JHVEPhoto

I’ve beforehand written a couple of small, impartial oil and gasoline firm, SandRidge Vitality, (NYSE: SD) discussing how I imagine it has a low valuation, a wonderful stability sheet, robust money flows and up to date shareholder distributions. I’ll keep within the similar business this time with an organization that has some related traits, however with an organization that’s on the opposite finish of the spectrum by way of measurement and scale.

For my part, Chevron (NYSE:CVX) is the very best of the massive oil majors. It has been on fairly a powerful run these days as oil costs have elevated, so it could be higher to attend for a pullback to purchase, however this can be a strong performer with a wonderful administration group that has put the shareholder first for many years with a rising dividend and periodic share repurchases. They’ve additionally considerably scaled again their capital expenditures within the final decade, preferring so as to add manufacturing within the US shale house relatively than decide to the costly deepwater initiatives of a long time previous. That stated, they’ve introduced some giant acquisitions just lately, with the monster $53 billion all inventory Hess deal nonetheless pending completion. This deal is a shot throughout the bow at the concept oil is peaking anytime quickly.

A Dividend Aristocrat

If you happen to personal Chevron, one of many foremost causes that you just personal it’s for the dividend, which is yielding greater than 4% at present and has been rising for 37 straight years. Administration has been steadfast that defending and rising the dividend is their first precedence; they are saying it nearly each convention name and so they proved it by sustaining the dividend by COVID, regardless of the shock to the oil markets. Chevron additionally boasts sturdy free money flows, a powerful stability sheet that has seen its debt decreased by half since early 2021, and a historical past of share repurchases with extra money flows that aren’t wanted for the dividend or its capital program.

Clearly, as an oil and gasoline main, the monetary outcomes and subsequently the inventory returns are closely influenced by the value of oil. That can also be the largest danger. If oil costs lower for some cause fully uncontrolled of the Firm – for instance if Saudi Arabia fully floods the market with low cost oil – Chevron’s inventory will decline and decline laborious, like all oil and gasoline firm. I don’t have the opinion that this can be a possible state of affairs, however something can occur as we’ve discovered just lately with COVID, so it does need to be a consideration while you personal the inventory. Chevron, nevertheless, has the flexibility to face up to a significant shock to grease costs on account of its measurement, borrowing capability, and long-term outlook. Actually, they’ve confirmed in recent times {that a} shock to costs stands out as the time to purchase.

Tail dangers apart, Chevron gives a really secure method to achieve publicity to grease and gasoline, which is usually a hedge to different industries that do poorly when oil costs rise. The importance and security of the dividend provide draw back safety for the inventory worth as effectively, and are possible solely to be put in danger if there’s a sustained downturn of oil costs.

Classes from the latest previous

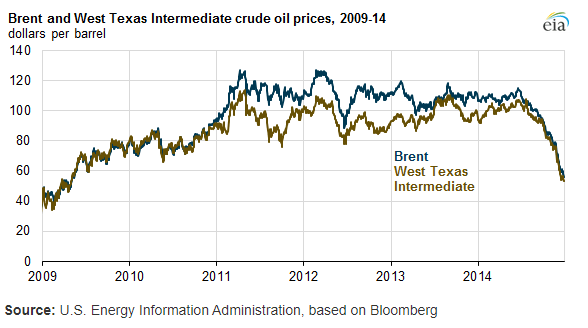

For my part, Chevron modified as an organization within the 2015/2016 timeframe and it was the “luck” of poor oil markets that helped make this doable. Simply previous to this time, oil costs had spent the previous 3-4 years hovering across the $100 mark. The tip of 2014 noticed fairly a unique pricing surroundings and this pressured Chevron’s hand, requiring them to shortly cut back their expenditures, which had been ballooning as a result of challenges of deepwater drilling, buoyed by excessive oil costs.

Brent and WTI crude oil costs, 2009-2014 (US Vitality Info Administration)

I used to be a shareholder on the time and considerably numb to the eye-popping capital plans that Chevron was presenting every December for the next yr. I simply figured that was the enterprise that they had been in, however on reflection I feel this was a really harmful sport that they had been taking part in.

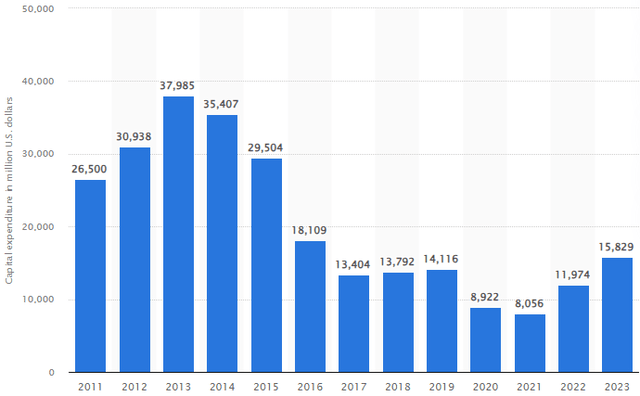

Check out Chevron’s capital expenditures previously 10 years:

Chevron capital expenditures (Macrotrends.internet)

With oil costs declining quickly, the capital plan introduced in December 2015 for was 24% beneath what they anticipated to spend in 2015, and as seen within the capital expenditure spending chart above, they haven’t come near these quantities, even with a big restoration in oil costs. Please observe that the capital expenditures and capital plan are totally different on account of affiliate capital plans and estimates vs precise price.

A couple of years later, this scaled again spending was essential to the corporate having the ability to face up to oil costs beneath $25 and proceed to pay its dividend throughout COVID. On the finish of 2020, they had been in a position to cut back their spending once more in response to decrease oil costs, and preserve it that degree for the upcoming years. Whereas comparatively momentary, have a look at how a lot oil dipped on the finish of 2020. Whereas that seems to be a blip on the chart, it’s vital to notice that the hole down from extra “regular” pricing was a couple of yr.

10 yr Brent Crude Oil chart (Tradingeconomics.com)

When investing in a commodity enterprise the place you may’t management the pricing, it’s vital to have the ability to face up to all environments. How would Chevron have fared in 2020 in the event that they had been spending $35 billion a yr on capital? That’s unimaginable to know, however price contemplating as an investor.

Decrease CapEx = Larger Free Money Move

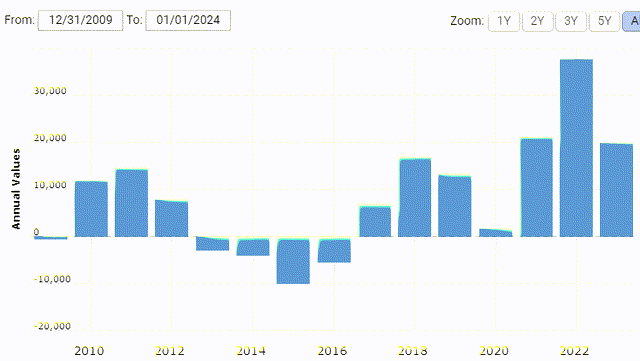

Clearly, the purpose of capital spending is to generate money flows sooner or later, however the easy truth is the much less you spend now, the extra free money move you generate at the moment. Taking an extended historical past of free money flows for Chevron, it’s clear the excessive spending days previously actually put a crimp on their money flows even in instances of robust oil costs.

Chevron annual free money move (Macrotrends.internet)

With 2023 free money flows at slightly below $20b, Chevron is buying and selling at 15x money flows, which is an inexpensive valuation for an organization with a 4%+ yield. As I’ve said above, I might in all probability let costs are available a bit earlier than beginning a brand new place, however I really feel very snug holding on to my present shares at these ranges and reinvesting my dividends.

Draw back Safety

Cloning Charlie Munger’s type, I’ll typically look to invert and perceive how a lot I can lose, relatively than how a lot I could make in a inventory. That’s not all the time doable for each inventory, however I feel that Chevron gives a chance to take action due to the dividend yield. The dividend supplies substantial draw back inventory worth safety due to the significance that administration has positioned on defending the dividend.

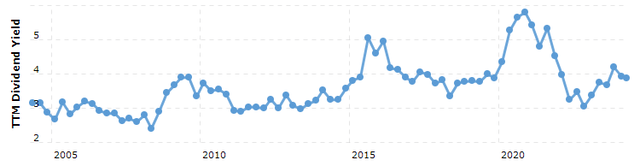

The beneath chart is the trailing twelve month dividend yield over the previous 20 years:

Chevron dividend yield historical past (Macrotrends.internet)

Even in dire instances, Chevron solely ended up yielding 6%. Immediately, that might deliver the inventory right down to about $109, however that’s dire, as soon as in a lifetime pandemic instances. In a standard poor pricing surroundings, the draw back appears to be like extra like a dividend yield of 5%, or $130 primarily based on the present dividend. That looks as if a fairly affordable draw back viewpoint, particularly given how robust the oil market has been just lately. Add in the truth that we all know Chevron desires to repeatedly enhance the dividend, which is simply going to boost that draw back safety annually.

I wouldn’t make this argument with each firm, as we all know {that a} excessive yield could possibly be a sign that the dividend is in bother. However with a dividend aristocrat like Chevron, I’m snug taking this stance.

Dangers to Proudly owning Chevron

As I’ve already mentioned above, Chevron doesn’t management pricing which is the obvious danger for an oil and gasoline firm, however I imagine that their robust stability sheet and skilled administration group have given them enough cushion to face up to durations of low costs.

An extended-term danger is the way forward for oil and whether or not we’re nearing a peak in oil consumption within the close to future. Chevron invests for many years, not quarters, and with this long-time horizon, the existential danger of oil needs to be thought of. I’ll reduce proper to the chase and inform you that for my part, there isn’t any existential danger of oil operating out in my lifetime, it doesn’t matter what yr anybody desires to placed on it. 2052 gave the impression to be a well-liked estimate popularized by the MAHB of Stanford College, although any estimate this far sooner or later is much from sure. The IEA launched a report final fall stating that fossil gasoline demand would peak by the top of this decade! When requested about that expectation, CEO Mike Wirth said:

I don’t assume they’re remotely proper,” he informed the Monetary Instances. “You may construct situations, however we reside in the true world and need to allocate capital to satisfy actual world calls for.

I am not going to wade straight into this debate, however I do wish to have a look at potential medium-term impacts from this concern, such because the transition of the flamable engine to electrical.

Clearly, now we have the know-how to provide some actually nice EVs led by Tesla right here within the US. However can we make them inexpensive or as inexpensive as flamable engines? And might the businesses that produce them achieve this profitably, with out authorities incentives for both the corporate or the shopper? Take a look at the cautionary tales of bankrupt EV firms similar to Lordstown Motors and Proterra. As well as, each Fisker and Lucid Motors each seem like barely avoiding chapter, which limits their skill to spend money on their product. Furthermore, the charging infrastructure must be considerably expanded. This all will take time, for my part, and can gradual the transition from the flamable engine within the subsequent decade.

One can look to China the place firms like BYD have seemingly discovered the method to success on this market as a cautionary story right here, however I simply don’t assume Individuals are going to hurry to purchase the kind of inexpensive EVs that BYD produces relatively than the large SUVs and pickup vans that dominate the highway at the moment. I could possibly be incorrect, however I’m downplaying the impression of EVS within the brief to medium time period.

The Extra Sensible Danger to Monitor

As I talk about above, I might be way more nervous as a shareholder if Chevron’s capital spending plans begin to enhance considerably from right here. With the $7.6 billion acquisition of PDC and extra importantly the pending acquisition of Hess, capital spending will clearly have to extend considerably as Chevron will probably be a a lot bigger firm. That would deliver capital ranges again to the $25 – $30 billion vary in a number of years simply, which isn’t essentially a difficulty for me as a result of the money flows from this a lot bigger firm ought to be capable of assist that. Nonetheless, I will probably be taking a look at their capital spending plans very carefully within the subsequent couple of years to guarantee that we don’t return to extra aggressive spending ranges, in relation to the dimensions of the enterprise. Whereas new funding is definitely a boon for future manufacturing and can make the corporate way more worthwhile when costs are excessive, it could enhance the danger considerably within the case of a downturn. I do assume that administration, which is the very best within the enterprise, has heeded the teachings of the final ten years and can be sure that any enhance in spending is finished judiciously.

Q1 Outcomes Anticipated Subsequent Week

With Chevron’s Q1 outcomes anticipated subsequent Friday, April twenty sixth, I am not anticipating any vital modifications to my thesis, however I might count on a fairly good quarter with robust oil costs, particularly within the second half of the quarter. I feel the extra vital developments to watch could be an replace on the Hess acquisition, in addition to the impression of the acquisition of PDC, as this would be the second full quarter with its outcomes included. This fall 2023 outcomes had been impacted by roughly $4 billion of one-time expenses associated to the write-down of property, primarily in California. It is going to be attention-grabbing to see what a full quarter appears to be like like with PDC’s outcomes included and with none giant impairments.

Conclusion

Whereas I stay cognizant of the dangers, Chevron is as secure as an oil and gasoline firm might be. Its dividend gives a powerful yield, and its stability sheet gives it flexibility to speculate and in addition face up to volatility in oil costs. Administration has been by many up and down cycles over the previous a number of years and has emerged battle examined and unwavering in its need to guard the dividend. For anybody seeking to spend money on the oil and gasoline house, Chevron is a superb firm to contemplate.

{kind=link}