Kicking off one other earnings season for the tech trade, we as at all times begin issues off with Intel, who’s the primary massive chipmaker out of the gate. Over a yr into the coronavirus pandemic – and slowly heading out of it – Intel has seen its ups and downs as product calls for have shifted and the corporate’s potential to execute over the long run has been challenged by fab delays. Following a very painful (by Intel requirements) first quarter, the corporate is hoping to place these issues behind them with a stronger second quarter.

For the second quarter of 2021, Intel reported $19.6B in income, a decline of lower than $100M versus Q2’20, and what Intel is asking a flat distinction total. Extra importantly, maybe, is that Intel’s profitability has additionally held fairly regular (and considerably improved over Q1), with Intel reserving $5.1B in web revenue for the quarter, a YoY decline of 1%. General, with a lone caveat, Intel’s Q2 efficiency has exceeded their earlier projections.

Intel’s famed gross margin has additionally recovered on each a quarterly and yearly foundation. At 57.1% it’s up nearly 2 proportion factors increased than Q1, and nearly 4 proportion factors increased than Q2’20. Intel’s gross margin has been topic to larger than ordinary fluctuations as of late – usually dropping every time a significant new product is ramping – however not less than for Q2 it’s on the rise as Intel enjoys a really worthwhile quarter.

| Intel Q2 2021 Monetary Outcomes (GAAP) | |||||

| Q2’2021 | Q1’2021 | Q2’2020 | |||

| Income | $19.6B | $19.7B | $19.7B | ||

| Working Revenue | $5.5B | $3.7B | $5.7B | ||

| Internet Revenue | $5.1B | $3.4B | $5.1B | ||

| Gross Margin | 57.1% | 55.2% | 53.3% | ||

| Shopper Computing Group Income | $10.1B | -5% | +6% | ||

| Information Heart Group Income | $6.5B | +16% | -9% | ||

| Web of Issues Group Income | $984M | +8% | +47% | ||

| Mobileye Income | $327M | -13% | +124% | ||

| Non-Unstable Reminiscence Options Group | $1.1B | flat | -34% | ||

| Programmable Options Group | $486M | flat | -3% | ||

Breaking issues down on a bunch foundation, there are a few main factors to instantly take away. The primary is that, whereas nonetheless recorded per Typically Accepted Accounting Rules (GAAP) guidelines, Intel is all however prepared to chop unfastened its NAND reminiscence enterprise, which it’s within the technique of promoting to SK hynix. That stated, the deal has not been authorised and a time limit has not been set, so whereas Intel is opting to exclude it from their non-GAAP outcomes (and future enterprise projections), they aren’t freed from it fairly but.

Second, that is the primary full quarter that can be utilized for year-over-year comparisons with the coronavirus pandemic. Whereas Intel’s manufacturing aspect has lengthy since stabilized there, year-over-year numbers are typically in odd locations because the demand combine a yr in the past was very uncommon, to place it mildly.

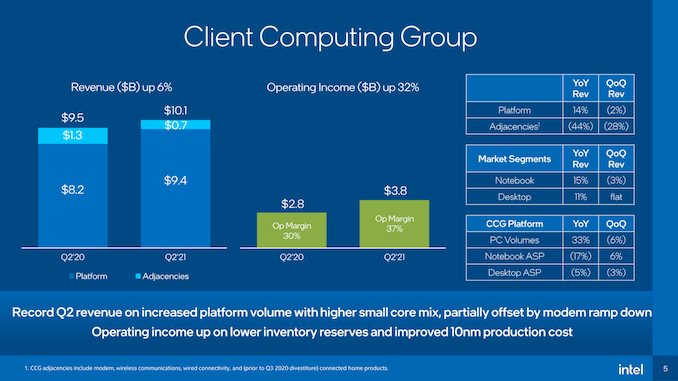

For Q2, Intel’s Shopper Computing Group was as soon as once more the most important winner; that division pulled in $10.1B in income, and is up 6% YoY. In keeping with Intel, each laptop computer and desktop income is up, as Intel has surpassed transport 50 million Tiger Lake processors. That stated, these income beneficial properties are largely volume-driven; ASPs for each desktop and cellular are down, due partially to what Intel is noting to be elevated gross sales of low core rely processors. Intel’s bettering fab state of affairs has additionally performed a component right here – in response to the corporate, 10nm manufacturing prices have dropped, serving to to enhance the division’s working revenue.

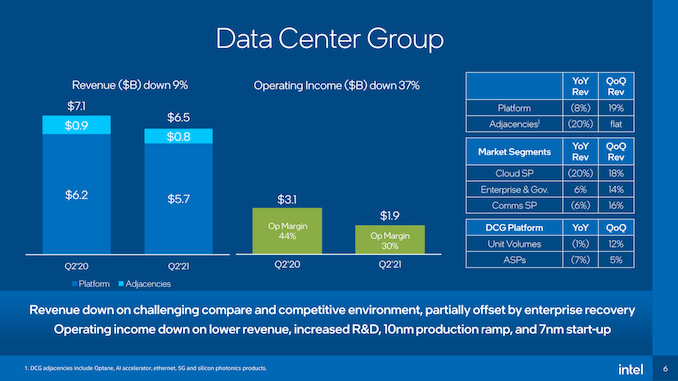

In the meantime Intel’s Information Heart Group is de facto beginning to really feel the influence of the more and more aggressive server setting. Whereas income was up 16% versus Intel’s powerful Q1, it’s nonetheless down 6% on a yearly foundation. Breaking that down additional, each cloud server supplier and communication gross sales are down, buoyed considerably by an uptick in enterprise and authorities gross sales. However with chip quantity and ASPs each down a bit, group income can solely fall. Intel has lengthy needed to get away from CCG main the corporate’s earnings – in massive half by rising its server revenues – however for the second it seems like that received’t be within the playing cards. Although as Intel continues to ramp up 10nm manufacturing (and thus Ice Lake Xeon manufacturing) there’s some alternative to get better in future quarters.

As beforehand talked about, Intel is seeking to reduce unfastened its NAND enterprise, which is now the one a part of the corporate’s Non-volatile Options Group (Optane is DCG). None the much less, for the second Intel nonetheless has to account for the group’s income, which is down 34% on a yearly foundation. As a result of Intel is downplaying the group a lot, they aren’t providing any significant written commentary on why revenues are down, however it will appear to be pandemic-related. NSG recorded a really massive bump in income a yr in the past, and issues have since fallen again in the direction of the trade baseline.

Rounding out Intel’s remaining divisions, each the ioT and Mobileye teams are up considerably on a yearly foundation, with income leaping 124% within the case of Mobileye. Each teams are benefitting from the post-pandemic restoration, in addition to further design wins within the case of Mobileye. In any other case, Intel’s last group, Programmable Options, noticed revenues decline a couple of p.c as a consequence of what Intel calls “stock digestion and provide constraints.”

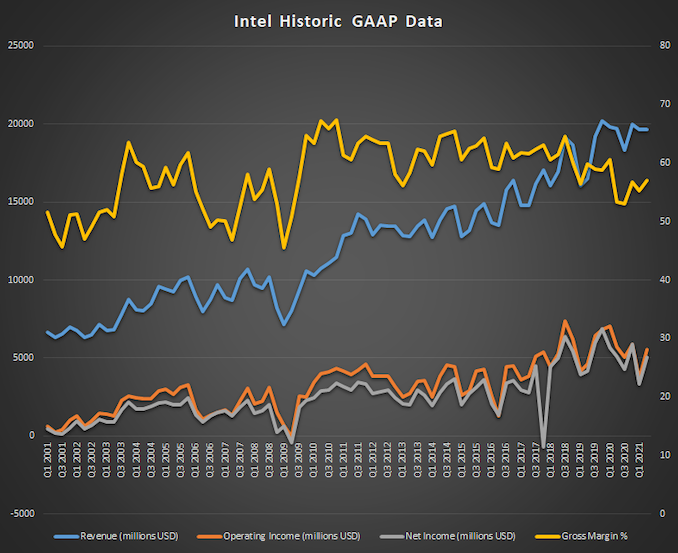

General, Q2’2021 marks a greater quarter for Intel on each a quarterly foundation and a yearly foundation. Together with recovering from their powerful Q1 three months in the past, Intel this yr isn’t going through one other fab delay, as Intel’s massive 7nm delay was first introduced as a part of their Q2’20 earnings. To make sure, the corporate is actually flat on income and revenue on a yearly foundation – whereas its competitors has usually grown – however as Intel will get additional into CEO Pat Gelsinger’s tenure, there’s growing confidence that Intel will hit its objectives (and a reducing window to overlook them).

Wanting ahead, primarily based on their stronger-than-expected Q2 efficiency and optimism about Q3 and past, Intel is growing its full-year steering. The corporate is now projecting income to develop on a yearly foundation, whereas gross margin projections stay unchanged at 56.5%. With that stated, Intel’s projections all exclude their NAND enterprise, with the corporate assuming that the deal shall be authorised by regulators this yr as initially deliberate.

Lastly, the subsequent massive enterprise replace from Intel will come on Monday, when Intel hosts its Intel Accelerated occasion. That webcast shall be targeted on Intel’s course of and packaging roadmaps, and is an enormous step in Intel’s efforts to determine their IDM 2.0 technique. We’re hoping to see extra on Intel’s 10nm and 7nm roadmaps there, in addition to extra on Intel’s next-gen packaging applied sciences. Within the meantime, Intel’s efforts appear to have not less than caught the collective ear of Silicon Valley, as the corporate has revealed at the moment that they’re in talks with 100 potential foundry prospects.

/cdn.vox-cdn.com/uploads/chorus_asset/file/25338407/3_Body_Problem_n_S1_E3_00_34_33_04RC.jpg_3_Body_Problem_n_S1_E3_00_34_33_04RC.jpg)

{kind=link}