kemalbas

I final wrote about Arcturus Therapeutics Holdings (NASDAQ:ARCT) in September 2021. Readers can see the fundamentals of the corporate from that article right here.

The corporate is a number one self-amplifying mRNA researcher and vaccine supplier and has a beneficial lipo nanoparticle supply expertise.

Since my final article there was a bunch of constructive information. The constructive earnings in the latest quarter add substance to this information. Extra necessary than quarterly earnings is the money injection ensuing from the brand new settlement with CS.

By definition, small biotech shares are excessive danger. Arcturus does, nonetheless, meet the factors an investor ought to search for. These are good money reserves, joint ventures with Massive Pharma corporations, and a promising testing programme going ahead. Now is an effective time to spend money on the corporate, however all the time with the proviso that such corporations are excessive danger.

ARCT Q3 Earnings

Income and profitability usually are not probably the most vital components in a small-cap biotech. Nonetheless, these produced by Arcturus had been wholesome. Extra necessary is money balances.

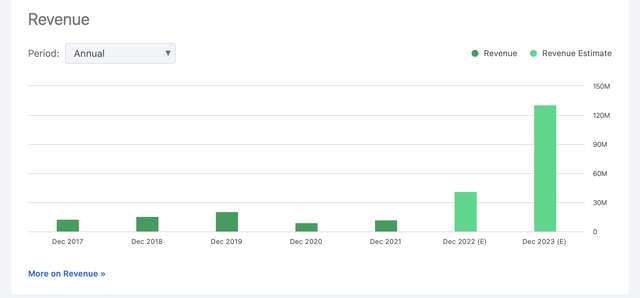

Primarily based on the SA Quant Scores, income is forecast to develop strongly, as per the illustration beneath:

in search of alpha

Q3 GAAP EPS was -$0.82, beating expectations by $1.04. Income of $27.09 million beat by $24.58 million.

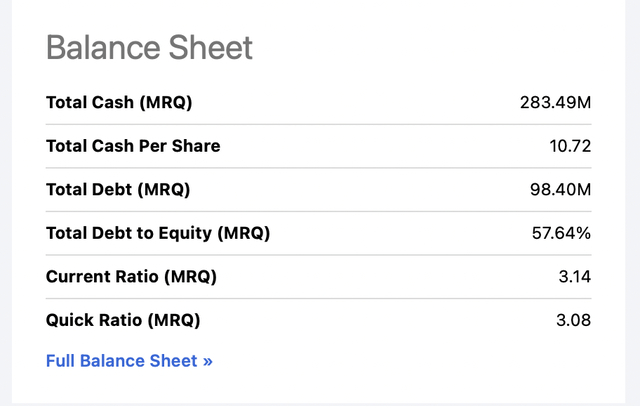

Money stability at $283.5 million compares to $370.5 million as of December 31, 2021. That was wholesome after money infusions from Vietnamese firm Vinbiocare and from the Financial Growth Board of Singapore. The corporate’s sturdy hyperlinks round Asia could possibly be of additional particular profit. Asia is probably the most populous continent and with a rising inhabitants and rising affluence. Nonetheless, Arcturus is now even more healthy with a pending sturdy infusion of money funds from the brand new tie-up detailed beneath.

The stability sheet particulars are as follows:

in search of alpha

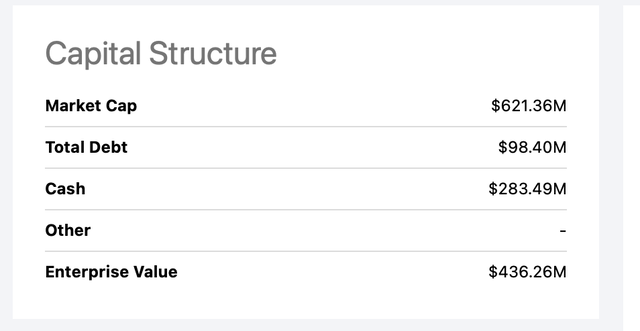

The capital construction is summarised beneath:

in search of alpha

The complete assertion of particulars will be seen within the firm press launch right here.

CSL Sequirus

Of all the excellent news coming in, the tie-up with CSL Sequirus appears probably the most related. CSL is a publicly listed unit of CSL Ltd (OTCPK:CSLLY). The corporate is a world chief in flu vaccine growth and distribution. They’re placing in $200 million upfront which supplies Arcturus “carte blanche” to push ahead with their analysis programme for the medium time period. The potential enter of funds from CSL is $4.3 billion. The small print of the settlement will be seen right here.

The deal provides CSL unique licensing rights for quite a lot of merchandise. Below the deal, Arcturus would get 40% of income on the COVID-19 merchandise. They’d additionally get double-digit royalties on different merchandise developed along side CSL.

On the analyst name CEO Joseph Payne reckoned the brand new funding secured means they’ve a enough money stability to hold out their deliberate bills for the following 3 years. That’s fairly a uncommon state of affairs for a small scale biotech firm. The three-year functionality doesn’t keep in mind any gross sales income that may happen.

Arcturus Pipeline

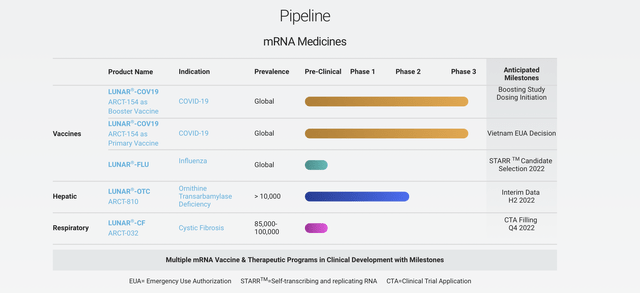

The pipeline is sort of complicated. A abstract of the corporate is illustrated beneath:

arcturus therapeutics

The corporate specialises in vaccines for Covid-19, influenza for different respiratory sicknesses and liver illnesses, and in pandemic preparedness. Goal therapies embrace additionally OTC (ornithine transcarbamylase deficiency) and cystic fibrosis. There’s at present no efficacious remedy for the OTC liver situation.

Wanting long-term, mRNA expertise generally can result in an virtually infinite variety of new therapies for numerous situations. As an illustration, rival BioNTech (NASDAQ:BNTX) is engaged on mRNA vaccines for malaria, tuberculosis, and HIV amongst others. The method permits the recipient’s personal cells successfully to turn into drug producers of the spike protein. This speedy and efficient method has led specialists to imagine that in 15 years time about one-third of all new drug approvals might be from mRNA medication.

Arcturus’ merchandise are primarily based round its STARR (self-transcribing and replicating RNA) platform expertise and LUNAR lipid-meditated supply expertise with its 250 proprietary lipids. That’s the place CSL successfully noticed the wealthy promise, particularly by way of the inhaler supply. The self-amplifying vaccines Arcturus can produce have sure main benefits over these out there proper now from Pfizer (NYSE:PFE) and Moderna (NASDAQ:MRNA).

They’re cheaper, simpler to move and simpler to retailer. That may be a vital distinction to curb an outbreak shortly. Covid-19 mRNA vaccines act on T-cells and assault Covid’s spike protein (t-cells are a kind of white cell which shield the physique in opposition to outdoors assaults). mRNA vaccines seem to have a greater security profile than inactivated vaccines by way of decrease incidence of unwanted side effects. These vaccines produce a far higher variety of these white cells than inactivated viruses equivalent to these produced by Sinovac and Sinopharm. It might be that future therapies would possibly advocate a mix of the 2 sorts of vaccine.

* The subsequent main growth ought to be in regard to the ARCT-154 Covid main and booster vaccine. That is anticipated to get Emergency Use Authorisation in Vietnam within the subsequent couple of months. It had profitable Part III effectivity trial ends in April this 12 months. The corporate had been working intently with its associate Vingroup in Vietnam. This now appears to have reached its concluding stage. Illustrated beneath from the corporate’s Twitter page is corporate workers assembly with the Vietnamese president:

Arcturus

Of explicit advantage right here is the truth that though ARCT-154 solely offered 55% safety in opposition to catching Covid, it offered 95% safety in opposition to hospitalisation or dying. That is an important issue now we now have moved into the truth that Covid is endemic around the globe. The main target now could be much less on avoiding catching Covid and extra on avoiding severe sickness from Covid.

In August this 12 months, their booster vaccine had been proven to be efficient in opposition to Omicron variants together with BA.5.

* As well as for COVID remedy there may be their ARCT-201 product. That is solely at Part 2 testing. It’s understood that this product was developed along side Duke-NUS in Singapore.

* ARCT-810 is focused at liver issues with OTC deficiency. It’s now transferring into Part II testing after Part 1B dosing. Its progress unexpectedly slowed this 12 months after delays in recruitment for the testing. Administration reiterated on the analyst name that they didn’t anticipate this drawback to recur.

* ARCT-032 is focused at lung issues from cystic fibrosis. This impacts about 70,000 individuals worldwide.

* LunaFlu is focused at influenza. This is perhaps developed along side CSL.

———————–

As well as, the corporate has numerous joint drug developments with outdoors events.

* Janssen Pharmaceutica, which is a part of Johnson & Johnson (JNJ), for hepatitis B.

* Ultragenyx (NYSE:RARE) for numerous uncommon illness targets.

* Takeda Pharmaceutical (NYSE:TAK) and Millennium Pharmaceutical for numerous mRNA developments

* Millennium Pharmaceutical for non-alcoholic steatohepatitis.

* Cooperation with Singapore Financial Growth Board and Duke-NUS Medical Faculty for Covid-19. That is already effectively superior. Singapore is focusing on itself to be a bio-pharma hub for Asia. Arcturus may gain advantage vastly from their shut cooperation with Singapore government-linked entities. It’s thought that the corporate has shut monetary and analysis ties with Israel as effectively.

ARCT Inventory Worth

The inventory worth has fallen consistent with the overall market.

The one-year inventory chart as offered by Charles Schwab Inc illustrates this:

charles schwab

This isn’t actually justified by the micro image of the corporate. It has been stated that the inventory worth has been artificially lowered by a cabal of brief merchants. I haven’t got the small print of this but when so they might should cowl quickly. Each day share buying and selling turnover for the corporate is just about $1 billion.

Inventory possession is sort of beneficial. 83.6% of inventory is owned by establishments. This could usually be considered steady for an organization. 12.2% is owned by firm insiders.

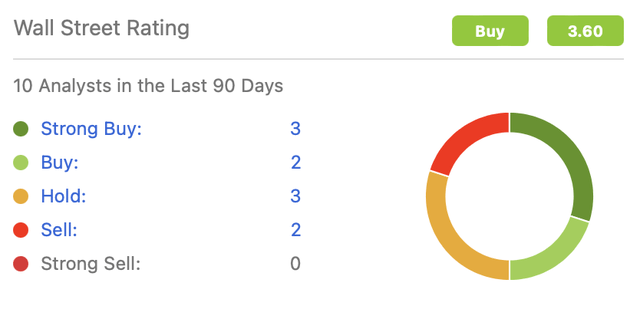

Normally, analysts are very blended on the corporate because the element beneath from SA evidences:

in search of alpha

Analysts have been altering their worth targets for the reason that outcomes and the CSL information. As an illustration, Citi has put in a brand new worth goal of $35. That is very conservative in my opinion in case you are bullish in regards to the firm. Baird alternatively have diminished their worth goal to $18 (impartial to underperform) on what I believe are fairly spurious grounds. Goldman has elevated their worth goal from $8 to $14. There could also be some connection between analyst forecasts and the shorting group.

Dangers

* Small biotechs equivalent to this are vulnerable to inventory worth manipulation by teams performing in live performance collectively.

* It might be that the promising pipeline medication all show to not be efficacious or to have dangerous unwanted side effects.

* The corporate might must bask in share dilution sooner or later to boost extra funds.

Conclusion

Current developments outlined on this article spotlight the corporate has a promising pipeline and the money to advance it. Earlier downturns within the inventory worth had primarily been centred round the concept the Covid-19 disaster was over. The truth is, it appears clear that Covid-19, together with influenza, is endemic and can proceed with no finish date in sight. Thus efficient and more cost effective vaccines might be a long-term want.

Arcturus has plenty of prime sights. It has a wonderful money runway. It has apparently very advantageous self-replicating mRNA expertise. It has particular strengths within the Asian area. In frequent with different drug growth corporations, it isn’t reliant on macroeconomic situations.

That doesn’t after all assure that the corporate’s merchandise might be commercially viable. Buyers ought to be aware that Arcturus is a lovely funding however nonetheless a high-risk one.

{kind=link}