excessive liquidity ranges in addition to its various semiconductor gear portfolio that serves the quickly rising ICAPS business (IoT, Communications, Automotive, Energy, and Sensors). Nonetheless, I nonetheless suppose the inventory has extra room to develop, fueled by the potential progress coming from patterning machine Centura Sculpta, AMAT service income, and the OLED market.

Google Finance

Catalysts

Demand for Centura Sculpta Will Be Stronger than Anticipated

On Feb. 28, 2023, AMAT introduced their new expertise that transforms semiconductor patterning. Centura Sculpta is a machine that enables for lowered steps in chip manufacturing, permitting for just one cycle of sample printing as a substitute of two. This tremendously reduces chip capital prices by an estimated quantity of $250 million per 100K wafers per 30 days and reduces chip manufacturing prices by about $50 per wafer. Extra importantly, this new expertise will contribute to inexperienced initiatives by permitting the saving of greater than 15 kWh of power, 0.35 kg of CO2, and 15 liters of water, per wafer. That is what I imagine the main worth of Centura Sculpta comes from—its potential to avoid wasting a great deal of various kinds of power and assets in chip manufacturing, an energy-intensive business.

Chip manufacturing requires loads of power and water. TSMC (TSM), the world’s largest chipmaker, used 6% of Taiwan’s complete energy and produced about 15 million tons of carbon in 2020. As well as, the corporate additionally used 193,000 tons of water per day, which is about 70 billion liters of water in a single 12 months, in 2020. Mixed with local weather change, it’s not shocking that Taiwan skilled its worst drought in over 50 years between 2020 to 2021.

With that being mentioned, semiconductor producers are continuously trying to enhance their operations to realize minimal environmental influence, as demonstrated in TSMC’s 2022 Sustainability Report. I imagine Centura Sculpta’s potential to not solely make manufacturing extra environment friendly but in addition cut back power consumption goes to draw much more demand than what the critics are at present claiming.

Accelerated Service Income Development

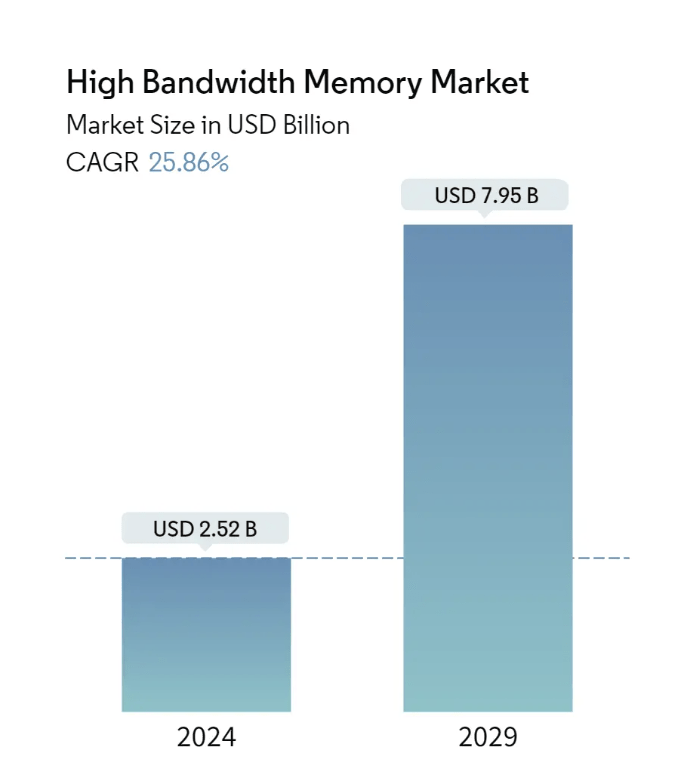

I imagine one other driver for AMAT’s future progress comes from the quickly increasing high-bandwidth reminiscence (HBM) packaging expertise.

HBM packaging permits for 3-D stacking of reminiscence chips, permitting them to be extra energy-efficient and to be extra compact. Presently, the market expects an enormous wave of progress within the HBM market, rising from a $2.52 billion market measurement to $7.95 B from 2024 to 2029 with a CAGR of 25.86%. Within the earnings name, they demonstrated confidence of their potential to seize this quickly rising market with their current applied sciences, stating that they count on their HBM packaging income to succeed in $0.5 billion in fiscal 2024—4 occasions as massive as that in fiscal 2023.

Motor Intelligence

Along with AMAT’s progress in HBM packaging applied sciences, I imagine there may also be super progress in AMAT’s Utilized International Providers (AGS) phase that accompanies the expansion in HBM. AGS provides providers that assist clients with the installment and upkeep of AMAT’s machines. HBM applied sciences require explicit upkeep attributable to greater machine utilization: the manufacturing of HBM chips requires further steps and a extra advanced process that causes greater machine utilization which results in greater demand attributable to extra put on and tear for the machines. As well as, the combination of HBM packaging applied sciences into corporations’ present manufacturing amenities may pose a problem.

These elements will increase the demand for AMAT’s upkeep providers. As machines are continuously in want of upkeep, the demand for AMAT’s providers is sticky. Within the 2023 annual report, AMAT’s service income, 22% of complete income for the 12 months 2023, grew 3% progress from final 12 months. Nonetheless, I predict that with the speedy progress of the HBM market, AMAT’s service income will develop at a charge of 8 – 10% sooner or later. With AMAT’s historic working margin for his or her service phase sitting at round 30%, this surge in service income will successfully be translated into bottom-line earnings, doubtlessly exceeding market expectations and boosting the inventory’s worth.

Fast Development within the OLED Section

Regardless of AMAT’s Show and Adjoining Markets phase, a enterprise unit that primarily produces gear that manufactures flat panel show merchandise, going through a gradual decline over the previous three years, I feel that AMAT’s Show and Adjoining Markets enterprise phase will really expertise a turnaround progress section by way of elevated machine gross sales, particularly machines that manufacture natural light-emitting diode show screens (OLED). AMAT is at present a market chief within the Flat Panel Show-Particular Tools market, proudly owning the largest piece of the pie—18.75% income share— in a market of $4.2 billion.

I imagine there are many alternatives for AMAT to seize within the OLED market, which is projected to develop at a CAGR of twenty-two.5% from now to 2030. Sooner or later, we are going to see an surprising surge in demand for OLED due to the necessity for AR/VR applied sciences, particularly AR/VR in healthcare, that rely closely on OLED shows. Whereas the AR/VR market is anticipated to develop at a CAGR of 11% from now to 2028, the healthcare AR/VR market is anticipated to develop at a a lot greater tempo.

In keeping with Statista, the healthcare AR/VR market has been the strongest in North America, valued at $477 million in 2028 and estimating an astonishing $4.6 billion in 2025, inserting North America because the quickest progress hub for healthcare AR/VR. One other report projected a CAGR of 18.2% for the worldwide healthcare AR/VR market, rising from $2.8 billion to $14.9 billion from 2024 to 2034. Subsequently, there’s super potential for AR/VR healthcare applied sciences in addition to OLED show manufacturing sooner or later, positioning AMAT in a positive place.

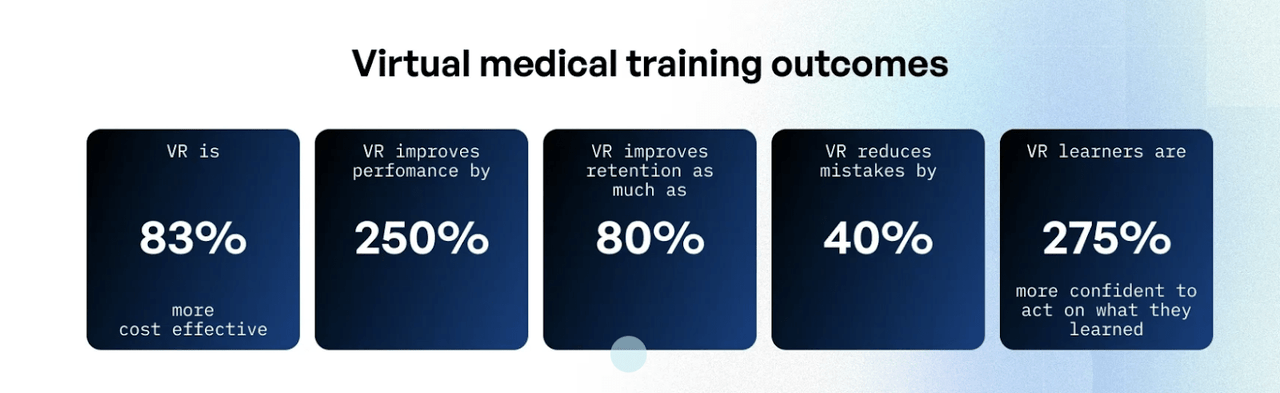

AR/VR expertise is essential to the way forward for healthcare due to its potential to revolutionize medical coaching. A research confirmed that the supply of an AR/VR surroundings really will increase engagement and retention in medical coaching than these with out the surroundings. One other research confirmed that surgeons educated in VR environments make 40% fewer errors than these with out the surroundings. Given these research and developments, I imagine that there will likely be a rise in reliance on AR/VR applied sciences from the healthcare industries thus boosting OLED gross sales within the course of, and rising AMAT’s Show and Adjoining Market phase.

I estimate that, for 2024, the corporate’s show gross sales will improve to five% of complete income from the earlier 3% and proceed to extend at about 2 proportion factors per 12 months by way of 2026, reversing the earlier pattern of phase income share discount and develop regularly together with the healthcare AR/VR market.

Onix Methods

Valuation

My Monetary Projections

Income Development Fee Projections

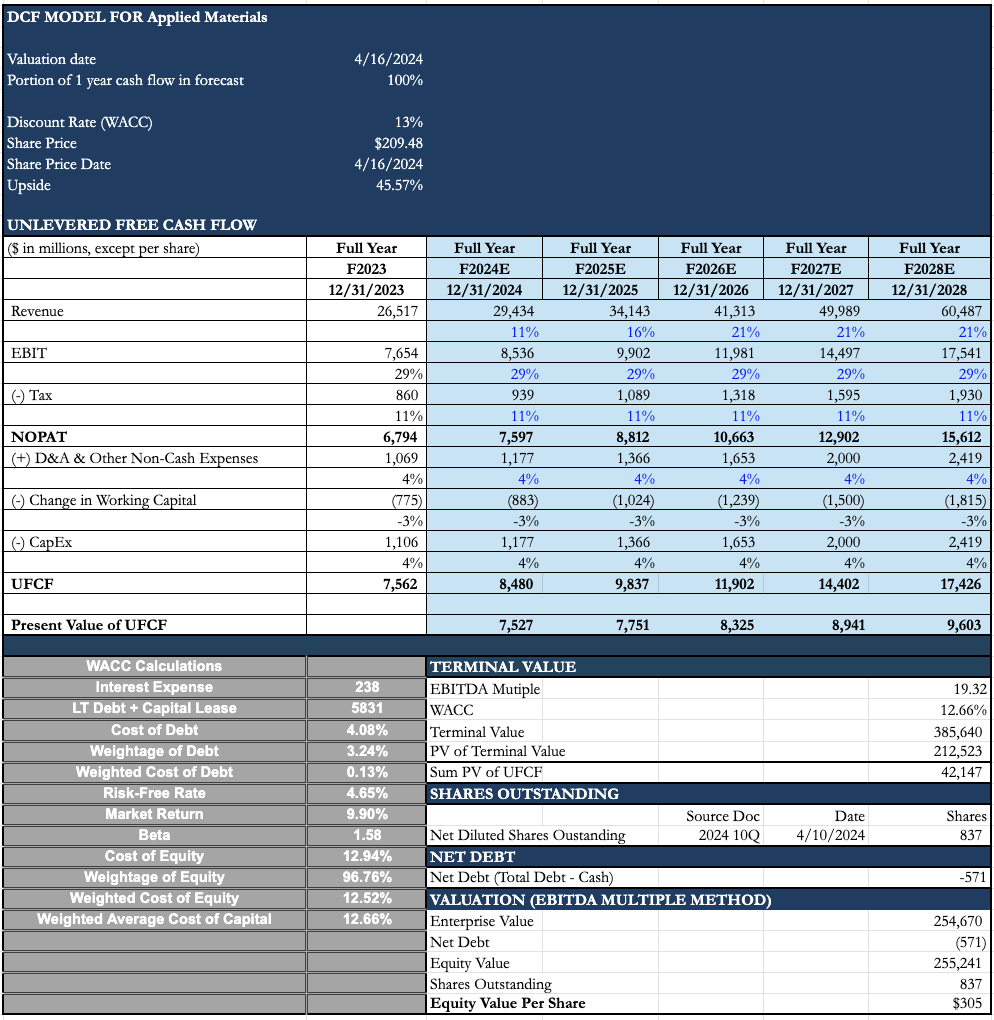

In my DCF mannequin, I first averaged the annual income progress charges for the corporate’s previous 5 years to get a base-case income progress charge of 11% for 2024. Then, primarily based on the three catalysts talked about above in addition to the long run progress of the semiconductor business, I elevated the anticipated income progress charge for 2025 to 16% and to 21% for the three years after that. Moreover, I assumed a relentless EBIT margin of 29% and a relentless D&A and CapEx expense as a proportion of income, as I imagine AMAT will proceed to decide to capital innovation to solidify and advance its market place.

Terminal Worth Projections

I then proceeded with the EBITDA a number of methodology to calculate the PV of the terminal worth. I first assumed a terminal progress charge of three%, which is on par with historic GDP progress charges, as a result of AMAT depends closely on demand for finish merchandise equivalent to automotive, client electronics, information facilities, and OLED shows which can be strongly related to GDP progress. For the exit EBITDA a number of, I used an EBITDA a number of of 19.32x, which is barely above the business common.

Weighted Common Price of Capital (WACC)

To calculate WACC, I first divided curiosity bills from long-term debt and capital leases; I then multiplied by the weightage of debt to discover a 0.13% Weighted Price of Debt. I exercised the same course of to unravel for the Price of Fairness, the place the 30-year treasury bond is the risk-free charge, the SPY historic common return is the market return, and I used PayPal’s beta of 1.58. After multiplying by the Weightage of Fairness, I arrived at a 12.52% Weighted Price of Fairness. Lastly, I added each the weighted value of debt and the weighted value of fairness to get a WACC of 12.66%.

Intrinsic Worth

I lastly summed the 5 years of projected money flows and current terminal worth to seek out the enterprise worth and subtracted it from internet debt. After dividing by complete shares excellent, I used to be led to a goal value of $305 per share, representing a 46% potential upside.

Dangers

Lack of Funding From Authorities

AMAT just lately confronted a major problem relating to its $4 billion semiconductor analysis facility that was planning to be in-built 2026. Regardless of the $52.7 billion funds promised by Biden’s CHIPS Act, the latest reallocation of federal funding excluded corporations like AMAT that aren’t concerned with the direct manufacturing of semiconductors. The enormous undertaking, involving the collaboration of a number of universities and private and non-private semiconductor corporations, is pressured to be postponed or canceled. Nonetheless, with AMAT’s sturdy dedication in the direction of innovation which is clear by their constant spending in R&D and CapEx, I imagine the undertaking will likely be postponed as a substitute of utterly terminated.

Conclusion

I wish to conclude this report with a Purchase Advice for AMAT inventory, with a goal value of $305. I imagine this value is justified by three necessary but surprising catalysts: the expansion within the new patterning expertise Centura Sculpta, the rise in service income pushed by the speedy enlargement of the HBM market, and the expansion within the show phase pushed by the enlargement of AR/VR to facilitate medical coaching. These elements, in my view, will contribute to driving AMAT’s future progress. Though the corporate is going through a scarcity of funding from the U.S. authorities, this isn’t going to cease AMAT from persevering with to stride in the direction of countless innovation, securing its place as a market chief in semiconductor gear.

{kind=link}