EschCollection

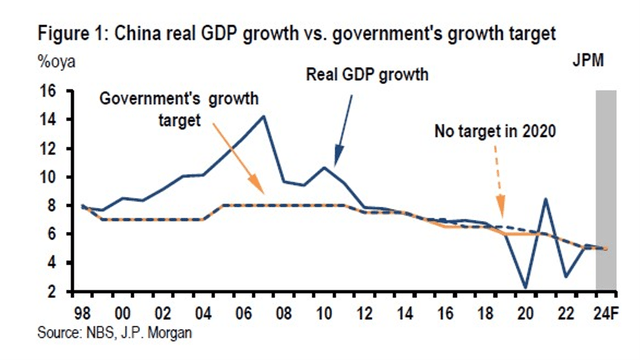

The IMF World Financial Outlook launched on Tuesday (April 16th) introduced a projection of China’s financial progress of 4.6% and 4.1% for, respectively, this 12 months and subsequent. In 2023, after the financial reopening with the tip of the “Covid zero” coverage, the speed was 5.2%, above the official goal of 5% (Determine 1).

This 12 months, the official goal has been arrange at 5% once more. However the challenges approached right here, the macroeconomic efficiency within the first quarter of 2024 has been in sync with such goal (He et al, 2024).

JPMorgan

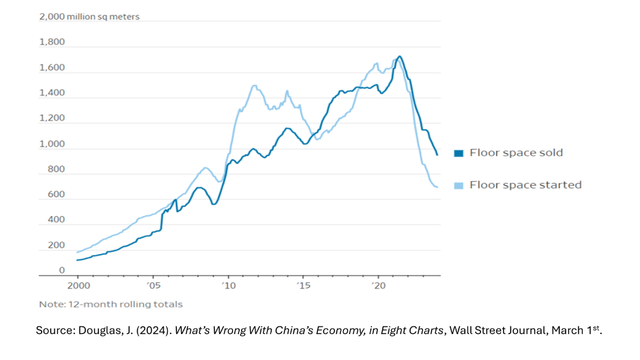

Six challenges may be recognized for China’s financial progress within the coming years. First, the exhaustion of the actual property sector as a progress issue, after having reached as much as 1 / 4 of the nation’s GDP. The restrictions established in 2021 by the Chinese language authorities on builders’ entry to low cost credit score, due to issues concerning the proportions reached by the actual property bubble, not solely reduce the increase, but in addition uncovered the fragility of builders’ belongings, as seen immediately within the case of Evergrande. Since then, there was a pointy drop in house gross sales, new building, and funding within the sector (determine 2).

Determine 2 – China: Residential Building and Gross sales

Wall Road Journal

Along with the extent of debt of fragile actual property corporations, the debt of native governments is one other downside. Particularly as a result of theirs revenues from the sale of land to actual property builders have shrunk. The diploma of publicity of Chinese language banks to each, with doable penalties by way of mortgage losses, may negatively have an effect on the provision of credit score within the financial system.

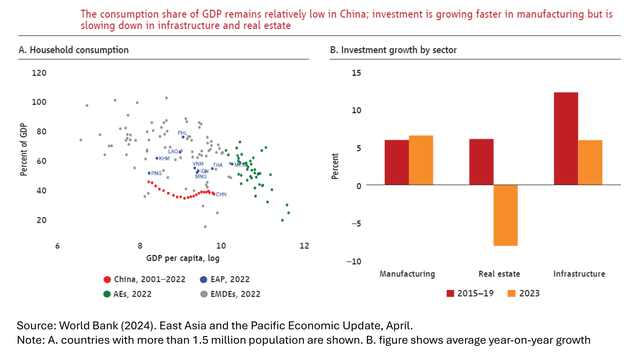

An issue with home demand by households represents a 3rd problem for progress. Chinese language households took on heavy debt to purchase actual property through the increase, and spending cuts accompanied the housing turbulence. Although it elevated after the tip of “Covid zero” final 12 months, consumption stays on a trajectory under that earlier than the pandemic (determine 3, left aspect). Measures of shopper confidence level to this.

Non-public investments for the home market, in addition to hiring, accompanied this retraction of home customers. Whereas funding in manufacturing saved tempo, it slowed down in actual property and infrastructure (Determine 3, proper aspect).

Determine 3 – China: Low Consumption and Investments

World Financial institution

What concerning the exterior sector as a type of compensation? A fourth problem to progress lies in exterior resistance to such a rise in exports in its place, provided that they now face the intensification of geopolitical rivalry overseas, particularly within the USA and different superior economies. Not by likelihood, a lot speak has been given to a “second shock” by way of Chinese language exports on the remainder of the world, significantly due to the dimensions of China’s figures this time.

The Chinese language lead in clear vitality expertise has, the truth is, been accompanied by a powerful growth, for instance, in gross sales of electrical vehicles overseas. Chinese language passenger automotive exports have surpassed Japan’s, whereas Chinese language corporations are searching for to strengthen positions overseas – comparable to BYD in Brazil, Hungary and elsewhere. However the dangers of dealing with extra market entry restrictions are excessive.

A fifth problem issues the unconventional change within the temper of overseas buyers. For the reason that third quarter of final 12 months, China’s steadiness of funds has recorded a web outflow of just about 12 billion {dollars} in direct funding, as a result of asset gross sales or non-reinvestment of income. Portfolio investments, that’s, shares and debt securities, additionally modified indicators.

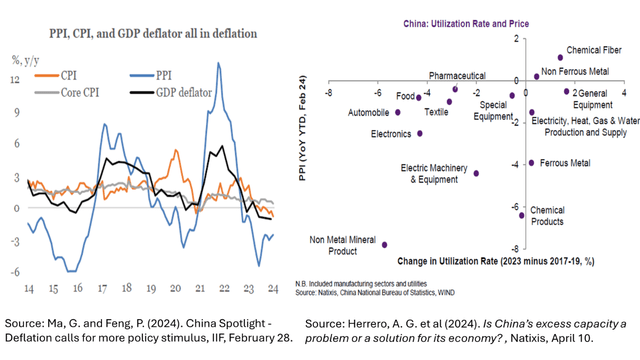

The insufficiency of mixture demand in China has been manifesting itself within the type of deflation within the home financial system. Client costs have been secure or falling for months and firms have been lowering costs for greater than a 12 months (Determine 4 – left aspect). Idle capability is excessive in lots of sectors, reflecting the surplus investments relative to ranges of demand (Determine 4 – proper aspect).

Determine 4 – China: Deflation and Capability Utilization Charges

IIF; Natixis

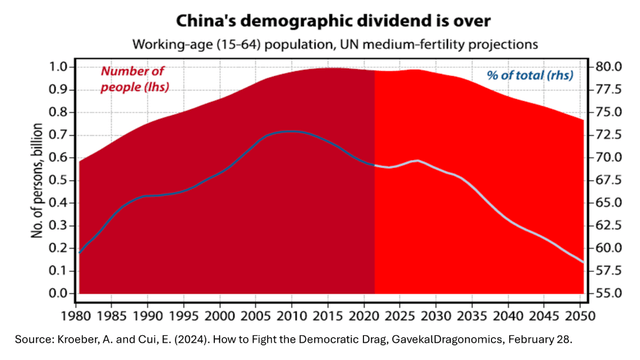

Demography constitutes a sixth problem. The rise within the provide of staff accompanying fast urbanization has reached its limits. The long-term decline within the variety of infants and the continued inhabitants decline, with a rising share of the inhabitants out of the job market, means – as in lots of different elements of the world – the tip of the demographic dividend (Andrade and Canuto, 2024) (Determine 5).The at the moment excessive youth unemployment price offers a supply of labor to be employed, however this doesn’t change the course on the difficulty of the proportion of Chinese language individuals of non-productive age.

Determine 5 – China’s Demographics

Gavekal

To know how the primary 4 challenges above intertwine, it’s price going again to the start of the final decade. In December 2011, when the author was one of many vice-presidents of the World Financial institution, I used to be at a ceremony in Beijing through which then-president Hu Jintao made one of many first statements concerning the want for an inevitable “rebalancing” of the Chinese language financial system. There must be a gradual redirection in the direction of a brand new progress sample, not related to funding charges near 50% of GDP and with home consumption growing in relation to investments and exports.

Additionally, stated Hu Jintao, an effort could be wanted to consolidate native insertion within the highest rungs of the added worth ladder in world worth chains, one thing that was successfully sought. Companies also needs to improve their weight in GDP in relation to manufacturing. There would not be the double-digit GDP progress charges of earlier many years, however progress would not be, as then-premier Wen Jiabao stated in 2007, “unstable, unbalanced, uncoordinated and unsustainable”.

Given the low stage of home consumption in GDP (a truth that’s nonetheless current) and, due to this fact, the dependence on investments and commerce balances, the transition would run the danger of experiencing an abrupt drop within the tempo of progress. To allay fears of an abrupt slowdown, waves of credit-driven overinvestment in infrastructure and housing adopted in later years. A second spherical was carried out in 2015–2017 in response to a housing slowdown and inventory market decline. As well as, in fact, to the growth insurance policies adopted through the pandemic disaster in 2020.

In impact, the decline in Chinese language GDP progress charges occurred solely progressively to six% in 2019. Now, nonetheless, the lever of overinvestment in actual property and infrastructure is working out. Not solely due to the debt ranges that accompanied its in depth use, but in addition as a result of, on the margin, its returns by way of GDP progress introduced a declining contribution.

Two reforms would have a powerful impact on progress (Canuto, 2022). First, reinforce social safety so as to persuade Chinese language individuals to avoid wasting much less. Moreover, resume the proposal made by Hu Jintao in 2011 – left apart by Xi Jinping – to “rebalance” private and non-private corporations, with a consequent acquire in productiveness as a result of variations favorable to the latter proven the place they function collectively.

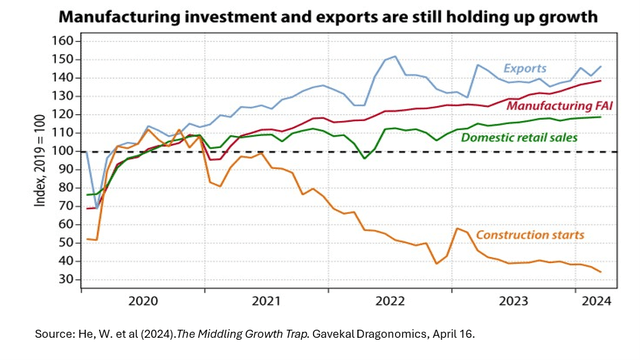

Such reforms don’t appear to be on the frontline forward. Nevertheless, regardless of the challenges approached right here, China’s financial progress path remained regular within the first quarter of the 12 months. Exports, manufacturing funding and travel-related shopper spending compensated for the drag from the property sector (Determine 5), thus far lifting the probabilities of reaching the goal of “round 5%” GDP progress this 12 months (He et al, 2024).

Determine 6 – China: progress regardless of the property sector drag

Gavekal

Authentic Put up

Otaviano Canuto, primarily based in Washington, D.C, is a former vp and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund, and a former vp on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil. Presently, he’s a senior fellow on the Coverage Heart for the New South, distinguished visiting scholar to the Worldwide Institute of Science and Expertise Coverage – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement.

{kind=link}