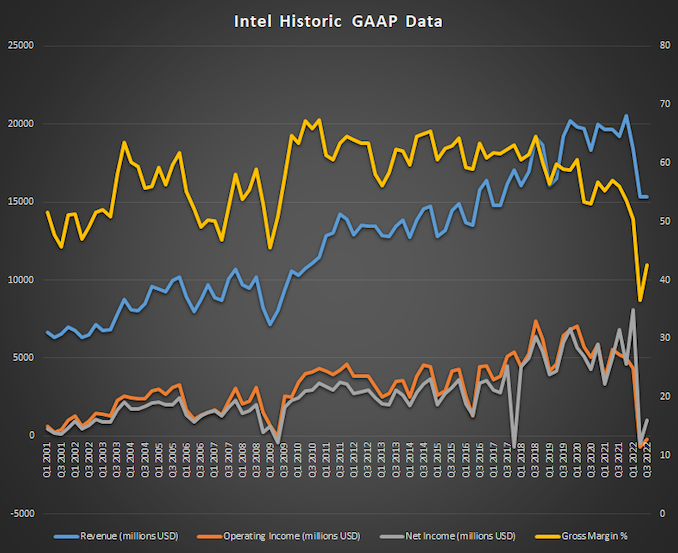

Whereas at all times an fascinating subject by default, company earnings reviews within the tech trade have grow to be particularly essential in the previous few months, because the trade prepares to climate what’s anticipated to be the largest downturn in demand within the final a number of years. Intel’s brutal Q2’22 report, which discovered the corporate dropping cash on a GAAP foundation for the primary time in 5 years, appears to have been a herald of issues to return for the most important trade, with AMD and different corporations since issuing earnings warnings forward of their very own Q3 reviews. In order the primary main tech firm to publish their full Q3’22 earnings report, Intel is as soon as once more prone to be a barometer of the tech trade’s efficiency over the previous three months.

For the third quarter of 2022, Intel reported $15.3B in income, a $3.9B decline versus the year-ago quarter. In comparison with Intel’s harsh Q2 report, the corporate has returned to profitability, reserving a cool billion {dollars} in web earnings, although that is nonetheless effectively beneath their historic norms. In reality, the corporate remains to be working at a (GAAP) loss, reserving an working earnings of -$175M. For Q3 not less than, it might seem that it’s Intel’s tax state of affairs that’s pushing them into the black, with the corporate recording a $1.2B tax profit.

| Intel Q3 2022 Monetary Outcomes (GAAP) | |||||

| Q3’2022 | Q2’2022 | Q3’2021 | |||

| Income | $15.3B | $15.3B | $19.2B | ||

| Working Revenue | -$175M | -$700M | $5.2B | ||

| Web Revenue | $1.0B | -$454M | $6.8B | ||

| Gross Margin | 42.6% | 36.5% | 56.0% | ||

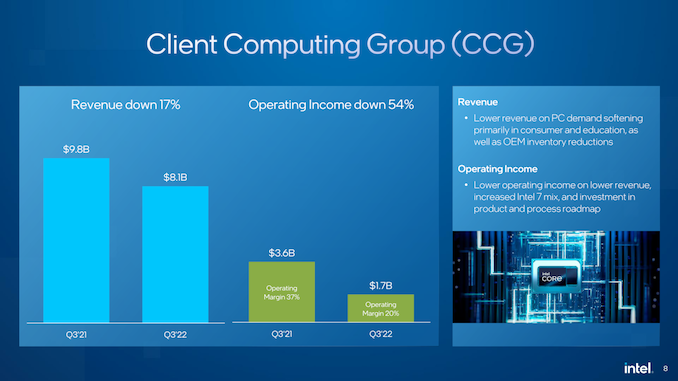

| Consumer Computing Group Income | $8.1B | +5% | -17% | ||

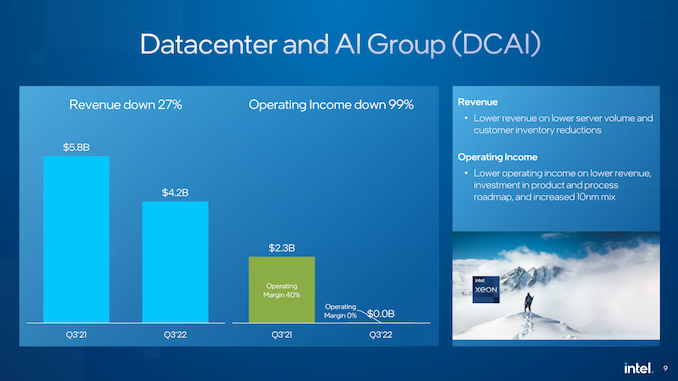

| Datacenter & AI Group Income | $4.2B | -9% | -27% | ||

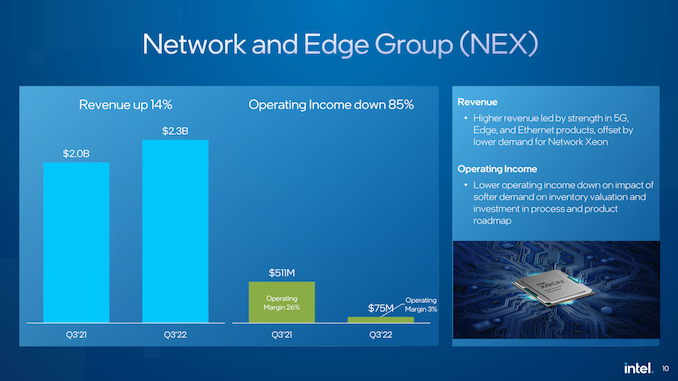

| Community & Edge Group Income | $2.3B | flat | +14% | ||

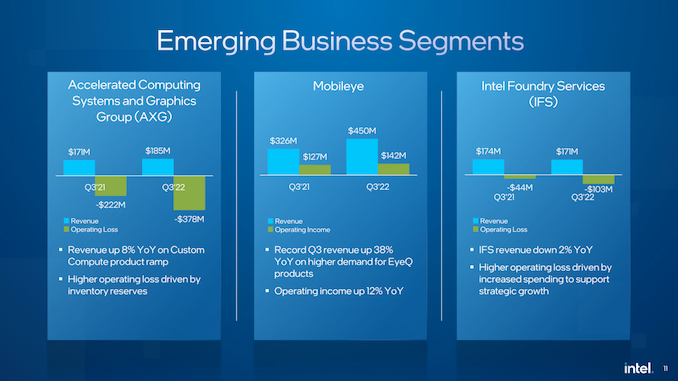

| Accelerated Computing Methods and Graphics Group Income | $185M | -1% | +8% | ||

| Mobileye | $450M | -2% | +38% | ||

| Intel Foundry Companies Income | $171M | +40% | -2% | ||

With that stated, after the hit Intel took in Q2, the corporate does seem like turning the nook, if slowly. Gross margins have improved to 42.6%, which though nonetheless beneath Intel’s historic (and even latest) common, is not less than excessive sufficient to maintain the corporate’s working earnings near constructive figures.

These figures additionally replicate some one-off expenses, particularly a $664M restructuring cost that Intel is taking now with a purpose to cut back ongoing prices (i.e. layoffs). We’ll go extra into Intel’s future projections and actions a bit afterward, however briefly, whereas Intel is prone to have seen the worst of issues on their finish, Intel is as soon as once more lowering their income projections for the 12 months because the bust cycle that the whole PC trade goes by means of isn’t over but.

Breaking issues down by Intel’s particular person enterprise teams, each of Intel’s main teams, CCG and DCAI, are down considerably on a year-over-year foundation. Observe that that is nonetheless the primary 12 months of Intel’s reorganized enterprise teams, so Intel has wanted to offer year-over-year comparisons for a way the brand new teams would have carried out in the event that they had been in place final 12 months.

Beginning as at all times with the CCG, Intel’s consumer group booked $8.1B in income, which is down 17% from the year-ago quarter. Probably the most uncovered to the collapse of the buyer market, CCG has been impacted by OEMs ordering fewer chips because of their very own massive inventories, as client and schooling system gross sales sluggish. Working margins are additionally equally down, as a consequence of a mixture of decrease revenues to e book prices in opposition to and Intel’s continued investments in product improvement.

For the quick time period, Intel expects the Complete Addressable Market (TAM) for the PC market to shrink by the “mid-to-high teenagers” for 2022, with that hit persevering with by means of the remainder of the 12 months. The latest launch of Intel’s 13th era Core (Raptor Lake) elements will assist to induce some new demand, however not sufficient to completely offset the general drop within the a lot bigger PC market.

As for Intel’s Information Heart and AI group (DCAI), the corporate took a fair bigger income hit there. For Q3 Intel booked $4.2B in DCAI income, down 27% from the year-ago quarter.

This drop in income has all however worn out the working profitability of the group, with Intel recording an working earnings of $0.0B and an working margin of 0% for the group. Intel is attributing the drop to decrease gross sales of server/AI elements as buyer demand weakens, whereas Intel’s relative prices go up as an increasing number of server processors are shipped on the Intel 7 and 10ESF processes.

Intel in fact is on the cusp of delivery its long-delayed 4th Era Xeon Scalable (Sapphire Rapids) processors. So together with financial components, clients are ready for Intel’s next-generation {hardware}. Based on the corporate, they formally shipped their “high-volume” Sapphire Rapids SKUs in Q3, although because the chips nonetheless haven’t made it so far as getting ARK entries, it’s clear that they’re not absolutely launched fairly but. None the much less, Sapphire Rapids has reached PRQ (Product Launch Qualification), which is the purpose the place Intel is sufficiently joyful that yields are excessive sufficient and the efficiency is appropriate for silicon to be made for retail merchandise.

Intel’s remaining billion-dollar enterprise, the Community and Edge group (NEX) is the one actual vibrant spot on this quarter’s earnings launch. NEX income was up 14% year-over-year, reaching $2.3B.

Nonetheless, working earnings was down severely, dropping 85% to simply $75M for the quarter. Finally Intel noticed sturdy demand for his or her extra devoted networking merchandise similar to 5G and Ethernet, whereas the Xeon merchandise bought as a part of this phase had been hit with decrease demand.

Lastly, Intel’s “rising” sub-billion-dollar teams had been a blended bag. AXG revenues are up barely, however the group will proceed to lose cash for a few years to return till Intel has absolutely damaged into the market and is delivery consumer and server GPUs in massive volumes. Intel Foundry Companies is in an identical boat, as Intel continues to make the investments wanted to interrupt into the contract fab market in an enormous means. In any other case Mobileye was not solely worthwhile, however grew year-over-year. Intel has simply accomplished the Mobileye IPO this week, which though it’s now not a wholly-owned subsidiary of Intel, will nonetheless be a constructive affect on Intel’s earnings sheet as Intel nonetheless owns many of the spin-off.

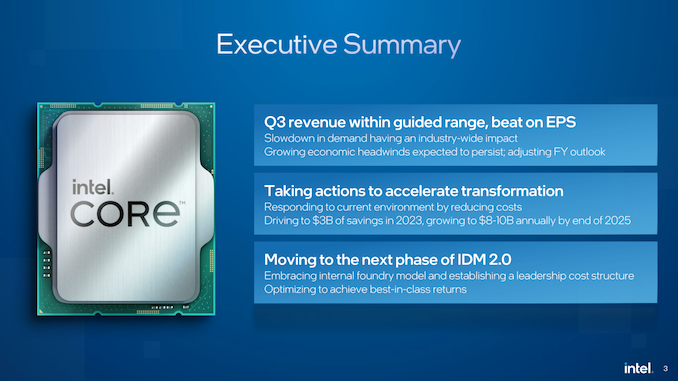

So what’s subsequent for Intel from right here? Although the corporate believes they’ve already weathered what would be the worst of their quarters from a profitability standpoint, Intel nonetheless want to arrange each itself and traders for the remainder of this bust cycle, and what’s (nonetheless) anticipated to be a basic financial recession.

So far as Intel’s personal projections go, the corporate is now calling for the 2022 fiscal 12 months to ship $63-$64B in income, which is down $2-$4B from their earlier (Q2) projection. Which is to say that the market goes to be softer than what Intel was pondering on the finish of Q2. If the brand new projections come to move, this may put revenues for the 12 months down 14%-16% from 2021.

This additionally implies that Intel’s gross margin won’t absolutely get better this 12 months. The gross margin for the 12 months is now projected to hit 47.5%, with This fall particularly anticipated to hit 45%. Intel nonetheless expects to show a revenue, however with income for This fall anticipated to say no as much as 28% from the year-ago quarter, they’re not out of this but.

On condition that Intel’s revenues and profitability aren’t anticipated to instantly get better, the corporate has made it clear that value reductions, together with layoffs, are on the best way. Particular layoffs haven’t but been introduced (a few of these will undoubtedly be introduced within the coming days, now that the earnings interval is over), however we all know that Intel took a $664M restructuring cost on this quarter with a purpose to enact these impending layoffs. At its present headcount, Intel has round 114,000 workers.

Altogether, Intel needs to save lots of $3B in prices for 2023, with that accelerating into 2025. And as capital expenditures being considered one of Intel’s greatest prices, that is additionally the place they are going to be making a few of their larger cuts. Based on the corporate, they’re going to proceed constructing fab shells, after which fill them with gear as demand dictates. This alone ought to enable the corporate to cut back capital expenditures by $2B for 2023.

Lastly, Intel can also be leaving the door open to any mergers, acquisitions, or divestitures that might profit the corporate because it appears to give attention to high-margin companies. There may be nothing particular right here to announce right this moment, however like every firm present process belt-tightening, Intel goes to be all of its choices.

General, whereas Q3’22 has not introduced Intel the identical form of beating because it took in Q2, the message from the corporate is that the challenges are removed from over. As famous by CEO Pat Gelsinger within the firm’s earnings launch: “we’re aggressively addressing prices and driving efficiencies throughout the enterprise”, as Intel works to realign itself to experience out the remainder of this bust cycle.

{kind=link}