Sascha Schuermann

On the subject of the medical trade, traders have a big number of methods to play the market. However this should not be a shock to anyone who understands simply how massive the medical house is relative to the U.S. economic system. As one of many largest parts of the economic system as measured by GDP, there should be many working components and numerous corporations devoted to offering the products and providers that make it function. One firm on this market that traders ought to a minimum of pay attention to is Baxter Worldwide (NYSE:BAX). Lately, the corporate engages in a wide range of actions, equivalent to offering peritoneal dialysis and hemodialysis, in addition to different dialysis therapies, options, and merchandise. It is also engaged in medicine supply actions and it even operates a chemical vitamin phase. From a purely basic perspective, the image for the agency has been a bit risky lately. Regardless of seeing income improve yr over yr, earnings and money flows have suffered. Because of this, shares of the corporate have taken one thing of a beating. Within the close to time period, I think that this might proceed. However given the place shares are priced, each on an absolute foundation and relative to different corporations on this market, I do assume that now is likely to be a very good time to price it a ‘purchase’.

A tricky time for Baxter Worldwide

The final time I wrote an article about Baxter Worldwide was in June of 2021. In that article, I lauded the corporate’s capability to develop, even throughout the worst of occasions. I felt as if it was a top quality chief in its market and that the worth of the inventory was not essentially unrealistic given the premium that traders would demand for such a high-quality enterprise. Besides, I felt as if the inventory was a bit too dear for me, main me to price it a ‘maintain’ to replicate my view that it will possible generate returns that will roughly match the broader market shifting ahead. Quick ahead to at present, and it appears as if I used to be a little bit too optimistic in my evaluation. Whereas the S&P 500 is down by 11.8%, shares of Baxter Worldwide have generated draw back of 29.2%.

Writer – SEC EDGAR Knowledge

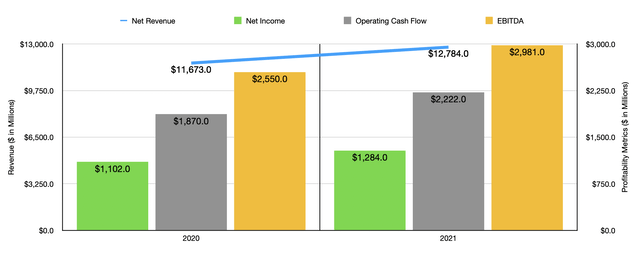

To be able to perceive why this return disparity exists, it is crucial that we dig into a number of the basic knowledge relating to the enterprise. Given the place the corporate was from a reporting perspective once I final wrote about it, we should always start with the 2021 fiscal yr as a complete. Throughout that yr, income got here in at $12.78 billion. That represents a large improve over the $11.67 billion generated in 2020. This roughly 10% improve yr over yr was pushed by a wide range of components. As an illustration, overseas foreign money fluctuations helped to the tune of three%. Along with that, two totally different acquisitions the corporate engaged in contributed $320 million in all to the corporate’s prime line progress. Robust demand for its choices was additionally one other key driver that various in nature from phase to phase. Because of the income improve, the corporate additionally noticed improved earnings. Internet revenue rose from $1.10 billion to $1.28 billion. Working money move rose from $1.87 billion to $2.22 billion. And EBITDA for the corporate improved from $2.55 billion to $2.98 billion.

Writer – SEC EDGAR Knowledge

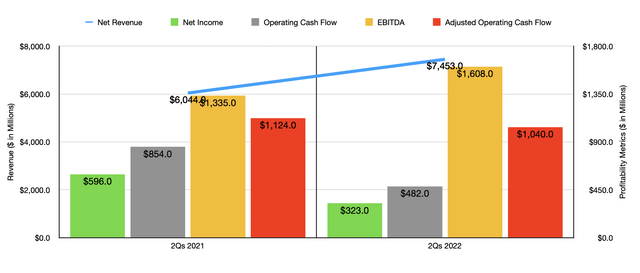

Heading into the 2022 fiscal yr, the image for the corporate modified much more, in some methods for the higher and in different methods for the worst. From a income facet, issues went rather well. Gross sales of $7.45 billion for the primary half of the yr got here in 23.3% increased than the $6.04 billion generated within the first half of 2021. This improve got here whilst overseas foreign money fluctuations impacted gross sales negatively to the tune of 4%. And in keeping with administration, the overwhelming majority of the advance got here from the corporate’s varied acquisitions, most notably its $10.5 billion buy of Hillrom, a transfer that by itself contributed about 24% to the corporate’s gross sales.

Usually, you’d anticipate to see profitability observe go well with. However that was sadly not the case. Internet revenue within the first half of 2022 totaled solely $323 million. This was down from the $586 million generated one yr earlier. There have been a number of points on this entrance. As an illustration, the corporate’s gross revenue margin shrank from 39.3% within the first half of 2021 to 37.6% the identical time this yr. This decline, administration mentioned, was pushed considerably by particular gadgets equivalent to elevated intangible asset amortization bills, acquisition and integration bills, regulatory points, and product-related gadgets. Related particular gadgets have been additionally instrumental in pushing the corporate’s promoting, common, and administrative prices up from 21.5% of gross sales to 27.2%. It will be one factor if the one ache we noticed was when it got here to web revenue. However we additionally noticed it with money move as properly. Within the first half of the yr, working money move was solely $482 million. This was down from the $854 million reported one yr earlier. Even when we modify for modifications in working capital, it will have fallen from $1.12 billion to $1.04 billion. In actual fact, the one profitability metric that improved yr over yr was EBITDA. In keeping with administration, that rose from $1.34 billion to $1.61 billion.

On the subject of the 2022 fiscal yr in its entirety, administration has supplied some fascinating enter. Precise earnings per share ought to are available in at between $1.82 and $1.92. However on an adjusted foundation, this might be between $3.60 and $3.70. To be extra cautious, I made a decision to make use of the official earnings per share when valuing the corporate. Primarily based on this knowledge, the corporate ought to generate web revenue this yr of round $950 million. If we assume that different profitability metrics will change based mostly on how they’ve been reported thus far this yr, then we should always anticipate adjusted working money move of $2.06 billion and EBITDA of $3.59 billion.

Writer – SEC EDGAR Knowledge

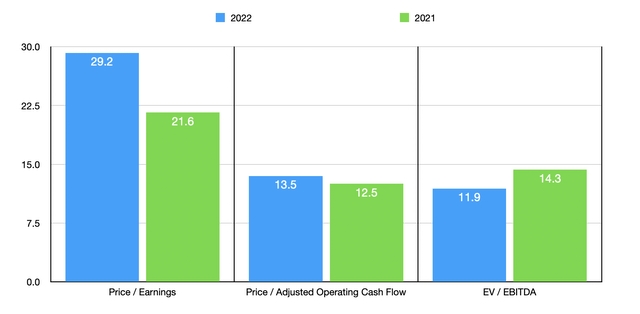

Primarily based on these estimates, the corporate can be buying and selling at a ahead price-to-earnings a number of of 29.2. Whereas that is lofty, the opposite profitability metrics are extra cheap. The value to adjusted working money move a number of needs to be 13.5, whereas the EV to EBITDA a number of ought to are available in at 11.9. Excluding the EV to EBITDA a number of, the pricing of the corporate does look dearer than what it will if we used knowledge from the 2021 fiscal yr. As a part of my evaluation, I additionally in contrast the corporate to 5 different corporations on this house. On a price-to-earnings foundation, these corporations ranged from a low of 33.2 to a excessive of 293.4. Utilizing the worth to working money move strategy, the vary was from 22.3 to 125.3. And utilizing the EV to EBITDA strategy, the vary was between 17.6 and 135.1. In all three circumstances, Baxter Worldwide was the most cost effective of the group.

| Firm | Worth / Earnings | Worth / Working Money Circulate | EV / EBITDA |

| Baxter Worldwide | 21.6 | 12.5 | 14.3 |

| IDEXX Laboratories (IDXX) | 76.5 | 75.4 | 54.4 |

| Olympus Corp (OTCPK:OCPNY) | 33.2 | 22.3 | 17.6 |

| ResMed (RMD) | 73.4 | 66.1 | 33.1 |

| Zimmer Biomet Holdings (ZBH) | 66.9 | 17.8 | 19.6 |

| DexCom (DXCM) | 293.4 | 125.3 | 135.1 |

Takeaway

Proper now, it appears to me as if Baxter Worldwide goes by one thing of a tough patch. Having mentioned that, I’ve little doubt that the long-term trajectory of the corporate would look optimistic. Gross sales proceed to rise and most of the pains that the corporate is experiencing on its backside line appear to be one-time in nature. I would not name the corporate a deep-value prospect by any means. However shares are positively on the cheaper facet of the spectrum, particularly relative to related corporations. So for these causes, I do really feel snug growing my score on the corporate from a ‘maintain’ to a ‘purchase’.

{kind=link}