With Market enrollment at a document excessive, the upcoming open enrollment interval might be among the many busiest but. Along with Market enrollees renewing protection, uninsured folks and people shopping for particular person protection off-Market might need to test if they’re eligible for expanded subsidies underneath the not too long ago handed Inflation Discount Act. As we method the tenth annual ACA open enrollment, let’s take a step again to see how many individuals are at present signed up for particular person market protection on- and off-Market and what they could contemplate when purchasing for well being protection.

Right here, we mix federal enrollment information with administrative information insurers report back to state regulators, as compiled by Mark Farrah Associates, to see how many individuals are signed up for every kind of particular person market protection, each on- and off-Market and with or with out subsidies, as of early 2022. We discover that as Market enrollment has reached document highs, fewer persons are shopping for protection off-Market, however the general particular person market is nonetheless rising.

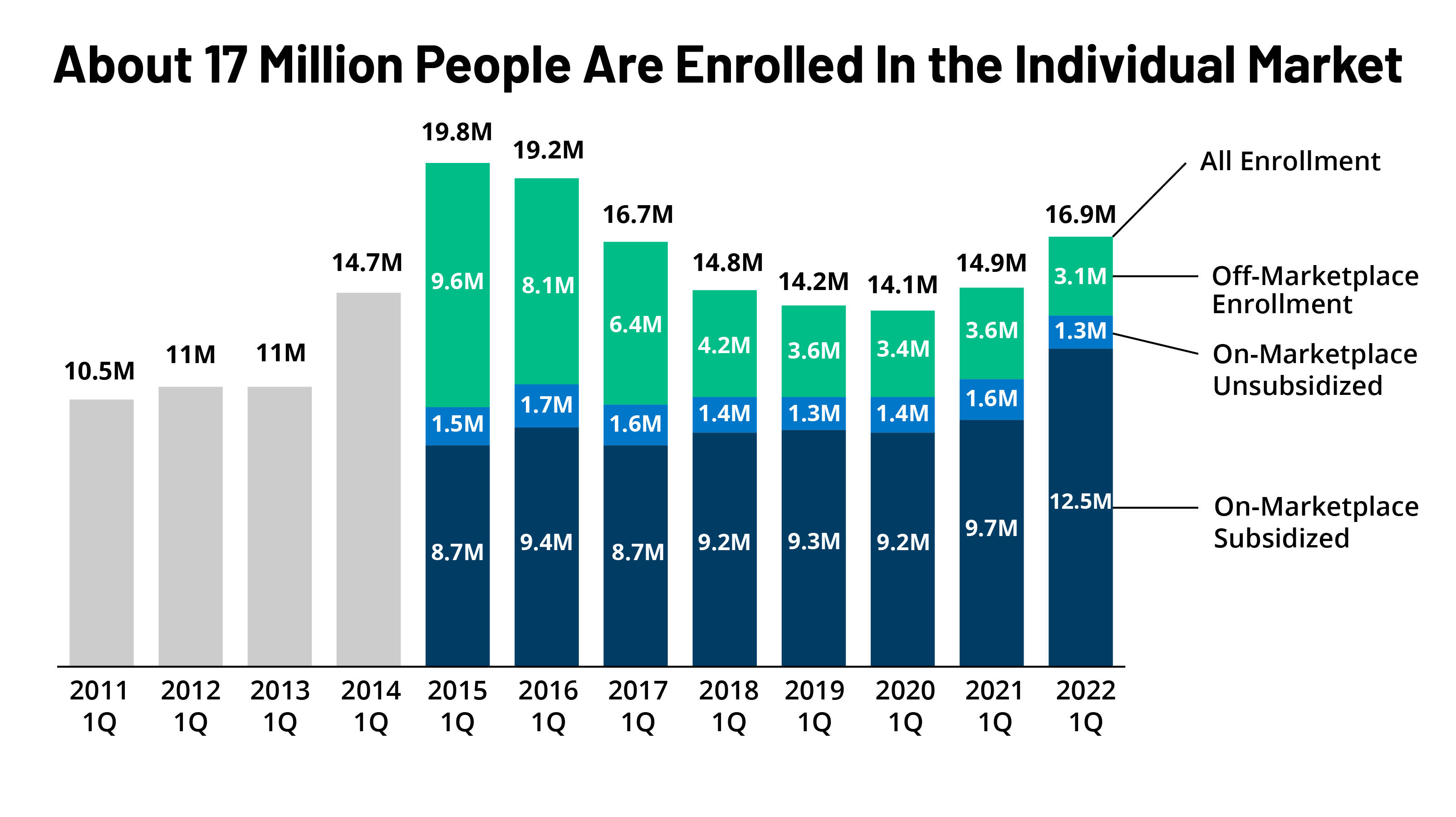

Particular person market enrollment is rising once more, pushed by enhanced subsidies. As of early 2022, we estimate there are 16.9 million folks with particular person market protection, the very best enrollment since 2016 (Determine 1). The person medical health insurance market grew quickly within the early years of ACA implementation, reaching practically 20 million folks in early 2015, practically double the roughly 11 million signed up earlier than the ACA. Nevertheless, these enrollment features have been partially offset by subsequent declines, significantly amongst folks not receiving subsidies amid steep premium will increase the next years. By early 2020, the person market had declined to about 14 million enrollees. (As a result of some plans don’t file quarterly information, we alter these plans’ enrollment numbers primarily based on enrollment adjustments seen in plans that do file quarterly. We additionally take away probably Youngsters’s Well being Insurance coverage Program, or CHIP, enrollees from the person market complete.)

With passage of enhanced subsidies within the American Rescue Plan Act (ARPA), mixed with boosted outreach and an prolonged enrollment interval, 2021 marked the primary yr since 2015 when there was a rise in particular person market enrollment. Particular person market enrollment grew about 5% from 14.1 million in first quarter 2020 to 14.9 million in first quarter 2021.

The ARPA’s subsidies didn’t merely carry folks from off-Market plans to the Market; the subsidies additionally helped carry general particular person market enrollment greater, as much as 16.9 million in early 2022, a rise of about 20% from early 2020.

Now, with enhanced subsidies in place, the overwhelming majority of individuals shopping for protection on the person market are sponsored. The not too long ago handed Inflation Discount Act continues the ARPA subsidies with out interruption for one more three years by 2025. Which means premiums are capped for folks with incomes over 400% of the poverty degree ($111,000 for a household of 4) who have been ineligible for subsidies beforehand, and those that have been already eligible for subsidies are paying even lower than they have been earlier than. General, about three in 4 particular person market enrollees at the moment are sponsored – by far the very best share because the ACA was carried out – and a few of those that aren’t receiving a subsidy may discover they’re eligible in the event that they moved onto the Market.

Heading into 2023 open enrollment, we estimate there are nonetheless about 3 million folks shopping for unsubsidized protection off-Market, together with some in non-ACA-compliant plans (like grandfathered and short-term plans). Regardless of Trump Administration efforts to advertise non-compliant protection, the variety of folks in non-compliant plans has fallen every year. Utilizing federal danger adjustment and effectuated enrollment information, we estimate 1.3 million folks have been in non-compliant plans in mid-2021, in comparison with 5.7 million in mid-2015. Though we don’t but have full 2022 information, it’s probably ACA-compliant enrollment (each on- and off-Market) is at present at a document excessive and that non-compliant enrollment is at a document low.

Some off-Market enrollees will discover they’re nonetheless ineligible for subsidies, even with enhanced subsidies. Undocumented immigrants and folks with reasonably priced affords of employer protection are ineligible for Market subsidies. Moreover, though there isn’t any longer an higher earnings restrict for subsidies, folks with greater incomes who would pay lower than 8.5% of their earnings for an unsubsidized benchmark silver plan are ineligible for subsidies as a result of their premium isn’t excessive sufficient to set off monetary assist. Even so, a few of the latter group might discover it advantageous to buy on the Market as a result of in the event that they expertise midyear adjustments of their earnings or different circumstances, they might start receiving subsidies mid-year with out altering plans or they may retroactively declare a subsidy once they file taxes.

How may future premium will increase have an effect on folks within the particular person market? Wanting again during the last 9 years of the ACA, adjustments in particular person market enrollment intently mirror adjustments in what folks needed to pay for protection. In years when premiums have been rising steeply from 2016-2018, unsubsidized particular person market enrollment fell. When premiums held principally regular in 2019 and 2020, so did particular person market enrollment. Then, as new subsidies grew to become obtainable in 2021 and 2022, particular person market enrollment picked up once more, pushed by a rise within the variety of sponsored enrollees.

Heading into 2023, we may even see unsubsidized premiums rise extra steeply than in previous years, pushed up by rising well being care costs and utilization. If premiums do rise, we may even see additional erosion of unsubsidized off-Market protection. Nevertheless, in contrast to when premiums rose in previous years, the Inflation Discount Act’s enhanced subsidies might defend the overwhelming majority of particular person market enrollees from will increase, even these with greater incomes. Actually, some individuals who aren’t sponsored in 2022 might discover premium will increase in 2023 make them newly eligible for subsidies (if their benchmark premium rises above 8.5% of their earnings). However, to make the most of subsidies, they would wish to buy on the Market throughout open enrollment.

{kind=link}