Sezeryadigar/E+ through Getty Pictures

I do know that worth buyers really feel a little bit of frustration proper now.

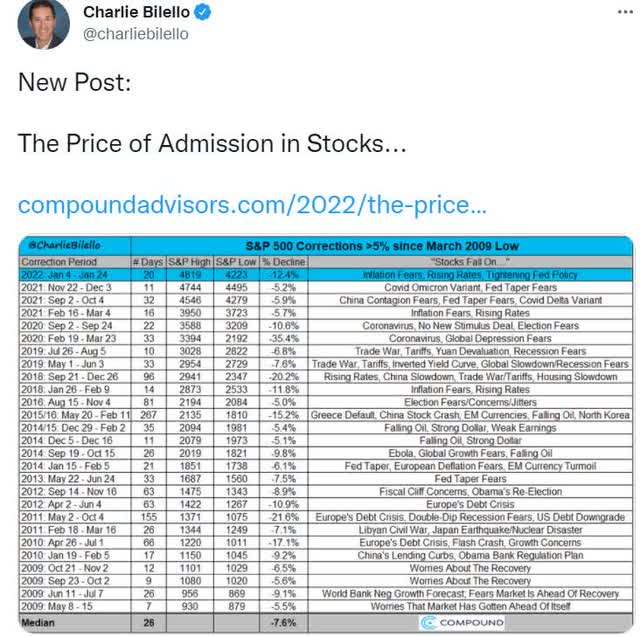

Charlie Bilello

What with this correction to this point seeing a peak 12.4% decline and now the market seems to be ripping increased once more.

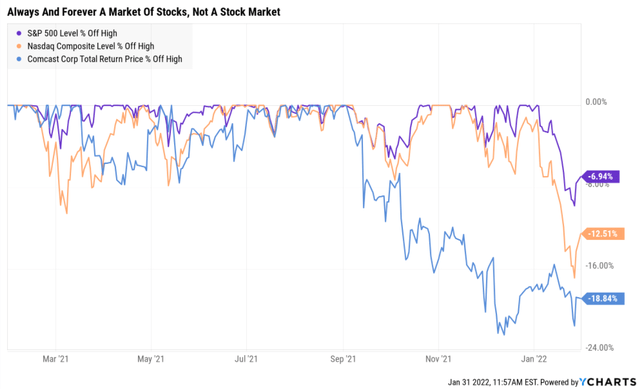

YCharts

The market is now simply 7% from its highs and tech shares are, at the very least for the second, screaming increased.

Does this imply the “purchase the dip” crowd has received? It is dependent upon your time-frame.

- within the long-term purchase the dip is at all times a good suggestion

- as a result of shares at all times go up in case your time-frame is lengthy sufficient

In 2022 it is potential that we’ll nonetheless see a 15% and even 20% correction, although it may not occur within the first half of the 12 months.

However guess what? Wonderful dividend progress blue-chips like Comcast (CMCSA) are nonetheless in a bear market and NOT screaming increased… but.

Do not forget that it is at all times and perpetually a market of shares, not a inventory market.

So let me inform you why Comcast is considered one of my prime precedence correction watchlist firms and the three the explanation why you would possibly wish to purchase this hyper-growth Tremendous SWAN now earlier than everybody else does later.

Cause 1: World-Class High quality You Can Belief

The Dividend King’s total high quality scores are primarily based on a 233 level mannequin that features:

-

dividend security

-

stability sheet power

-

credit score scores

-

credit score default swap medium-term chapter threat information

-

quick and long-term chapter threat

-

accounting and company fraud threat

-

profitability and enterprise mannequin

-

progress consensus estimates

-

value of capital

-

long-term risk-management scores from MSCI, Morningstar, FactSet, S&P, Reuters’/Refinitiv and Simply Capital

-

administration high quality

-

dividend pleasant company tradition/earnings dependability

-

long-term complete returns (a Ben Graham signal of high quality)

-

analyst consensus long-term return potential

It truly contains over 1,000 metrics in the event you depend every part factored in by 12 ranking businesses we use to evaluate elementary threat.

How do we all know that our security and high quality mannequin works effectively?

Through the two worst recessions in 75 years, our security mannequin predicted 87% of blue-chip dividend cuts in the course of the final baptism by hearth for any dividend security mannequin.

How does CMCSA rating on one of many world’s most complete and correct security fashions? Very effectively certainly.

Dividend Security

| Ranking | Dividend Kings Security Rating (145 Level Security Mannequin) | Approximate Dividend Reduce Danger (Common Recession) |

Approximate Dividend Reduce Danger In Pandemic Stage Recession |

| 1 – unsafe | 0% to twenty% | over 4% | 16+% |

| 2- under common | 21% to 40% | over 2% | 8% to 16% |

| 3 – common | 41% to 60% | 2% | 4% to eight% |

| 4 – secure | 61% to 80% | 1% | 2% to 4% |

| 5- very secure | 81% to 100% | 0.5% | 1% to 2% |

| CMCSA | 93% | 0.5% | 1.4% |

Lengthy-Time period Dependability

| Firm | DK Lengthy-Time period Dependability Rating | Interpretation | Factors |

| Non-Reliable Corporations | 18% or under | Poor Dependability | 1 |

| Low Dependability Corporations | 19% to 57% | Under-Common Dependability | 2 |

| S&P 500/Business Common | 58% (58% to 67% vary) | Common Dependability | 3 |

| Above-Common | 68% to 77% | Very Reliable | 4 |

| Very Good | 78% or increased | Distinctive Dependability | 5 |

| CMCSA | 76% | Very Reliable | 4 |

Total High quality

| CMCSA | Remaining Rating | Ranking |

| Security | 93% | 5/5 very secure |

| Enterprise Mannequin | 80% | 3/3 extensive moat |

| Dependability | 76% | 4/5 very reliable |

| Whole | 86% | 12/13 Tremendous SWAN |

CMCSA is a medium-risk Tremendous SWAN with long-term risk-management within the fifty fifth business percentile.

CMCSA: 92nd Highest High quality Grasp Record Firm (Out of 509) = 82nd Percentile

The DK 500 Grasp Record contains the world’s highest high quality firms together with:

-

All dividend champions

-

All dividend aristocrats

-

All dividend kings

-

All world aristocrats (akin to BTI, ENB, and NVS)

-

All 13/13 Extremely Swans (as near good high quality as exists on Wall Road)

- 43 of the world’s finest progress shares (on its strategy to 50)

CMCSA’s 86% high quality rating means its related in high quality to such blue-chips as

- Philip Morris Worldwide (PM) – dividend king

- Visa (V)

- Linde (LIN) – dividend aristocrat

- Abbott Labs (ABT) – dividend king

- Lockheed Martin (LMT)

- Altria (MO) – dividend king

- Realty Revenue (O) -dividend aristocrat

- Mastercard (MA)

- Walmart (WMT) – dividend aristocrat

- NVIDIA (NVDA)

Mainly, even among the many world’s highest high quality firms, CMCSA is increased high quality than 82% of them.

What makes Comcast so top quality?

Comcast is made up of three elements. The core cable enterprise owns networks able to offering tv, Web entry, and cellphone companies to roughly 60 million U.S. properties and companies, or almost half of the nation. About 55% of the properties on this territory subscribe to at the very least one Comcast service.

Comcast acquired NBCUniversal from Basic Electrical in 2011. NBCU owns a number of cable networks, together with CNBC, MSNBC, and USA, the NBC broadcast community, a number of native NBC associates, Common Studios, and several other theme parks. Sky, acquired in 2018, is the dominant tv supplier within the U.Ok. and has invested closely in unique and proprietary content material to construct this place. The agency can also be the most important pay-television supplier in Italy and has a presence in Germany and Austria.” – Morningstar

It is a extremely diversified media conglomerate.

- a telecom big (56% of gross sales)

- a media big (27% of gross sales)

- and a theme parks big (16% of gross sales)

One which has an distinctive monitor file of delivering market-smashing dividend progress and complete returns.

- $1 invested into CMCSA in 1972 on the IPO value is now price $381 adjusted for inflation

- 12.9% CAGR actual returns vs 6.5% CAGR S&P 500

- 2X the annular returns = nearly 18X the wealth over 49 years

Enterprise Replace

Comcast Ramps Up Peacock Funding as Broadband Development Slows; Shares Engaging…

The agency once more posted a drop in broadband buyer additions in the course of the interval (212,000 versus 538,000 a 12 months in the past), which administration continues to ascribe to a slowdown in housing exercise…

Administration introduced that it’ll enhance funding to increase the agency’s community to extra new places in 2022 and past, which we consider is a great, if overdue, use of capital…

NBCU plans to double Peacock content material funding to $3 billion in 2022, ramping to $5 billion yearly over the subsequent couple years…

Given the content material and sources at NBCU’s disposal, we consider it may well catch up, however stiff competitors for purchasers and content material will seemingly damage profitability over the subsequent couple years greater than we had anticipated…

Whole NBCU income elevated 26% 12 months over 12 months in the course of the quarter, with the theme park enterprise delivering spectacular outcomes, however rising content material prices pulled the phase’s EBITDA margin right down to 13.7% from 18.5% final 12 months.” – Morningstar

Peacock is way behind within the streaming wars, with 24.5 million subscribers, in comparison with effectively over 200 million for Netflix (NFLX), and Amazon (AMZN), and Disney’s nearly 120 million.

Even AT&T’s (T)’s HBO Max has about 2.5X as many subscribers.

Nonetheless, streaming is the long run and CMCSA has the monetary sources to at the very least put up struggle on this vital a part of its enterprise.

CMCSA Credit score Rankings

| Ranking Company | Credit score Ranking | 30-12 months Default/Chapter Danger | Likelihood of Dropping 100% Of Your Funding 1 In |

| S&P | A- secure | 2.50% | 40.0 |

| Fitch | A- secure | 2.50% | 40.0 |

| Moody’s | A3 (A- equal) secure | 2.50% | 40.0 |

| Consensus | A- secure | 2.50% | 40.0 |

(Sources: S&P, Moody’s, Fitch)

That is an A-rated firm with very low elementary threat.

CMCSA Leverage Consensus Forecast

| 12 months | Debt/EBITDA | Internet Debt/EBITDA (3.5 Or Much less Protected In accordance To Credit score Ranking Businesses) |

Curiosity Protection (4+ Protected) |

| 2020 | 3.37 | 2.99 | 3.81 |

| 2021 | 2.84 | 2.52 | 5.02 |

| 2022 | 2.49 | 2.24 | 5.92 |

| 2023 | 2.44 | 2.14 | 6.76 |

| 2024 | 2.10 | 1.97 | 7.27 |

| 2025 | 1.86 | 1.85 | 7.61 |

| Annualized Change | -11.14% | -9.14% | 14.82% |

(Supply: FactSet Analysis Terminal)

The stability sheet is getting steadily stronger, with debt declining steadily and money stream rising at 7% with money flows at 7% to 12%.

CMCSA Stability Sheet Consensus Forecast

| 12 months | Whole Debt (Thousands and thousands) | Money | Internet Debt (Thousands and thousands) | Curiosity Price (Thousands and thousands) | EBITDA (Thousands and thousands) | Working Revenue (Thousands and thousands) | Curiosity Price |

| 2020 | $103,760 | $11,740 | $92,020 | $4,588 | $30,826 | $17,493 | 4.42% |

| 2021 | $98,270 | $9,718 | $87,158 | $4,193 | $34,605 | $21,055 | 4.27% |

| 2022 | $95,413 | $8,149 | $85,913 | $4,134 | $38,315 | $24,473 | 4.33% |

| 2023 | $99,988 | $13,768 | $87,631 | $4,029 | $40,957 | $27,221 | 4.03% |

| 2024 | $90,308 | $14,458 | $84,774 | $4,071 | $43,061 | $29,596 | 4.51% |

| 2025 | $83,255 | $16,120 | $82,536 | $4,032 | $44,642 | $30,675 | 4.84% |

| 2026 | NA | NA | NA | NA | $46,500 | $772 | NA |

| Annualized Development | -4.31% | 6.55% | -2.15% | -2.55% | 7.09% | 11.89% | 1.84% |

(Supply: FactSet Analysis Terminal)

Administration is dedicated to its A-credit ranking and plans to take care of leverage under 3.5 debt/EBITDA, which ranking businesses contemplate secure for this business.

We ended the 12 months with internet leverage at 2.4 instances and returned a complete of $8.5 billion to shareholders, together with $4.5 billion in dividend funds and $4 billion in share repurchases.

For 2022 as I stated beforehand, we count on to proceed to take care of leverage at round present ranges, which I count on will assist continued sturdy capital returns.” – CFO, This fall convention name

CMCSA Bond Profile

- $25.4 billion in liquidity

- very effectively staggered bond maturities

- no bother refinancing these bonds

- the bond market is prepared to lend to CMCSA for 75 years at 4.4%

- the sensible cash on Wall Road may be very assured in CMCSA’s enterprise prospects

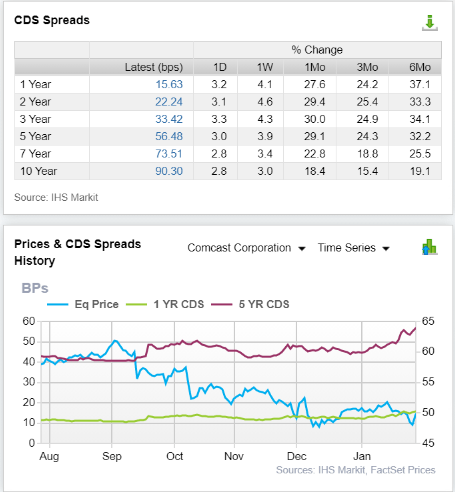

CMCSA Credit score Default SWAPs

FactSet Analysis Terminal

Credit score default swaps are insurance coverage in opposition to bond defaults, and thus symbolize a real-time bond market estimate of an organization’s quick and medium-term chapter threat.

- 10-year chapter threat 0.9%

- 5-year chapter threat 0.565%

Notice how the value has crashed in latest months. But the bond market’s real-time estimate of elementary threat has been comparatively regular, rising solely a modest quantity since administration introduced increased content material spending for Peacock throughout earnings.

So long as elementary threat just isn’t rising, a crashing inventory value just isn’t a priority for prudent long-term earnings buyers.

- analysts, ranking businesses, and the bond market all agree the thesis stays intact

If the businesses elementary threat had been to change into elevated sufficient for buyers to fret we would find out about it and ranking businesses would additionally start to downgrade CMCSA throughout their annual credit standing opinions.

Profitability: Wall Road’s Favourite High quality Proxy

CMCSA’s historic profitability is within the prime 20% of its friends.

CMCSA Trailing 12-Month Profitability Vs. Friends

| Metric | Business Percentile | Main International Media Corporations Extra Worthwhile Than CMCSA (Out Of 965) |

| Working Margin | 84.05 | 154 |

| Internet Margin | 80.73 | 186 |

| Return On Fairness | 80.20 | 191 |

| Return On Property | 69.63 | 293 |

| Return On Capital | 71.50 | 275 |

| Common | 77.22 | 220 |

(Supply: GuruFocus Premium)

Our definition of a large moat is sustaining profitability within the prime 25% of friends for many years.

CMCSA has maintained eightieth percentile profitability for 30+ years regardless of quite a few potential disruption dangers.

CMCSA Revenue Margin Consensus Forecast

| 12 months | DCF Margin | EBITDA Margin | EBIT (Working) Margin | Internet Margin | Return On Capital Growth |

Return On Capital Forecast |

| 2020 | 12.8% | 29.8% | 16.9% | 10.2% | 1.27 | |

| 2021 | 12.8% | 29.9% | 18.2% | 12.3% | TTM ROC | 45.76% |

| 2022 | 12.9% | 31.3% | 20.0% | 13.0% | Newest ROC | 47.10% |

| 2023 | 14.3% | 32.6% | 21.7% | 14.4% | 2026 ROC | 58.04% |

| 2024 | 16.0% | 33.0% | 22.7% | 14.9% | 2026 ROC | 59.74% |

| 2025 | 16.9% | 33.6% | 23.1% | 15.4% | Common | 58.89% |

| 2026 | 16.6% | 33.7% | 0.0% | 15.2% | Business Median | 13.53% |

| Annualized Development | 4.38% | 2.10% | 6.45% | 6.98% | CMCSA/Friends | 4.35 |

| Vs S&P | 4.53 |

(Supply: FactSet Analysis Terminal)

Comcast’s margins are anticipated to steadily enhance over time, regardless of increased progress spending for issues like Broadband enlargement and Peacock.

ROC has been regular for a decade (not counting the pandemic that shut parks).

ROC is up 100% within the final three many years.

Return on capital is pre-tax revenue/the cash it takes to run the enterprise (working capital).

That is Joel Greenblatt’s gold customary proxy for high quality and moatiness, and Comcast has a few of the finest ROC within the business.

CMCSA Dividend Development Consensus Forecast

| 12 months | Dividend Consensus | FCF/share Consensus | Payout Ratio | Retained (Publish-Dividend) Money Flows | Buyback Potential | Debt Reimbursement Potential |

| 2021 | $1.00 | $3.16 | 31.6% | $9,869 | 4.46% | 10.0% |

| 2022 | $1.08 | $3.56 | 30.3% | $11,331 | 5.12% | 11.5% |

| 2023 | $1.20 | $4.41 | 27.2% | $14,666 | 6.63% | 15.4% |

| 2024 | $1.28 | $4.81 | 26.6% | $16,129 | 7.29% | 16.1% |

| 2025 | $1.35 | $5.43 | 24.9% | $18,642 | 8.42% | 20.6% |

| 2026 | $1.40 | $6.08 | 23.0% | $21,383 | 9.66% | 25.7% |

| Whole 2021 Via 2026 | $3.28 | $11.13 | 29.5% | $35,866.65 | 16.20% | 36.50% |

| Annualized Price | 6.96% | 13.98% | -6.16% | 16.72% | 16.72% | 20.66% |

(Supply: FactSet Analysis Terminal)

- 70% FCF payout ratios are secure in accordance with ranking businesses for this business

- CMCSA’s is anticipated to fall to 23% by 2026

- $36 billion post-dividend retained money stream

- sufficient to repay 37% of debt or purchase again 16% of shares.

- As much as nearly 10% of shares in 2026 at as we speak’s valuation

- $60.6 billion in buybacks anticipated via 2026

- 27% of shares at present valuations

- 6% per 12 months

Comcast has already purchased again $4 billion in inventory in 2021 and the board simply elevated the authorization by one other $10 billion.

As we introduced this morning, we’re elevating the dividend by $0.08 to $1.08 per share, our 14th consecutive annual enhance, and our Board of Administrators has elevated our share repurchase authorization to $10 billion. This capital allocation coverage will enable us to take care of the stability we have talked about, make investments organically within the companies, preserve a robust stability sheet, and return capital to shareholders.” – CFO, This fall convention name

The underside line is that Comcast owns a few of the finest media and telecom property in America, which generate secure, recurring earnings. That is what makes it an excellent long-term dividend progress blue-chip.

Cause 2: A Sturdy Development Runway

You may not count on a telecom to be a fast-growing firm and in the event you solely have a look at the highest line, you would be proper.

CMCSA Medium-Time period Development Consensus Forecast

| 12 months | Gross sales | Free Money Movement | EBITDA | EBIT (Working Revenue) | Internet Revenue |

| 2020 | $103,564 | $13,280 | $30,826 | $17,493 | $10,534 |

| 2021 | $115,698 | $14,830 | $34,605 | $21,055 | $14,199 |

| 2022 | $122,301 | $15,724 | $38,315 | $24,473 | $15,958 |

| 2023 | $125,608 | $17,926 | $40,957 | $27,221 | $18,115 |

| 2024 | $130,363 | $20,805 | $43,061 | $29,596 | $19,418 |

| 2025 | $132,892 | $22,467 | $44,642 | $30,675 | $20,419 |

| 2026 | $137,878 | $22,870 | $46,500 | NA | $21,024 |

| Annualized Development | 4.89% | 9.48% | 7.09% | 11.89% | 12.21% |

(Supply: FactSet Analysis Terminal)

Analysts count on Comcast to develop at a modest 5% so far as gross sales go. However its backside line is anticipated to develop lots quicker, double-digits in reality.

That is attributable to a few of the finest economies of scale within the business, which administration plans to maintain enhancing via disciplined cost-cutting.

(Supply: FactSet Analysis Terminal)

It is not subscriber progress that analysts count on to drive CMCSA’s prime and bottom-line progress however regular and fast will increase in common income per consumer, or ARPU.

- 12.4% CAGR progress in ARPU from 2020 via 2025

That is why CMCSA is planning to extend spending for Peacock to $5 billion per 12 months, to higher assist it monetize its current asset base and amortize its prices throughout a bigger and extra diversified income stream.

That is how one can drive regular margin progress and 15% long-term earnings progress (mixed with wholesome buybacks) even with a sluggish however regular decline in cable subscriptions.

CMCSA Lengthy-Time period Development Outlook

- 14.7% to 18.1% CAGR progress consensus vary

- 15.1% CAGR median progress forecast

- smoothing for outliers historic analyst margins of error are 5% to the draw back and 15% to the upside

- 13% to 21% CAGR historic margin-of-error adjusted progress consensus vary

CMCSA is anticipated to develop at related charges because the final 13 years, a interval that has seen very regular cord-cutting that analysts totally count on to proceed.

Bear in mind the expansion thesis for Comcast is not that cable subscribers will develop.

It is that Comcast will have the ability to higher monetize its total buyer base, and continue to grow regardless of secular headwinds in considered one of its core companies.

- very similar to tobacco firms continue to grow regardless of falling cigarette volumes

Cause 3: A Great Firm At Anti-Bubble Valuations

Within the trendy cord-cutting period, CMCSA’s historic truthful worth is between 17.5 and 18.5X earnings.

| Metric | Historic Truthful Worth Multiples (13-Years) | 2020 | 2021 | 2022 | 2023 |

12-Month Ahead Truthful Worth |

| 13-12 months Median Yield | 1.68% | $54.76 | $59.52 | $59.52 | $64.29 | |

| Earnings | 18.12 | $47.29 | $57.71 | $67.41 | $76.47 | |

| Common | $50.75 | $58.60 | $63.22 | $69.85 | $63.73 | |

| Present Value | $49.92 | |||||

|

Low cost To Truthful Worth |

1.64% | 14.82% | 21.04% | 28.53% | 21.67% | |

|

Upside To Truthful Worth (NOT Together with Dividends) |

1.67% | 17.39% | 26.65% | 39.92% | 27.67% | |

| 2022 EPS | 2023 EPS | 2021 Weighted EPS | 2022 Weighted EPS | 12-Month Ahead EPS | 12-Month Common Truthful Worth Ahead PE |

Present Ahead PE |

| $3.72 | $4.26 | $3.43 | $0.33 | $3.76 | 16.9 | 13.3 |

(Supply: Dividend Kings Analysis Terminal, FactSet)

Comcast is price about 17X earnings and as we speak trades at 13.3.

Not solely is {that a} very enticing valuation for a Tremendous SWAN high quality firm rising at 15%, nevertheless it truly understates simply how attractively valued CMCSA actually is.

CMCSA is buying and selling at 8.5X EV/EBITDA proper now.

- enterprise worth = market cap + internet debt

- EV/EBITDA is “the acquirer’s a number of”

- Joel Greenblatt and personal fairness’s favourite valuation metric

How low is 8.5X EV/EBITDA? In accordance with the Graham/Dodd truthful worth components it doubtlessly means CMCSA is priced for zero progress.

15% is definitely what is anticipated.

Within the first 10 seasons of Shark Tank, the typical EV/EBITDA a number of was 7.0.

Pre-pandemic the typical non-public fairness deal was closing at 12.3 EV/EBITDA and after the pandemic that rose to over 13.

Immediately you should buy CMCSA as an anti-bubble inventory, at the very least taking a look at its acquirer’s a number of.

- a hyper-growth Tremendous SWAN buying and selling at non-public fairness valuations

|

Analyst Median 12-Month Value Goal |

Morningstar Truthful Worth Estimate |

| $62.47 (14.7 PE) | $60.00 (16 PE) |

|

Low cost To Value Goal (Not A Truthful Worth Estimate) |

Low cost To Truthful Worth |

| 20.25% | 16.97% |

|

Upside To Value Goal (Not Together with Dividend) |

Upside To Truthful Worth (Not Together with Dividend) |

| 25.39% | 20.43% |

|

12-Month Median Whole Return Value (Together with Dividend) |

Truthful Worth + 12-Month Dividend |

| $63.55 | $61.08 |

|

Low cost To Whole Value Goal (Not A Truthful Worth Estimate) |

Low cost To Truthful Worth + 12-Month Dividend |

| 21.61% | 18.43% |

|

Upside To Value Goal ( Together with Dividend) |

Upside To Truthful Worth + Dividend |

| 27.56% | 22.60% |

(Supply: Dividend Kings Analysis Terminal, FactSet)

Analysts count on 28% complete returns from CMCSA in simply the subsequent 12 months, and 20% of that might be justified by its fundamentals and valuation.

For anybody snug with CMCSA’s threat profile, it is a doubtlessly sturdy purchase at a 15% historic low cost to truthful worth, and here is why.

Whole Return Potential: Purchase Comcast Immediately And You may Thank Me Tomorrow

For context, here is the return potential of the 18% overvalued S&P 500.

| 12 months | EPS Consensus | YOY Development | Ahead PE | Blended PE | Overvaluation (Ahead PE) |

Overvaluation (Blended PE) |

| 2021 | $203.82 | 48.69% | 23.5 | 23.1 | 37% | 31% |

| 2022 | $222.51 | 9.17% | 19.9 | 21.7 | 16% | 23% |

| 2023 | $245.41 | 10.29% | 18.1 | 19.0 | 5% | 8% |

| 2024 | $274.74 | 11.95% | 16.1 | 17.1 | -6% | -3% |

| 12-Month ahead EPS | 12-Month Ahead PE | Historic Overvaluation | PEG | 25-12 months Common PEG | S&P 500 Dividend Yield |

25-12 months Common Dividend Yield |

| $223.57 | 19.823 | 17.78% | 2.33 | 3.62 | 1.45% | 2.01% |

(Supply: DK S&P 500 Valuation And Whole Return Software) up to date weekly

Shares have already priced in nearly the entire 100% EPS progress from 2020 via 2024 and is buying and selling at 21.1X ahead earnings.

- 16.8 is the 25-year common

Analysts count on the S&P 500 to ship about -8% complete returns over the subsequent two years.

| 12 months | Upside Potential By Finish of That 12 months | Consensus CAGR Return Potential By Finish of That 12 months | Chance-Weighted Return (Annualized) |

Inflation And Danger-Adjusted Anticipated Returns |

| 2027 | 35.17% | 6.21% | 4.66% | 1.93% |

(Supply: DK S&P 500 Valuation And Whole Return Software) up to date weekly

Adjusted for inflation, the risk-expected returns of the S&P 500 are about 2% for the subsequent 5 years.

- S&P’s historic inflation-adjusted returns are 6% to 7% CAGR

However here is what buyers shopping for CMCSA as we speak can fairly count on.

- 5-year consensus return potential vary: 16% to 22% CAGR

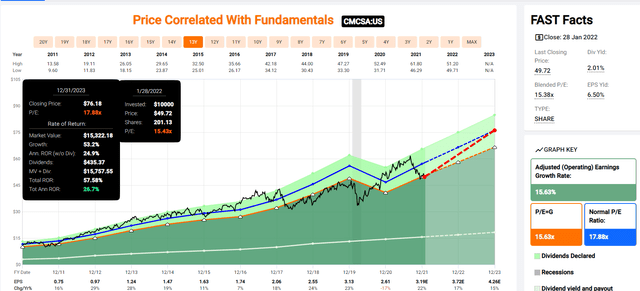

CMCSA 2023 Consensus Whole Return Potential

FAST Graphs, FactSet Analysis

In accordance with analysts, CMCSA may not simply ship Buffett-like 24% returns in 2022 however for the subsequent two years.

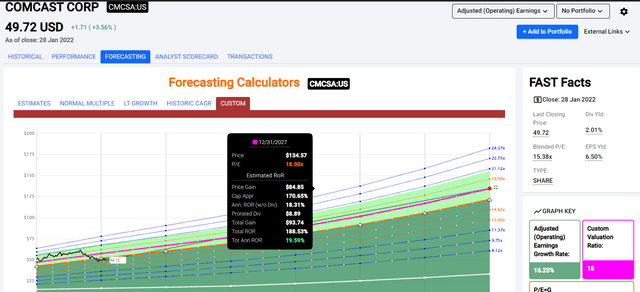

CMCSA 2027 Consensus Whole Return Potential

FAST Graphs, FactSet Analysis

- if CMCSA grows as anticipated and returns to historic mid-range truthful worth

- then 189% complete returns or 20% CAGR

- about 5x greater than the S&P 500 consensus

CMCSA Funding Determination Rating

Dividend Kings

Dividend Kings Automated Funding Determination Software

For anybody snug with its threat profile, CMCSA is without doubt one of the most affordable and prudent hyper-growth blue-chips you should buy in as we speak’s quickly reinflating and nonetheless overvalued market.

Danger Profile: Why Comcast Is not Proper For Everybody

There are not any risk-free firms and no firm is true for everybody. It’s important to be snug with the basic threat profile.

CMCSA’s Danger Profile Consists of

- political/regulator threat (globally)

- disruption threat (T-Cellular if now rolling out $50 per thirty days 5-G dwelling web)

- altering client tastes (problem reaching earlier economies of scale with the rise of streaming for instance)

- M&A execution threat (together with regulatory threat on this as effectively)

- expertise retention threat (tightest job market in over 50 years)

- foreign money threat (grows over time as they develop internationally)

- cybersecurity threat: hackers and ransomware

Comcast is anticipated to begin to see shrinking subscribers inside just a few years and solely very sturdy progress in common income per consumer is anticipated to end in sturdy bottom-line progress.

- altering client tastes may end in ARPU progress not coming in as anticipated

How can we quantify, monitor, and monitor such a posh threat profile? By doing what massive establishments do.

Materials Monetary ESG Danger Evaluation: How Massive Establishments Measure Whole Danger

Here’s a particular report that outlines an important features of understanding long-term ESG monetary dangers in your investments.

- ESG is NOT “political or private ethics primarily based investing”

- it is complete long-term threat administration evaluation

ESG is simply regular threat by one other identify.” Simon MacMahon, head of ESG and company governance analysis, Sustainalytics” – Morningstar

ESG components are considered, alongside all different credit score components, once we contemplate they’re related to and have or might have a cloth affect on creditworthiness.” – S&P

ESG is a measure of threat, not of ethics, political correctness, or private opinion.

S&P, Fitch, Moody’s, DBRS (Canadian ranking company), AM Finest (insurance coverage ranking company), R&I Credit score Ranking (Japanese ranking company), and the Japan Credit score Ranking Company have been utilizing ESG fashions of their credit score scores for many years.

- credit score and threat administration scores make up 38% of the DK security and high quality mannequin

- dividend/stability sheet/threat scores make up 79% of the DK security and high quality mannequin

Dividend Aristocrats: 67th Business Percentile On Danger Administration (Above-Common, Medium Danger)

CMCSA Lengthy-Time period Danger Administration Consensus

| Ranking Company | Business Percentile |

Ranking Company Classification |

| MSCI 37 Metric Mannequin | 57.0% |

BB, below-average |

| Morningstar/Sustainalytics 20 Metric Mannequin | 65.9% |

24.7/100 Medium-Danger |

| Reuters’/Refinitiv 500+ Metric Mannequin | 91.4% | Good |

| S&P 1,000+ Metric Mannequin | 40.0% |

Under-Common (Steady Development) |

| Simply Capital 19 Metric Mannequin | 92.31% | Wonderful |

| Consensus | 69.3% | Above-Common |

| FactSet Qualitative Evaluation | Common | Optimistic Development |

(Sources: MSCI, Morningstar, Reuters’, S&P, Simply Capital, FactSet Analysis)

CMCSA’s Lengthy-Time period Danger Administration Is The 198th Finest In The Grasp Record (sixtieth Percentile)

CMCSA’s risk-management consensus is within the prime 40% of the world’s highest high quality firms and just like that of such different firms as

- Pembina Pipeline Corp (PBA)

- Illinois Software Works (ITW) – dividend king

- Cardinal Well being (CAH) – dividend aristocrat

- Royal Financial institution of Canada (RY)

- QUALCOMM (QCOM)

- Consolidated Edison (ED) – dividend aristocrat

- Verizon (VZ)

The underside line is that every one firms have dangers, and CMCSA is above-average at managing theirs.

How We Monitor CMCSA’s Danger Profile

- 38 analysts

- 3 credit standing businesses

- 8 complete threat ranking businesses

- 46 specialists who collectively know this enterprise higher than anybody apart from administration

- and the bond market, the “sensible cash” on Wall Road

When the info change, I alter my thoughts. What do you do sir?” – John Maynard Keynes

There are not any sacred cows at iREIT or Dividend Kings. Wherever the basics lead we at all times observe. That is the essence of disciplined monetary science, the maths retiring wealthy and staying wealthy in retirement.

Backside Line: Purchase Comcast Now Earlier than Everybody Else Does

I can not promise you that the worry we noticed within the markets in January will not return in just a few weeks and even tomorrow.

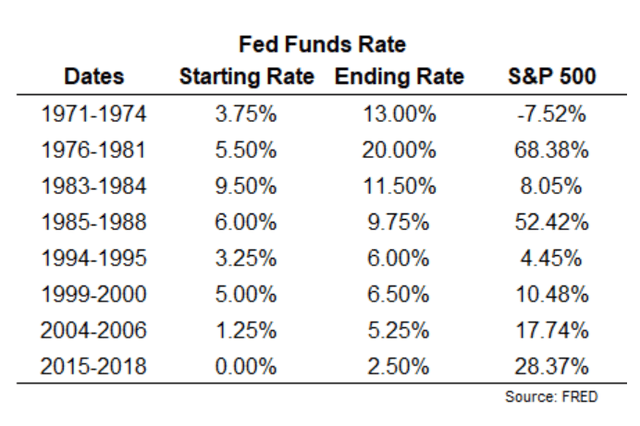

In accordance with a latest survey by Financial institution of America of 400 mutual fund managers, zero had been anticipating 4+ charge hikes in 2022.

Day by day Shot, Bloomberg

In distinction, the bond market is now all however sure we’ll get 5 charge hikes this 12 months and Financial institution of America and several other Fed presidents assume it could possibly be as a lot as seven.

What does this imply within the short-term? That the inventory market and bond market considerably disagree about rates of interest this 12 months.

Traditionally, when the inventory and bond market disagree, the “sensible cash”, i.e. the bond market, is confirmed proper.

That would imply that we’d see this correction reverse, retest, and even break to new lows.

Or we may see file highs finish the correction, and if the Fed comes via with 5 charge hikes (or extra) we may see one other, presumably deeper correction of 15% to twenty%.

Ben Carlson

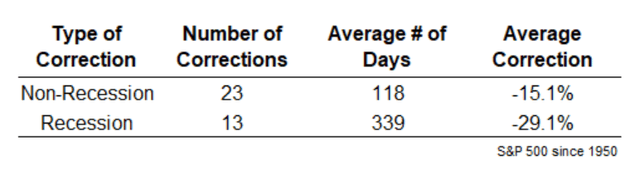

The typical non-recessionary correction since 1950 has seen shares fall for about 4 months, by 15%.

Ben Carlson

The typical non-recessionary bear market has tended to be gentle, a few 19% to twenty% decline.

Together with recessions, the typical bear market sees shares fall for 13 months, a mean of 33%. It then takes about two years to get again to file highs.

- the typical bear market lasts three years from peak to a brand new file excessive

If there may be any 12 months during which elevated valuations and a tightening Fed may set off a 15% to twenty% correction, it is 2022.

The principle objective of the inventory market is to make fools of as many males as potential.” – Barnard Baruch

In fact, historic averages solely give us an thought of what MIGHT occur, they do not predict what is going to occur.

Common Inventory Acquire Throughout Fed Tightening Cycle Is 23% (Ben Carlson )

Finance is a science, however a statistical one, and there are not any ensures.

However what I can inform you is that no long-term investor, who averted changing into a pressured vendor for emotional or monetary causes, has ever regretted shopping for Comcast at 13.3X ahead earnings of 8.5X EV/EBITDA.

And primarily based on a cautious and thorough examination of the most effective obtainable information we have now as we speak, I can say with 80% confidence that as we speak is unlikely to be the primary time.

For this reason I purchased extra Comcast for my retirement portfolio not too long ago and also you would possibly wish to do the identical.

Luck is what occurs when preparation meets alternative.” – Roman Thinker Seneca the Youthful

As a result of in a market that was nonetheless overvalued when it may need bottomed and is now doubtlessly roaring again to file highs, nice blue-chip bargains are nonetheless plentiful if the place to look.

When you’re looking for world-class high quality, hyper-growth, and enticing valuation, contemplate Comcast.

In case you are uninterested in fretting over each market downturn, contemplate Comcast’s very secure and steadily rising dividends.

When you’re uninterested in praying for luck on Wall Road, then it is time to cease playing and begin investing in blue-chips like Comcast.

After fastidiously inspecting the information, I’ve only one conclusion on the subject of this hyper-growth Tremendous SWAN.

Purchase Comcast now earlier than everybody else does.

{kind=link}