B4LLS

There are two methods to be fooled. One is to imagine what is not true; the opposite is to refuse to imagine what’s true.”― Soren Kierkegaard

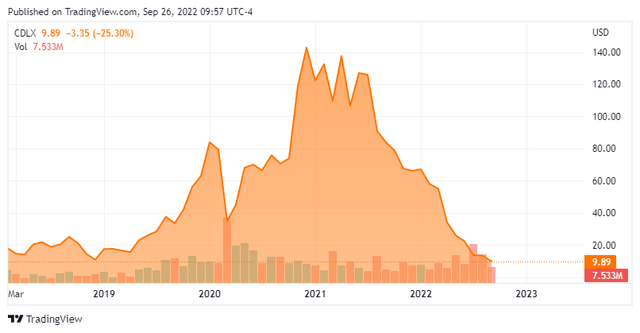

Right now, we shine the highlight on Cardlytics, Inc. (NASDAQ:CDLX) for the primary time. As will be seen beneath, the inventory has been crushed on a poorly timed acquisition in addition to a more difficult setting for each digital promoting spend and client spending. The corporate not too long ago introduced in a new CEO, lowered steering, and carried out some cost-cutting measures. Will or not it’s sufficient to cease the bleeding? An evaluation follows beneath.

In search of Alpha

Firm Overview:

Cardlytics, Inc. is headquartered in Atlanta, GA. The corporate operates an promoting platform in the US and the UK. The agency provides Cardlytics platform to its shoppers. It is a proprietary native financial institution promoting channel that permits entrepreneurs to succeed in prospects by their community of economic establishment companions by numerous digital channels (EX, cellular apps, electronic mail, and so on.). Cardlytics additionally supplies its Bridg platform. It is a buyer knowledge platform which makes use of point-of-sale knowledge and permits entrepreneurs to carry out analytics and focused loyalty advertising and marketing, in addition to measure the impression of their advertising and marketing. The inventory presently trades round ten bucks a share and sports activities an approximate $320 million market capitalization.

August Firm Presentation

Cardlytics works with banks and monetary establishments to run their banking rewards packages that promote buyer loyalty and deepen banking relationships. For which, Cardlytics has a safe view into the place and when shoppers are spending their cash. In flip, these insights will help entrepreneurs establish, attain, and affect doubtless patrons at scale.

Second Quarter Outcomes:

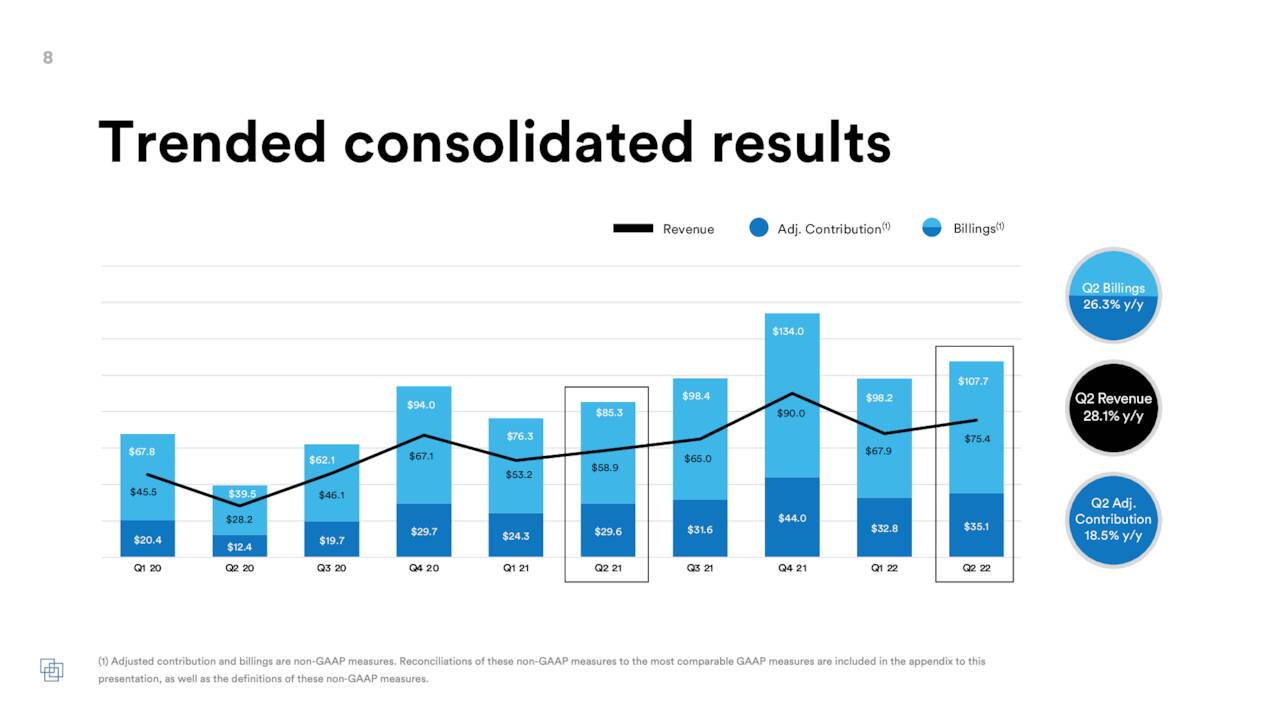

On August 2nd, Cardlytics posted its second quarter numbers. The corporate misplaced $3.75 a share on a GAAP foundation, lacking expectations by over $2.80 a share. Revenues rose 28% from the identical interval a 12 months to $75.4 million, simply barely lacking the consensus. The corporate took an $83 million goodwill impairment value in relation to the acquisition of Bridg (mentioned later on this part) which accounts for almost all of the headline backside line ‘miss’.

August Firm Presentation

Administration offered another key metrics for the second quarter:

- Billings, a non-GAAP metric, was $107.7 million, a rise of 26% year-over-year, in comparison with $85.3 million within the second quarter of 2021.

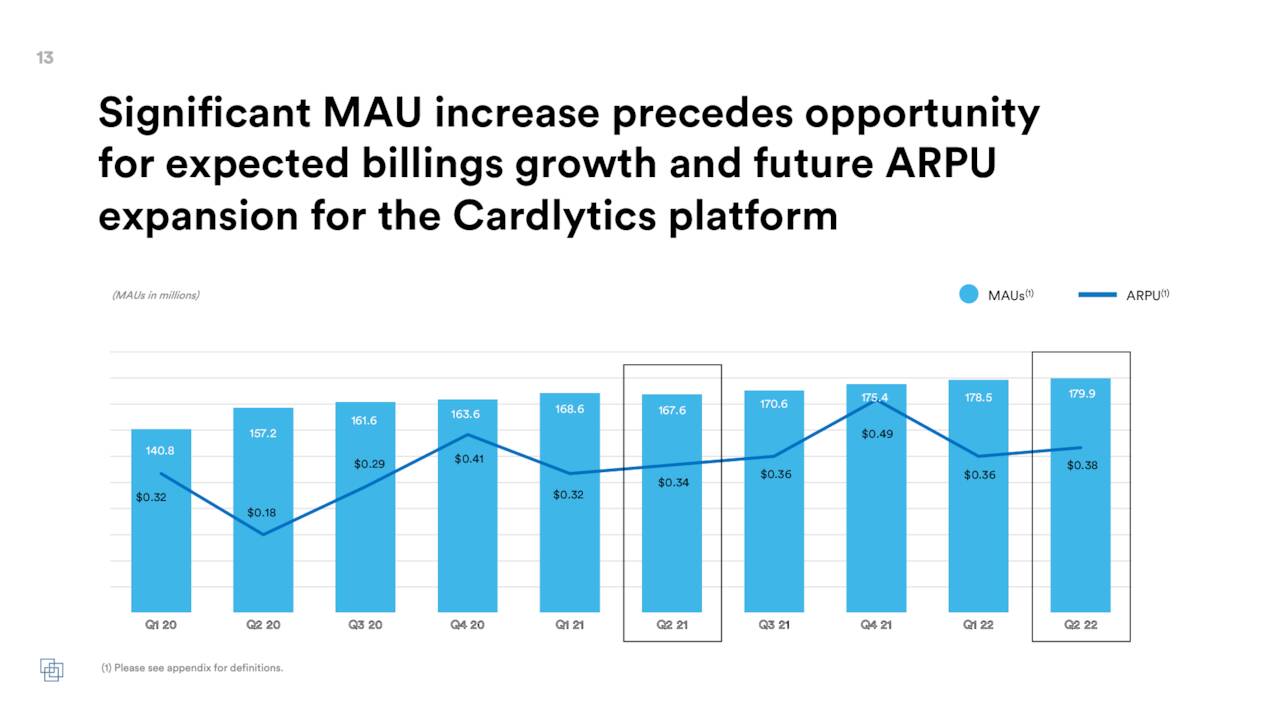

- Cardlytics MAUs (Month-to-month Lively Customers) had been 179.9 million, a rise of seven%, in comparison with 167.6 million within the second quarter of 2021.

- Cardlytics ARPU (Common Income Per Person) was $0.38, a rise of 12%, in comparison with $0.34 within the second quarter of 2021.

August Firm Presentation

Again in April of final 12 months, Cardlytics bought Bridg, a buyer knowledge platform for $350 million in money. Bridg has a cloud-based platform that retailers and CPG entrepreneurs use for a variety of purposes, together with analyzing buyer habits, advertising and marketing on digital platforms, and measuring the effectiveness of their enterprise methods, whereas following client privateness finest practices. Bridg ARR was $21.8 million within the second quarter, which was up 35% sequentially from the primary quarter of this 12 months. As a part of this acquisition, Cardlytics additionally agreed to make two potential earnout funds in money and inventory on the primary and second anniversary of the closing. This will probably be primarily based on Bridg’s U.S. annualized income run fee. Cardlytics expects these funds may equal roughly $100 million to $300 million in whole.

Administration lowered its steering and now believes revenues will develop simply 10% to fifteen% within the second half of 2022 on a year-over-year foundation.

Analyst Commentary & Stability Sheet:

Since Q2 outcomes got here out, the analyst group has been fairly detrimental on Cardlytics’ prospects. JPMorgan ($17 value goal), Craig-Hallum ($15 value goal), and Wells Fargo ($13 value goal) have all maintained or downgraded to Maintain rankings. Needham ($19 value goal) reissued its Purchase score and seems to be the lone optimist on CDLX in the meanwhile.

Simply over 20% of the excellent float within the shares are presently held brief. A number of insiders step up their purchases in each Could and August, shopping for roughly $600,000 value of shares in mixture throughout these two months. The corporate ended the second quarter with simply over $155 million of money and marketable securities on its steadiness sheet in opposition to roughly $225 million of long-term debt. The corporate additionally has entry to a $60 million credit score facility if wanted.

Verdict:

The present analyst agency consensus has the corporate shedding simply over $1.50 a share in FY2022 as revenues rise some 18% to $317 million. In FY2023, the mission gross sales will rise 15% and losses will probably be lower to simply over $1.10 a share.

The corporate named its new CEO in July and he can have loads of challenges going ahead within the coming months and quarters. Digital promoting spend progress is falling and can proceed to take action because the nation heads into recession. Client spending can also be dropping. Administration acknowledged on its second quarter earnings name that common restaurant spending it screens was up 12% initially of the second quarter, however had fallen to simply 2% by the top of the quarter as however one instance of this client spending slowdown.

As well as, in hindsight, it seems the corporate clearly overpaid for the Bridg acquisition given its present income run fee and up to date goodwill write-down. Cardlytics additionally used $40 million of money within the second quarter to purchase again inventory on the common value of $28 a share. Hardly, one of the best use for its money looking back. That inventory buyback authorization has now been used up it needs to be famous.

August Firm Presentation

The corporate is implementing a plan to chop $15 million in annual prices out of operations and hopes to realize constructive free money circulation by the third quarter of 2023. Given the declining financial system, it’s laborious to say whether or not these measures will probably be sufficient to stem losses within the coming quarters and years. Shorts appear to imagine the inventory has additional to fall primarily based on the excessive brief proportion within the shares. Subsequently, till extra progress is seen on a number of fronts, CDLX appears to be an keep away from proper now for buyers.

The one who writes for fools is all the time certain of a giant viewers.”― Arthur Schopenhauer

{kind=link}