Sakorn Sukkasemsakorn/iStock through Getty Pictures

Investing Atmosphere

US fairness markets reached new all-time highs in Q1 supported by a resilient US economic system, a normal pattern of disinflation and an acceleration in company earnings progress. Given largely benign financial information providing little indication {that a} recession is close to, rate of interest markets pared again the variety of anticipated Federal Reserve price cuts in 2024. The S&P 500® Index (SP500, SPX) rose 10.56%, persevering with the sturdy rally that started in late October of final yr. There was broad-based power throughout sectors. Communication companies, financials, vitality, industrials and expertise shares had been every up double-digit percentages. Greater yielding sectors (actual property, utilities and client staples) trailed.

The market’s transfer greater has been an unusually easy one. In Q1, the S&P 500® Index skilled solely three down days of 1 % or higher. Over the five-year interval from 2019 to 2023, the common quarter had 9 such days. There are many dangers that might upset the apple cart, whether or not geopolitical or macroeconomic. The continued conflicts within the Center East and Ukraine proceed to rage, and inflation—although trending decrease—stays above the Federal Reserve’s 2% goal. Markets in the course of the first three months of the yr confirmed comparatively little concern, nevertheless. Earnings—the bedrock of enterprise values—are rising soundly as soon as once more, and the recession that many predicted would have began by now has but to emerge. Nonetheless, volatility has picked up in April as we write this letter.

Efficiency Dialogue

In Q1, the portfolio carried out in keeping with our complete return expectations—delivering a powerful complete return comprised of premium revenue (a portfolio present yield that’s higher than or equal to 2X the common present yield for shares within the S&P 500® Index) and stable capital appreciation. Our Core Worth, Dividend Restoration and Dividend Development holdings drove our total return as bond proxies and stuck revenue securities trailed the broad fairness market.

Our high contributors had been nVent Electrical (NVT), Corebridge Monetary (CRBG) and Lamar Promoting (LAMR). nVent Electrical gives electrical connections and safety options. These are mission-critical parts in industrial electrical and mechanical methods and civil infrastructure. nVent has proven constant and regular progress because the pandemic, having reported 12 consecutive quarters of year-over-year gross sales progress supported by the secular tailwinds of electrification, sustainability and digitalization. Development has come from a mixture of volumes and pricing, with the corporate efficiently offsetting inflation with pricing. Because of the low price of its merchandise relative to a undertaking and excessive failure prices for patrons, nVent has good pricing energy and sustainable margins. Within the latest quarter, the corporate’s information facilities enterprise (~14% of gross sales) was a standout, rising 20% yr over yr, because the acceleration in synthetic intelligence infrastructure investments has created elevated demand for the corporate’s liquid cooling options. Although nVent is not promoting as cheaply as when it first drew our curiosity, the inventory nonetheless sells at a decrease P/E a number of than the S&P 500® Index regardless of higher earnings progress.

Corebridge, a life insurance coverage and retirement options firm, was beforehand a unit of AIG and a September 2022 IPO. AIG nonetheless owns ~51% of the corporate following its latest secondary sale in November 2023, equaling 9.1% of shares excellent. Since including Corebridge to the portfolio in Q1 2023, it’s been amongst our high performers because the “greater for longer” rate of interest atmosphere has pushed a rise in unfold revenue. Our funding thesis has been that Corebridge would profit from the present rate of interest atmosphere following ZIRP (zero rate of interest coverage) and would even have loads of room to enhance its aggressive place and wring out efficiencies to enhance ROE now that it’s a standalone entity that’s not half of a giant inefficient and capital-constrained mum or dad. Even after latest inventory value good points, Corebridge yields 3.2% on its dividend, with a double-digit free money circulate yield. Along with Corebridge’s common dividend, the corporate paid two particular dividends in 2023 totaling $1.78, which is 7.6% on the March quarterending inventory value. Moreover dividends, we count on free money circulate will probably be used to make sure holding firm liquidity, retire diluted shares and assist modest progress expectations.

Lamar Promoting—our largest place—operates outside promoting buildings comparable to billboards, digital billboards and transit advertisements. Outcomes have been comparatively regular, with power in native/regional gross sales lifting the highest line, whereas margin enchancment drove better-than-expected earnings progress. Along with returning money to shareholders (the dividend yields 4.7%), administration is concentrated on delevering the stability sheet given restricted M&A alternatives. Whereas the corporate’s progress can ebb and circulate, over the long run, the corporate has skilled common annualized natural progress within the excessive single digits, supplemented by small tuckin acquisitions. With a file of persistently producing free money circulate and prudent capital allocation that features excessive return of capital to shareholders, this inventory matches our course of.

Our backside contributors had been Cable One (CABO), Philips (PHG) and Common Well being Realty Earnings Belief (UHT). Cable One, a small cable firm working in rural US markets, was our greatest detractor in Q1. Shares have remained weak because of issues about competitors from wi-fi suppliers and depressed subscriber progress, pushed partly by fewer residential strikes in a frozen US housing market. Broadband subscriber additions picked up within the newest quarter, however elevated promotions and discounting decreased common income per subscriber, and an finish to the ACP (Reasonably priced Connectivity Program) accepting new enrollees creates a further headwind to rising subscribers. Whereas wi-fi firms are coming into new markets, 5G is just not presently aggressive with cable’s obtain speeds, and based mostly on the physics of wi-fi information supply, 5G is unlikely to be aggressive with cable for a few years, if ever. Cable continues to have a aggressive benefit with respect to community speeds, reliability and capital depth. Regardless of latest progress challenges, free money circulate conversion stays stable, and the valuation is very enticing, having a free money circulate yield of ~12% and promoting under our estimate of 8X normalized earnings. We just like the cable enterprise typically because of its excessive recurring income, pricing energy and wholesome working leverage.

Since Philips, a well being care expertise firm, initiated a voluntary recall of its first-generation CPAP machine greater than two years in the past, buyers have shunned the inventory as a result of uncertainty associated to potential litigation liabilities. That has left the inventory extraordinarily undervalued. In January, Philips agreed with the US authorities on a proposed consent decree offering a roadmap of required actions and prohibitions—a course of prone to take three years to conclude. As a part of the consent decree, Philips is prohibited from promoting CPAP or BiPAP sleep gadgets within the US. Nonetheless, Philips should still service sleep and respiratory care gadgets already with well being care supplier and sufferers and will proceed to promote different merchandise within the US. Additional, it doesn’t influence the corporate’s gross sales outdoors the US. The general phrases are as anticipated, and there may be now a path ahead for Philips to ultimately return to the market. We respect that till there may be higher readability on the full settlement price, the inventory could stay below stress, however on the present asking value, shares promote at a big low cost to our estimates of intrinsic worth.

Common Realty Earnings Belief (UHT) is a well being care REIT (actual property funding belief) specializing in well being care amenities, together with acute care hospitals, behavioral well being facilities and medical workplace buildings. Our preliminary buy was in June 2023. Like different excessive revenue producing shares, UHT has been out of favor given greater rates of interest. Moreover the inventory promoting at low ranges relative to its historic valuation and different REITs, we preferred UHT’s observe file of execution, low leverage, decreased cyclicality and constant annual dividend progress. It presently yields almost 8%. Current outcomes have been sturdy, with income progress up over 5% pushed by annual lease value escalators, a greater mixture of property, elevated occupancy and M&A. Nonetheless, UHT was down in Q1 together with the broader actual property sector as interest-rate delicate areas badly lagged the remainder of the market.

Portfolio Exercise

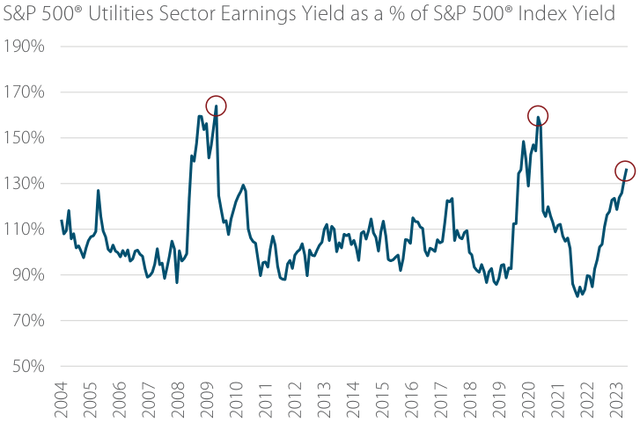

In Q1, we added two utilities to the portfolio: Alliant Power (LNT) and Evergy (EVRG). Alliant Power is a US-regulated electrical energy and pure gasoline utility working within the Midwest. Evergy is a Kansas-based, absolutely built-in, absolutely electrical utility. Because the sector has lagged considerably over the previous yr, resulting in an above-average earnings yield relative to the broader market (Exhibit 1), we’re discovering extra alternative.

Exhibit 1: Utilities Sector: Mispriced Yield

Supply: Artisan Companions/FactSet. As of 31 Mar 2024. Previous efficiency doesn’t assure and isn’t a dependable indicator of future outcomes.

As a gaggle, utilities have been out of favor for just a few causes. The rate of interest atmosphere has made bonds extra interesting, and better inflation has elevated labor, gear and commodities prices whereas additionally elevating utilities’ prices of capital. Utility firms can go on plenty of their prices to prospects; nevertheless, charges are regulated, and regulators have strived to restrict the rise in prospects’ utility payments, which have already skilled massive will increase within the post-COVID inflationary interval. Consequently, utilities haven’t been capable of enhance their ROEs as latest charges instances have gone in opposition to them.

Alliant Power serves roughly 995,000 electrical and 425,000 pure gasoline prospects by way of two public utility subsidiaries, Interstate Energy and Mild (operates in Iowa) and Wisconsin Energy and Mild. Regardless of little change within the firm’s regulatory or working environments, the inventory has retrenched over the previous yr, and it now trades for about 16X P/E in comparison with a mean of 18X over the previous 10 years and has a 3.6% dividend yield. The corporate continues to put money into price base, and a optimistic end result on its present price case in September may give it a lift.

Evergy serves greater than 1.7 million prospects in Kansas and Missouri. Along with the aforementioned dynamics weighing on utilities share costs, Evergy had two key price instances in 2023, one in Kansas and the opposite in Missouri, that offered danger for buyers. The Missouri case went higher than anticipated, however the returns allowed by the Kansas regulator had been punishingly low. Although Evergy operates in a subpar regulatory atmosphere, the utility is an efficient operator, with sturdy buyer satisfaction scores, below-average capex wants and a clear stability sheet. The regulatory atmosphere could enhance sooner or later, however even when it doesn’t, Evergy trades for simply 13X 2024 earnings, which is under common relative to its historical past and friends— and pays a dividend yielding 4.7%.

We additionally added Ryanair Holdings (RYAAY), an Eire-based low-cost airline centered on the European market. The airline’s low-cost, excessive on-time, high-efficiency mannequin has helped it to take share from inefficient legacy and state-sponsored carriers over the previous 20 years. Ryanair retains a web money stability sheet to opportunistically buy plane countercyclically when it will possibly accomplish that at cheaper costs. Moreover, the corporate’s economics are favorable. It has pricing energy because of business consolidation, capability progress that’s under demand progress and an absence of overlap on key routes. This results in sturdy returns on fairness and margins. Ryanair lately initiated its first dividend coverage, and we estimate the dividend may yield 2%–3%. Along with the dividend, Ryanair is predicted to repurchase inventory. Over the past decade, the corporate has retired 20% of its share rely. That is exceptional contemplating it was a growth-focused airline and nonetheless had web money after a pandemic. The inventory sells at a horny low-doubledigit P/E, however we don’t want a number of enlargement for this funding to contribute effectively to our portfolio revenue and capital appreciation aims. We imagine merely continued execution of the enterprise ought to result in stable returns.

Perspective

With market-cap weighted indices hitting new highs and the S&P 500® Index promoting for 23X (FY1) earnings, value-conscious buyers—a gaggle during which we proudly admit to being members—could really feel some trepidation relating to ahead return expectations for the asset class. Nonetheless, we imagine it could be a mistake to focus solely on the S&P 500® Index, which has grow to be more and more concentrated amongst just a few mega-cap shares, and in our view, not represents the varied alternative set that exists inside our price funding universe. As we’ve famous in prior letters and on our weblog Artisancanvas.com, worth is traditionally low-cost. Other than the pandemic years of 2020 to 2021, large-cap worth hasn’t been this low-cost relative to large-cap progress because the aftermath of the tech bubble. The Russell 1000® Worth Index trades for 16.5X FY1 estimated earnings. The Russell 1000® Development Index trades at 28.8X FY1 estimates. The typical and median valuation spreads between these indices have been 7.8 and 6.1 share factors over the previous 26 years. At this time, it’s 12.2 share factors. We don’t know if the valuation premium for progress shares will revert in a yr or over the subsequent 10, however we do know that the present unfold positions worth shares favorably from right here.

|

Rigorously contemplate the Fund’s funding goal, dangers and costs and bills. This and different necessary info is contained within the Fund’s prospectus and abstract prospectus, which may be obtained by calling 800.344.1770. Learn fastidiously earlier than investing. Present and future portfolio holdings are topic to danger. The worth of portfolio securities chosen by the funding staff could rise or fall in response to firm, market, financial, political, regulatory or different information, at occasions higher than the market or benchmark index. A portfolio’s environmental, social and governance (“ESG”) concerns could restrict the funding alternatives out there and, consequently, the portfolio could forgo sure funding alternatives and underperform portfolios that don’t contemplate ESG components. There isn’t a assure that the businesses during which the portfolio invests will declare dividends sooner or later or that dividends, if declared, will stay at present ranges or enhance over time. The fairness, mounted revenue and by-product safety varieties referenced every include inherent dangers, together with the danger of loss like all investments, and capital appreciation and revenue is just not assured. Worldwide investments contain particular dangers, together with forex fluctuation, decrease liquidity, totally different accounting strategies and financial and political methods, and better transaction prices. These dangers usually are higher in rising and fewer developed markets, together with frontier markets. Worth securities could underperform different asset varieties throughout a given interval. Securities of small- and medium-sized firms are inclined to have a shorter historical past of operations, be extra risky and fewer liquid and will have underperformed securities of huge firms throughout some durations. S&P 500® Index measures the efficiency of 500 US firms centered on the large-cap sector of the market. Russell 1000® Development Index measures the efficiency of US large-cap firms with greater value/guide ratios and forecasted progress values. Russell 1000® Worth Index measures the efficiency of US large-cap firms with lower cost/guide ratios and forecasted progress values. The Dow Jones US Choose Dividend Index measures the efficiency of the US’s main shares by dividend yield. The index(es) are unmanaged; embrace web reinvested dividends; don’t mirror charges or bills; and are usually not out there for direct funding. This abstract represents the views of the portfolio managers as of 31 Mar 2024. These views could change, and the Fund disclaims any obligation to advise buyers of such modifications. For the aim of figuring out the Fund’s holdings, securities of the identical issuer are aggregated to find out the burden within the Fund. The holdings talked about above comprise the next percentages of the Fund’s complete web property as of 31 Mar 2024: nVent Electrical PLC 2.1%, Corebridge Monetary Inc 1.8%, Lamar Promoting Co 3.7%, Cable One Inc 3.4%, Koninklijke Philips NV 1.1%, Common Well being Realty Earnings Belief 1.3%, Alliant Power Corp 1.7%, Evergy Inc 1.5%, Ryanair Holdings PLC 1.5%. Securities named within the Commentary, however not listed below are not held within the Fund as of the date of this report. Portfolio holdings are topic to vary with out discover and are usually not supposed as suggestions of particular person securities. All info on this report, except in any other case indicated, contains all courses of shares (besides efficiency and expense ratio info) and is as of the date proven within the higher proper hand nook. This materials doesn’t represent funding recommendation. Portfolio safety yields are topic to market situations and are usually not assured. The International Business Classification Normal (GICS®) is the unique mental property of MSCI Inc. (MSCI) and Normal & Poor’s Monetary Providers, LLC (S&P). Neither MSCI, S&P, their associates, nor any of their third social gathering suppliers (“GICS Events”) makes any representations or warranties, specific or implied, with respect to GICS or the outcomes to be obtained by the use thereof, and expressly disclaim all warranties, together with warranties of accuracy, completeness, merchantability and health for a specific goal. The GICS Events shall not have any legal responsibility for any direct, oblique, particular, punitive, consequential or every other damages (together with misplaced earnings) even when notified of such damages. The S&P 500® and Dow Jones US Choose Dividend (“Indices”) are merchandise of S&P Dow Jones Indices LLC (“S&P DJI”) and/or its associates and has been licensed to be used. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P International, Inc. All rights reserved. Redistribution or copy in entire or partly are prohibited with out written permission of S&P Dow Jones Indices LLC. S&P® is a registered trademark of S&P International and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). None of S&P DJI, Dow Jones, their associates or third social gathering licensors makes any illustration or guarantee, specific or implied, as to the power of any index to precisely symbolize the asset class or market sector that it purports to symbolize and none shall have any legal responsibility for any errors, omissions, or interruptions of any index or the info included therein. Frank Russell Firm (“Russell”) is the supply and proprietor of the emblems, service marks and copyrights associated to the Russell Indexes. Russell® is a trademark of Frank Russell Firm. Neither Russell nor its licensors settle for any legal responsibility for any errors or omissions within the Russell Indexes and/or Russell rankings or underlying information and no social gathering could depend on any Russell Indexes and/or Russell rankings and/or underlying information contained on this communication. No additional distribution of Russell Knowledge is permitted with out Russell’s specific written consent. Russell doesn’t promote, sponsor or endorse the content material of this communication. Attribution is used to judge the funding administration choices which affected the portfolio’s efficiency when in comparison with a benchmark index. Attribution is just not precise, however ought to be thought of an approximation of the relative contribution of every of the components thought of. Portfolio holdings are labeled into 5 revenue classes: Core Worth, Dividend Restoration, Dividend Development, Bond Proxy and Capital Construction. Core Worth holdings are investments per the staff’s worth investing strategy that even have an revenue part. Dividend Restoration holdings are investments the place the present yield doesn’t mirror the long run payout. Dividend Development holdings are investments the place the dividend payout is predicted to develop over a multiyear interval. Bond Proxy holdings are investments in companies that are much less economically delicate and have regular dividend polices. Capital Construction holdings are devices that comprise non-equity elements of the capital construction (e.g., most popular securities, convertibles and bonds). This materials is supplied for informational functions with out regard to your explicit funding wants and shall not be construed as funding or tax recommendation on which you will rely in your funding choices. Buyers ought to seek the advice of their monetary and tax adviser earlier than making investments as a way to decide the appropriateness of any funding product mentioned herein. Free Money Stream is a measure of economic efficiency calculated as working money circulate minus capital expenditures. Free Money Stream Yield is an total return analysis ratio of a inventory, which standardizes the free money circulate per share an organization is predicted to earn in opposition to its market value per share. The ratio is calculated by taking the free money circulate per share divided by the share value. Worth-to-Earnings (P/E) is a valuation ratio of an organization’s present share value in comparison with its per-share earnings. Dividend Yield is a monetary ratio that exhibits how a lot an organization pays out in dividends every year relative to its share value. Normalized Earnings are earnings which might be adjusted for the cyclical ups and downs over a enterprise cycle. Earnings Yield (which is the inverse of the P/E ratio) is the corporate’s per-share earnings divided by its present share value. Unfold is the distinction in yield between two bonds of comparable maturity however totally different credit score high quality. Artisan Companions Funds provided by way of Artisan Companions Distributors LLC (APDLLC), member FINRA. APDLLC is a completely owned dealer/vendor subsidiary of Artisan Companions Holdings LP. Artisan Companions Restricted Partnership, an funding advisory agency and adviser to Artisan Companions Funds, is wholly owned by Artisan Companions Holdings LP. © 2024 Artisan Companions. All rights reserved. |

Unique Put up

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.

{kind=link}