Kawisara Kaewprasert/iStock by way of Getty Photographs

Introduction

Boston Properties, Inc. (NYSE:BXP) is an actual property funding belief (“REIT”) that owns workplace actual property throughout main developed cities throughout the USA. Whereas the corporate has a portfolio of excellent property with decrease emptiness charges than the comparables for related property sorts in related cities, the workplace market outlook stays notably weak and there are a selection of tendencies like rate of interest headwinds, work-from-home, and migration elements which might be more likely to persist. These elements give me some confidence that whereas the market costs in a extra rosy outlook that workplace actual property might take loads longer time to recuperate than what individuals anticipate. On this article, I am going to talk about my rationale for avoiding shares of Boston Properties regardless of its portfolio of high quality actual property and secure dividend and my causes for ranking the shares as a ‘maintain’.

Firm Overview

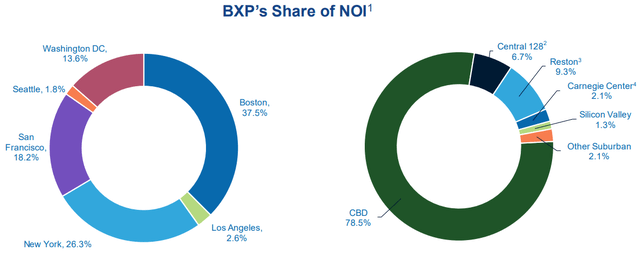

Boston Properties, Inc is a REIT that owns a number of workplace properties in main markets throughout the united States. It primarily operates in developed cities like Boston, Los Angeles, New York, San Francisco, Seattle, and Washington, DC, most principally in premium central enterprise district areas (78.5% of complete NOI comes from CBD areas). With a complete of 188 properties (a few of that are owned by the corporate and others which might be owned via joint ventures), the corporate has a complete of 53.3 million sq. ft of land to its title. Out of the 188 properties, 167 are places of work, 14 are retail properties, 6 are residential, and one is a resort.

Investor Presentation

Background

Total, I just like the geographic diversification that Boston Properties has. However after we take a look at the U.S. Workplace Market Outlook report by Colliers, these markets have fared fairly poorly. For instance, regardless of the nationwide common U.S. workplace emptiness charge at 16.9%, cities like Boston, Los Angeles, Seattle, Washington DC, and San Francisco have fared far worse with emptiness charges of 23.1%, 21.8%, 25.4%, 18.4%, and 27.9%, respectively for Downtown Class A. Solely New York has a greater emptiness charge than the nationwide common at 13.1%.

U.S. Workplace Market Emptiness Charges (Colliers)

Take into account that these charges are for Downtown Class A, which most of Boston Properties’ places of work are. Apparently, in most of those markets (Boston, Los Angeles, San Francisco), the Downtown Class A properties have larger emptiness charges than the suburban workplace properties. So regardless of the notion that Downtown Class A is larger high quality, it is truly been hit the toughest and has confirmed to be much less resilient than suburban over the previous couple of years. One constructive for Boston Properties is that these markets are typically extra liquid, with Manhattan, Los Angeles, and Boston having the best energetic gross sales market by quantity in 2023 at $4.6 billion, $3.6 billion, and $2.7 billion.

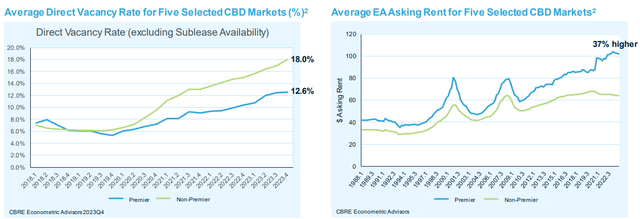

However if you evaluate Downtown Class A (premier) to the remainder of Downtown (non-premier), we will see from the graph under that there is been a widening divergence between emptiness charges in addition to rents between premier and non-premier property, each knowledge factors favoring premier workplace properties. This knowledge, collected by CBRE and introduced within the firm’s investor presentation, is in keeping with the Colliers report, however the findings are fascinating if you evaluate Downtown Class A to the remainder of Downtown and Downtown Class A to suburban.

Investor Presentation

Once we evaluate Boston Properties’ emptiness charges to the remainder of workplace, it does not look so unhealthy. Boston Properties’ portfolio is 88% occupied so the emptiness charge is round 12%, implying that its been typically extra resilient and certain has a greater high quality portfolio.

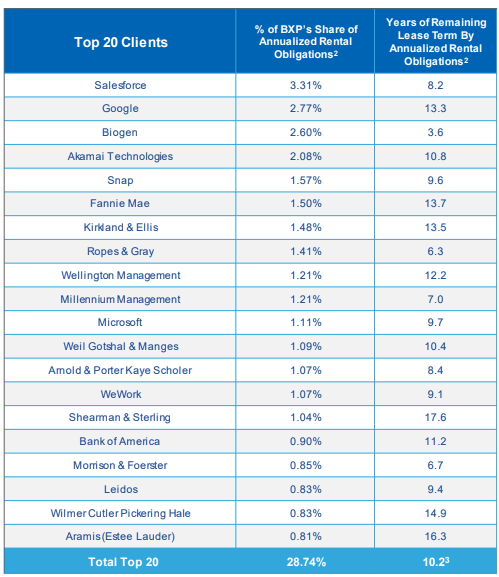

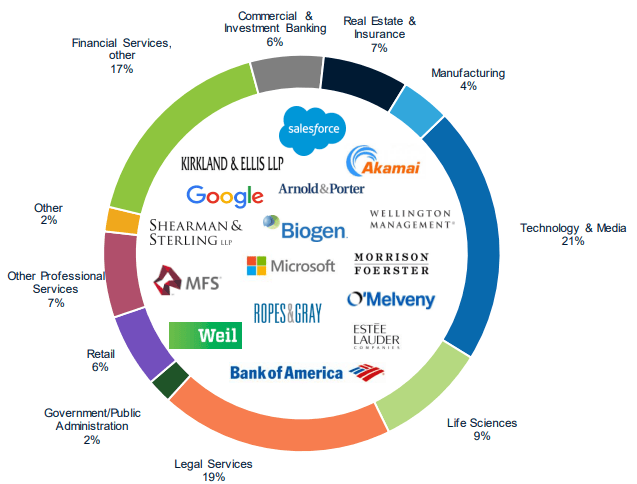

We see this clearly with the tenant mixture of the portfolio. Nobody consumer makes up greater than 4% of the corporate’s rental revenues and most of those firms are Fortune 500 firms like Salesforce (CRM), Google (GOOG), and Microsoft (MSFT), to call a number of.

High Tenants (Investor Presentation)

Even amongst the top markets that these firms serve, it isn’t simply know-how firms or simply firms in a single business. Whereas know-how and media does make the most important portion at 21% of rental revenues, monetary companies, authorized companies, and life sciences are all effectively represented so there is not a lot focus threat right here.

Trade Diversification (Investor Presentation)

Outlook

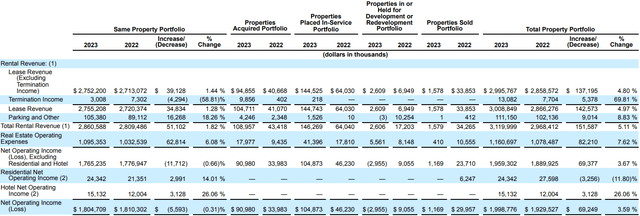

When taking a look at the newest This fall and full year outcomes for Boston Properties reported earlier this March, the corporate reported NOI of just below $2 billion which represented a rise of three.59% 12 months over 12 months. Most of this was because of new properties added to the portfolio, as internet working earnings on a identical property portfolio foundation was primarily unchanged (down 0.31%). The brand new properties have been primarily attributable to a few important ones, notably Madison Centre (Seattle), 125 Broadway (a $603 million life sciences property in Boston), and Santa Monica Enterprise Park. Collectively, these added 2.2 million sq. ft to the property portfolio, partially offset by some workplace/flex and residential properties which have been offered.

Latest Outcomes (Firm Filings)

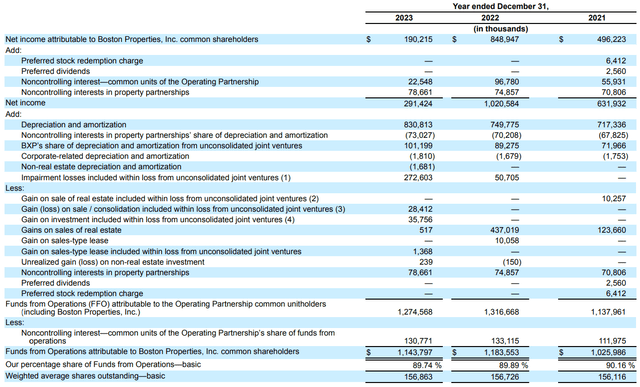

From a funds from operations (FFO) perspective, Boston properties truly noticed a decline of three.4% from $1.18 billion in 2022 to $1.14 billion for 2023. Dividing the $1.18 billion by the weighted common shares excellent on the quarter finish date offers us an FFO per share worth of $7.29, which was additionally 3.4% on a per share foundation in opposition to final 12 months’s $7.55. So general, Boston Properties appears to have carried out according to what we would have anticipated based mostly on the findings from business stories about workplace.

FFO Breakdown (Firm Filings)

Looking into the long run, it is onerous to discover a concrete catalyst that can propel Boston Properties shares larger. For one factor, administration wasn’t so upbeat on the earnings name, forecasting simply $7.28 per share in FFO, implying zero progress for 2024. This steering consists of assumptions about numerous properties reaching completion in the course of the 12 months so I’d anticipate that on a identical property portfolio foundation, we’re more likely to see declines once more for the 12 months.

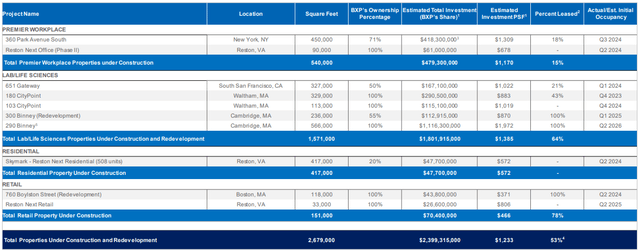

Improvement Pipeline (Investor Presentation)

One of many largest contributing elements by way of how workplace actual property will carry out over the following few years would be the impression of rates of interest and what occurs to the yield curve. In CBRE’s U.S. Actual Property Outlook report, the actual property companies agency sees workplace performing negatively, however vacancies ought to peak at 19.8% someday later this 12 months. Based mostly on this, actual property values are more likely to decline 5% to fifteen% as cap charges rise.

One factor I discovered fascinating was that the markets which might be anticipated to carry out effectively are Las Vegas, Miami, and Nashville (markets that Boston Properties does not have publicity to) and the markets which might be anticipated to do poorly embody lots of the markets that the REIT is positioned in. In Las Vegas for instance, the emptiness charges have already began to slender with constructive internet absorption. To me, there are doubtless higher markets to be uncovered to, particularly contemplating the exodus of excessive earnings earners leaving attributable to excessive taxes and excessive value of residing. This additionally exhibits up in census knowledge which exhibits definitively that the inhabitants in markets like New York is in actual fact declining.

In my opinion, I believe the pandemic has doubtless modified migration tendencies and elements like work at home are right here to remain. Numerous jobs (together with my very own) permit people to work in hybrid working environments or fully distant. Based on Forbes, on the finish of 2023, about 12.7% of full-time staff work at home, whereas 28.2% work a hybrid mannequin. By 2025, its projected that 22% of the workforce will work remotely. That does not bode effectively for workplace actual property and positively not for Boston Properties.

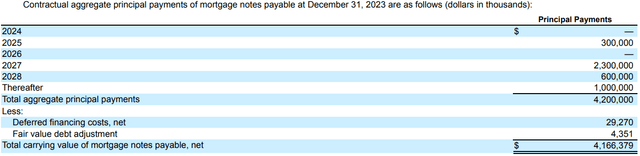

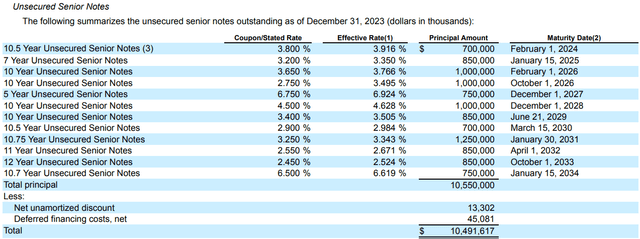

As for the corporate’s steadiness sheet, Boston Properties is extremely levered. The principle gadgets so far as debt goes is $4.2 billion in mortgage notes, $10.5 billion in senior unsecured notes, and an unsecured time period mortgage for $1.2 billion for complete long-term debt of $15.9 billion ex-leases. With $1.6 billion of money, this brings the online leverage to about 7.4x and the fastened cost protection ratio to about 2.5x. This appears fairly excessive threat, nevertheless administration famous that they’re comfy with the present leverage within the capital construction and do not anticipate growing its internet leverage ratio from right here. As for the maturity cycle and credit score rankings, many of the debt is laddered and has been secured at fastened charges. The credit score outlook in response to S&P and Moody’s is secure with an A- and Baa2 ranking, respectively (supply: TD Securities).

Mortgage Notes Payable (Firm Filings)

Unsecured Senior Notes (Firm Filings)

Valuation

Based mostly on the 13 analysts who cowl the inventory, there are 5 ‘purchase’ rankings and eight ‘maintain’ rankings on Boston Properties with a median value goal of $74.00, a excessive estimate of $80.00, and a low estimate of $67.00 (supply: TD Securities). From the present value to the common value goal one 12 months out, this means potential upside of 17.0%, not together with the 6.2% yield. With 23.2% complete return potential, evidently regardless of the predominantly maintain rankings that analysts are bullish on the near-term upside of the inventory.

Total, I disagree with the analysts’ consensus right here, noting that many of the goal revisions upwards have been attributable to a number of enlargement over the previous couple of quarters, moderately than ranking upgrades and changes upwards in FFO. Thus, I do not see a motive to assign the corporate the next a number of from right here on out. Regardless of the FFO outlook being flat for 2024 as per administration’s steering, the inventory is up 25% within the final twelve months. This offers it a ahead a number of of 8.6x, which appears affordable, particularly in opposition to friends like Vornado Realty Belief (VNO), Kilroy Realty (KRC), and SL Inexperienced (SLG) who’ve P/FFO multiples of 9.2x, 7.8x, and eight.2x, respectively, so it does commerce at a small premium to the group. Traders ought to take into account nevertheless that FFO is unlikely to develop a lot from right here.

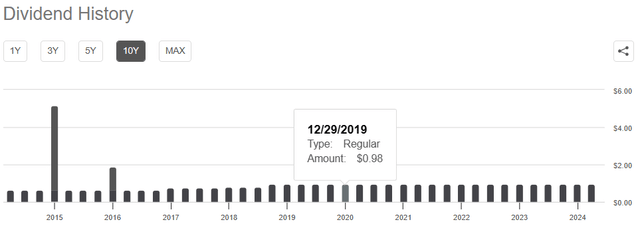

Boston Properties 6.2% dividend yield seems to be supported sufficiently with FFO having not been minimize in any respect in the course of the pandemic. Nevertheless, with an over leveraged steadiness sheet and restricted FFO progress, it is also unlikely we’ll see dividend will increase going ahead. Till we see a significant rebound in workplace actual property, I am not assured within the REITs capability to lift its dividend.

Looking for Alpha

Conclusion

In abstract, Boston Properties appears to personal high quality property given its emptiness charges are decrease than Downtown Class A properties in comparable markets. Nevertheless, with a number of elements together with work-from-home, rates of interest, and migration tendencies, workplace actual property, notably within the markets that BXP is in, are being hit loads more durable which makes me assume {that a} restoration is unlikely to come back any time quickly. With the corporate’s shares having rallied over the previous 12 months, evidently the market is pricing in a extra rosy outlook. As well as, whereas the corporate does not appear costly at 8.6x P/FFO, there is not a lot room for FFO progress and administration’s steering suggest a decline in NOI on a comparable property foundation in 2024. As such, regardless of its superior property portfolio with diversified and long-term tenants and my confidence within the REIT’s capability to keep up its dividend, I charge shares of BXP as a ‘maintain’ till we begin to see indicators of enchancment.

{kind=link}