(Bloomberg) — China’s central financial institution boosted its gross injection of short-term money into the monetary system after concern over a debt disaster at China Evergrande Group roiled international markets.

Most Learn from Bloomberg

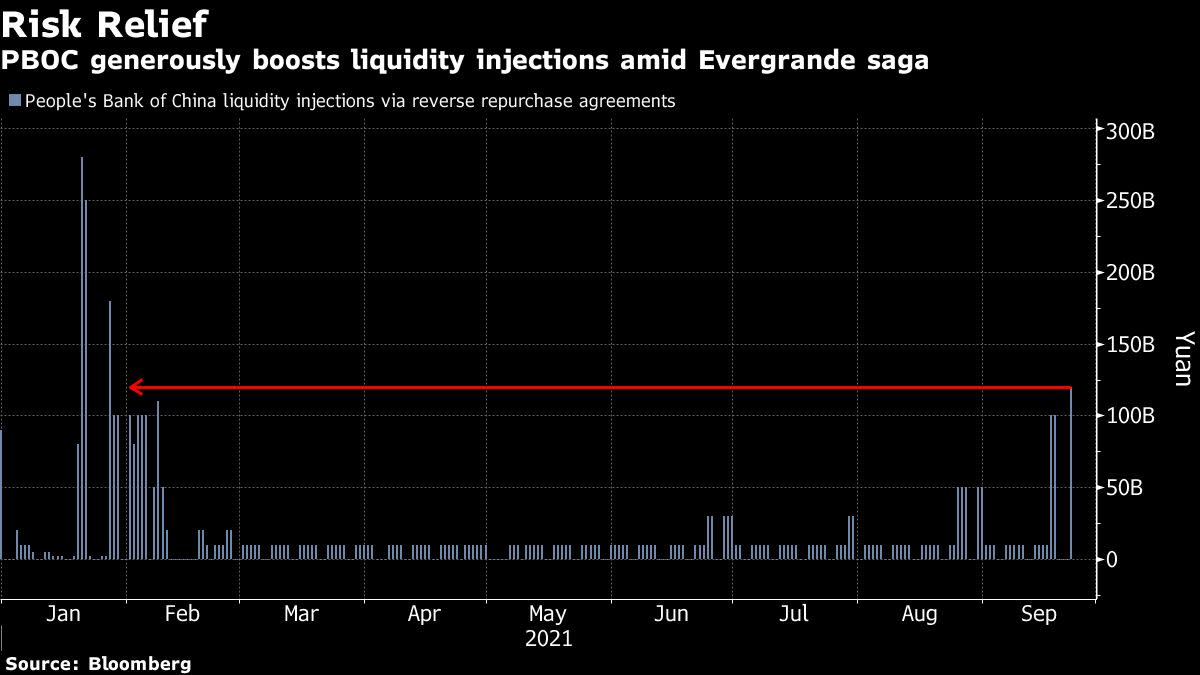

The Individuals’s Financial institution of China pumped 120 billion yuan ($18.6 billion) into the banking system by means of reverse repurchase agreements, leading to a web injection of 90 billion yuan. That matches the quantity seen on Friday, and was just under that of Saturday. Sentiment was additionally boosted after Evergrande’s onshore property unit mentioned it plans to repay curiosity due Thursday on its native bonds.

“The PBOC’s web injection might be geared toward soothing nerves because the market worries about Evergrande,” mentioned Eugene Leow, a senior charges strategist at DBS Financial institution Ltd. in Singapore. “Whereas the goal could also be to instill self-discipline, there may be additionally a necessity to forestall contagion into the true economic system or to different sectors.”

The necessity to calm market jitters is urgent amid losses in China-related equities worldwide over latest days amid concern over Evergrande’s debt woes. The benchmark CSI 300 Index fell as a lot as 1.9% Wednesday after the Cling Seng China Enterprises Index — a gauge of Chinese language shares traded in Hong Kong — slid essentially the most in two months on Monday. Losses got here at the same time as Wall Road analysts sought to reassure buyers that Evergrande received’t result in a Lehman second.

China’s money operations have been geared toward putting a stability between spurring development damage by contemporary virus outbreaks and tighter laws, whereas stopping asset bubbles. Authorities are likely to loosen their grip on liquidity towards quarter-end because of elevated demand for money from banks for regulatory checks. Lenders additionally have to hoard extra funds forward of the one-week vacation in the beginning of October.

There was “a reduction that there was an honest web liquidity injection, albeit a few of it will likely be required for quarter-end regulatory checks,” mentioned Mitul Kotecha, chief rising markets Asia & Europe strategist at TD Securities in Singapore. “It factors to a need to maintain steady liquidity within the days.”

Evergrande’s onshore property unit mentioned it negotiated a plan with bondholders to repay curiosity due Sept. 23 on native yuan bonds, in accordance with a vaguely worded alternate submitting on Wednesday. The corporate mentioned it should make the curiosity cost for its 5.8% 2025 safety. The quantity due for the coupon was 232 million yuan, in accordance with knowledge compiled by Bloomberg.

That got here after Evergrande missed curiosity funds due Monday to a minimum of two of its largest financial institution collectors, individuals acquainted with the matter mentioned, asking to not be recognized discussing non-public info.

Uncertainty over how monetary troubles at China’s largest property developer — with $300 billion of liabilities — can be resolved has swelled because the authorities have shunned offering any public assurances on a state-led decision. China’s slowing economic system has compounded investor angst. Nonetheless, many analysts — together with these at Citigroup Inc., Barclays Plc and UBS Group AG — say the Evergrande disaster isn’t more likely to turn out to be a Chinese language model of the Lehman collapse.

Merely boosting liquidity received’t be sufficient to unravel the Evergrande disaster by itself, mentioned Ding Shuang, chief economist for Larger China and North Asia at Normal Chartered Plc in Hong Kong.

“What the market hopes the federal government will do is to provide you with a plan that may assist the corporate restructure and refinance in a easy means,” he mentioned. “China’s backside line is that it received’t permit the Evergrande challenge to show right into a full-fledged monetary disaster or let it set off any systemic dangers.”

(Updates with further element in second paragraph, new quote in third.)

Most Learn from Bloomberg Businessweek

©2021 Bloomberg L.P.