Joa_Souza/iStock Unreleased through Getty Pictures

Be aware: I beforehand lined Braskem (NYSE:BAK). In my earlier take, I highlighted the potential of the ADNOC acquisition, bringing a 100% upside potential. Since my word, BAK’s shares have moved up 51%. In in the present day’s article, I’ll talk about the later updates on the deal and discusses BAK’s ranking.

Braskem is a kind of uncommon alternatives the place all the pieces appears so negatively aligned. Counter intuitively, the draw back danger is way decrease in such instances as a result of all nightmare eventualities are already priced in. After I wrote my article on BAK, the risk-reward ratio was wonderful, at BAK’s share worth round $7. The current inventory worth is $10.31. Is the BAK share purchase at the moment worth?

Braskem deal updates

BAK stays within the highlight for potential acquisition. Along with ADNOC (Abu Dhabi Nationwide Oil Firm), just a few others are contemplating the chance to purchase the sixth-largest chemical firm on the planet. Saudi Arabian firm SABIC (Saudi Fundamental Industries Corp.) was rumored as a possible acquirer. SABIC’s main shareholder is Saudi Aramco, which has 70% possession. Later in February, SABIC launched a press release denying its curiosity in buying BAK.

One other Center East candidate in Kuwait’s Petrochemical Industries Firm (PIC). Throughout his journey to the area, Petrobras CEO Jean Paul Prates met with the oil business executives and shared his intentions for future partnerships. PIC was among the many names referred to. Nonetheless, till now, PIC has not but submitted a proper proposal.

For now, solely ADNOC is progressing towards the acquisition. In the meantime, Petrobras (PBR) can also be getting concerned in due diligence. PBR already owns 47% of BAK.

In February, ADNOC acquired a 24.9% stake in OMV. Many buyers interpret this transfer negatively as associated to the BAK acquisition. I’ve a special opinion. ADNOC and Mubadala Fund (an Abu Dhabi sovereign fund and main shareholder in ADNOC) are flush with money plus ADNOC doesn’t have operations in Western Hemisphere. Therefore, BAK appears tempting proposition.

Mataripe Refinery (RLAM) is perhaps concerned to hurry up the deal. RLAM accounts for about 10% of Brazil’s whole oil refining capability. Petrobras CEO Prates affirms the corporate’s intentions to barter with Mubadala to promote the refinery. In 2021, Mataripe was offered to the earlier Mubadala administration for $1.65 billion.

Then again, ADNOC (and Mubadala) search alternatives to park its money. BAK is amongst them. In my earlier word, I identified the political dynamics because the decisive issue. I nonetheless maintain the identical view. The deal closely is determined by Lula’s administration’s will to proceed. A minimum of for now, the politics act as a tailwind, rising the chances of a profitable deal.

Beneath is a quote from an article on Lula’s plans for the Brazilian oil business.

Lula needs Petrobras to carry on to extra of its refining capability to displace gas imports. The primary aim is to test pump costs for the good thing about native customers, who’ve been clobbered by double-digit inflation this yr.

“There’s a consensus throughout the Lula camp that they wish to shut the hole between home (gas) manufacturing and imports,” says Mark Langevin, a senior advisor to Horizon Entry Consulting and former coverage advisor to the president-elect. “They wish to make it possible for home costs replicate the price of manufacturing and never the pursuits of huge Petrobras shareholders — together with the federal authorities — that need massive dividends.”

The Brazilian President Lula expressed implicitly its help to take again Mataripe. In my view, Mubadala/ADNOC and the Brazilian authorities appear to have what the opposite facet needs. So, the chances for profitable ADNOC/BAK deal are excessive.

Stability sheet

In December 2023, BAK canceled its credit standing providers. Beneath is a remark from a earlier article on what it would imply:

For instance, a credit standing is perhaps withdrawn if the corporate is anticipated to be dissolved or merged with one other entity. In fact, this assertion doesn’t imply ADNOC (or whoever) will compete within the take care of BAK. It is perhaps one thing else—for instance, the difficulty in Maceio.

In February, BAK introduced its credit score rating by S&P, BB+, with a secure outlook. Earlier than canceling its credit standing providers, BAK scored BBB- with a unfavourable outlook.

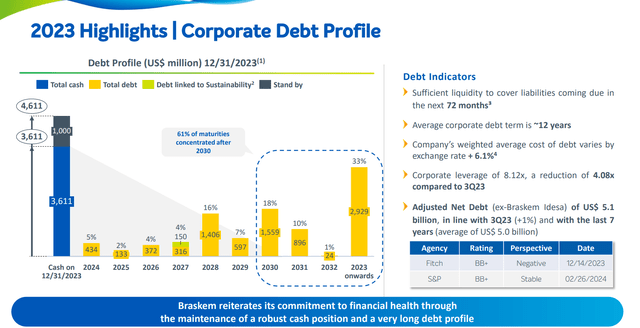

BAK’s liquidity place is greater than adequate. The corporate holds $3.9 billion in money and has $12.3 billion in whole debt (together with $609 million lease agreements), as proven within the desk beneath from 4Q23 presentation.

BAK 4Q23 presentation

61% of the debt maturities come after 2030. In 2024, the corporate should repay $434 million, and in 2025, $133 million.

As I discussed in my final word on BAK, it is a speculative place associated to the acquisition of BAK. So, my main concern within the firm’s financials is its liquidity, i.e., its potential to cowl its debt installments. The income, earnings, and revenue margins don’t present decisive data in that case. In conclusion, BAK’s liquidity is greater than sufficient to cowl its obligations within the coming years, mitigating the chance of untimely chapter.

Traders Takeaway

A major danger isn’t respecting tag-along rights. Which means all minor shareholders don’t get the upside of the deal. Given the final information, the uncertainties round tag-along rights are diminishing. In February 2024, Petrobras exercised its rights when it offered its 18.8% share in UEG Auracaria to Ambar Energia SA.

The political surroundings stays supportive of the take care of ADNOC. As identified, the Mataripe refinery could velocity up the acquisition. Lula’s administration needs to extend Brazil’s refinery capability, whereas ADNOC needs to broaden its enterprise globally by shopping for high quality property for cents on the greenback.

The Maceio catastrophe carries some dangers that may undermine my thesis. The implication is twofold. Firstly, ADNOC may cancel the deal due to the Maceio situation, saying they don’t wish to be related to the accident by investing in BAK. In my view, that is attainable, although not a possible state of affairs.

Then again, the political facet of Maceio’s accident could undermine the deal. In Marich 2024, the CPI (Parliamentary Fee of Inquiring ) began a probe towards BAK. The end result of the probe will contain native politics. It is determined by how far the investigation reaches. It could flip the tide even among the many high-ranking officers, rising the uncertainties across the take care of ADNOC.

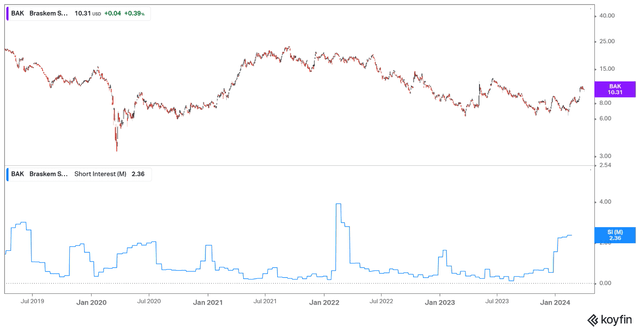

Extra conviction to my thesis provides BAK’s brief positioning. It’s not extraordinarily excessive, but it surely appears ok for a brief squeeze in case of optimistic information concerning the BAK/ADNOC deal.

Koyfin

Quick curiosity isn’t a prerequisite for a Purchase. Nonetheless, it provides worth to the thesis when mixed with particular conditions. A chief instance of overtly brief positioning was ZIM delivery in December 2023 and PGM (platinum group metals), particularly palladium. ZIM, particularly, made the extreme bull transfer, propelled by the primary Houthis assaults.

Braskem is a particular state of affairs play, betting on ADNOC’s acquisition of BAK. Since my earlier report, the celebrities have lined up for a profitable deal. The worth motion confirms that, since December, the value has jumped by 50%.

With the anticipated takeover worth by ADNOC within the vary of $14-$15/share and the current inventory worth of $10.3, the risk-reward isn’t skewed in our favor. BAK has satisfactory liquidity to service its money owed whereas ready for the deal competitors. I count on volatility forward following the CPI probe, so if the value drops beneath $9.0, I could add extra measurement. Till then, I sit tight. I give BAK a maintain ranking.

{kind=link}