yujie chen/iStock Editorial through Getty Photographs

Funding thesis

BT Group plc’s (OTCPK:BTGOF) shares have considerably underperformed its world friends, stemming from a weakening and unstable UK financial system. While valuations are low, with the shortage of any optimistic catalysts within the close to time period, we see no speedy causes to take a position. We fee BT Group shares as impartial.

Fast primer

BT Group is the world’s oldest telecommunications, with roots courting again to 1846. It stays the UK’s largest shopper cellular (with the EE model), fastened, and converged communication supplier with a relationship with over 45% of UK households. It has enterprise and world service divisions and operates a fixed-access community referred to as Openreach, which wholesales connectivity to different communication suppliers.

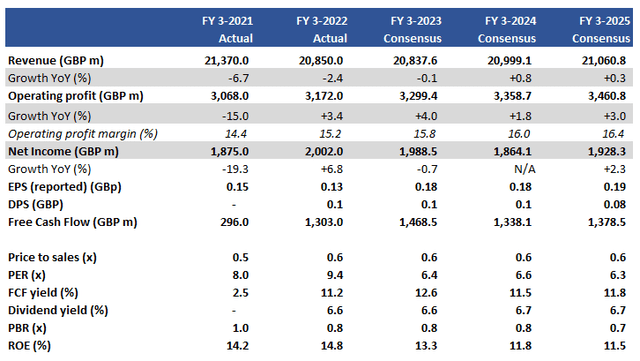

Key financials with consensus forecasts

Key financials with consensus forecasts (Firm, Refinitiv)

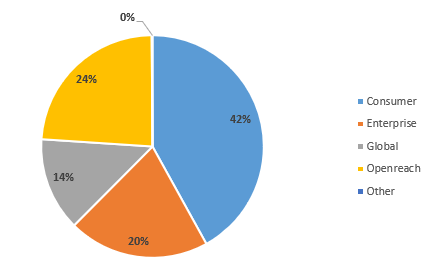

Gross sales break up by section H1 FY3/2023

Gross sales break up by section H1 FY3/2023 (Firm)

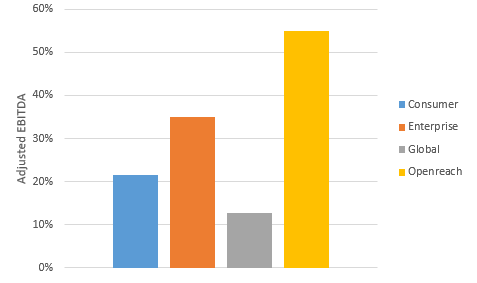

Adjusted EBITDA margin per section H1 FY3/2023

Adjusted EBITDA margin per section H1 FY3/2023 (Firm)

Our targets

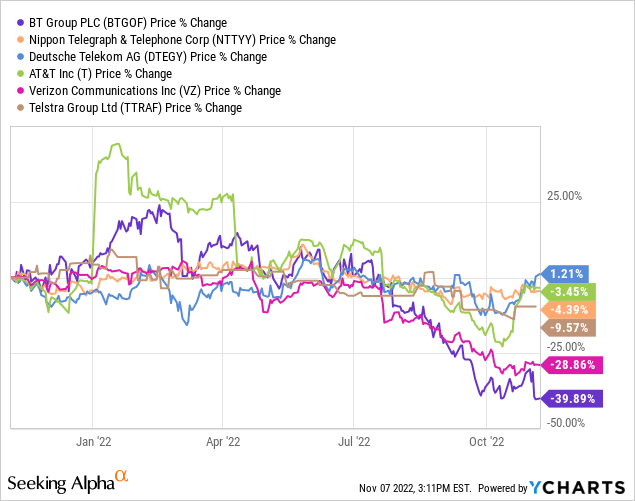

BT Group has skilled notable underperformance YTD versus its world peer group, with Deutsche Telekom (OTCQX:DTEGY), AT&T (T), and NTT (OTCPK:NTTYY) displaying comparatively robust outperformance. The telecommunication sector is ex-growth however steady and tends to carry out no matter enterprise cycles, influenced extra by know-how with next-generation community roll-outs. Historically seen as a conservative space to take a position, we need to examine whether or not BT Group is engaging given its vital share worth correction.

Restricted positives in H1 FY3/2023 outcomes

The UK financial system is below intense stress from exogenous elements such because the Russian invasion of Ukraine, and by capturing itself within the foot as the federal government launched after which retracted a ‘mini-budget’ that blasted up borrowing prices and broken the nation’s monetary market popularity. BT typically describes itself as underpinning financial progress within the UK, however sadly, it seems to be struggling because of being so integral to its house market. A tightening fiscal coverage announcement can be anticipated subsequent week on seventeenth November 2022.

H1 FY3/2023 outcomes disenchanted the market with income earlier than tax falling 17.6% YoY, however feedback made about inflation (notably power) driving the necessity for accelerated value financial savings have been a serious unfavorable. The unique value financial savings goal has been raised from GBP2.5 billion/USD2.1 billion to GBP3.0 billion/USD2.6 billion by the tip of FY3/2025. The enterprise is incapable of driving sustainable earnings in its present type. Imposing value cuts shall be very troublesome to execute given inflationary pressures (rising power prices are exhausting to hedge), in addition to workforce unrest over pay, which in the summertime led to strikes and clients lacking out on getting broadband connections to their properties.

Free money circulation at interim fell to GBP64 million/USD55 million from GBP360 million/USD313 million YoY as capex rose GBP705 million/USD613 million (web page 15) as efforts proceed to increase its FTTP (fibre-to-the-premises) by Openreach for its fastened community construct and connections. BT is investing GBP15 billion/USD13 billion to assist Openreach’s FTTP community attain 25 million UK premises by December 2026 (at the moment at 8.8 million), of which 6.2 million of these shall be in rural or semi-rural areas. Openreach is probably the most worthwhile enterprise by EBITDA margin for BT and is essential for its future success. Nonetheless, there may be nonetheless some strategy to go earlier than capex ranges can start to normalize.

Rising debt and wish for persistence

Internet debt ranges elevated by GBP801 million/USD696 million to GBP19.0 billion/USD16.5 billion in H1 FY3/2023, leading to a internet debt-to-equity ratio of 1.2x which isn’t too excessive danger, however greater than extra liquid friends resembling NTT on 0.9x who’re additionally asset-rich with long run investments. The debt schedule reveals a big spike in maturities in FY3/2026 (web page 51), highlighting that BT’s financing prices are going to extend over the medium time period. Increasing leverage and rising financing prices usually are not optimistic however with a present curiosity protection ratio of three.8x, there may be nonetheless room for maneuver.

There usually are not many positives to speak about BT within the quick time period; administration continues to promote the long-term story whereby free money circulation expands by a minimum of GBP1.5 billion/USD1.3 billion from FY3/2023 to FY3/2031, successfully doubling in eight years. The important thing driver stays the roll-out of FTTP, promoting converged cellular/fastened companies with value-add companies on prime to decrease churn and growing ARPA (common income per account) and capex is peaking this 12 months at round GBP5.0 billion/USD 4.3 billion. The important thing query seems to be whether or not the enterprise can navigate the subsequent few years financing its FTTP roll-out efficiently, while working its legacy companies with out an excessive amount of disruption. The enterprise setting will stay difficult with the Financial institution of England forecasting a 2-year recession from the summer season of CY2022.

Valuation

Consensus forecasts estimate flat progress into FY3/2024 and FY3/2025, which can look too optimistic given the corporate is embarking on value reductions to fight margin stress. Adverse sentiment could also be coming from the truth that earnings could decline, and dividends per share could also be minimize regardless of the payout coverage based mostly on sustaining or rising it YoY. The present estimated dividend yield of 12% seems barely stretched however is a lovely degree of return.

Dangers

Upside danger comes from BT managing to chop prices efficiently, demonstrating a restoration profile in earnings. The FTTP roll-out might speed up and the gross sales combine might begin to enhance quicker than anticipated.

Draw back danger comes from inflationary value pressures growing going forwards, each for power in addition to workers wages which can dampen margins. The price-of-living disaster might lead to falling ARPA and growing buyer churn, for each retail shoppers and enterprises.

Conclusion

Regardless of the speedy difficulties of value inflation confronted by BT Group, we really feel that draw back danger is proscribed given the current share worth correction. Nonetheless, there isn’t a simple approach for the corporate to submit a restoration profile, and it must navigate a tough 2 years till the FTTP undertaking nears completion and capex demand start to fall again. Present valuations are in worth territory with PBR 0.8x and dividend yield above 10%, however we count on to see weakening leads to the subsequent 6-12 months. With no speedy causes to take a position, we fee BT Group plc shares as impartial.

{kind=link}