SweetBabeeJay

Comcast inventory: Nonetheless a purchase regardless of latest rallies

I final wrote about Comcast Company (NASDAQ:CMCSA) a few yr and a half in the past. In that article, I argued for a BUY thesis primarily based on Warren Buffett’s rule of 10x EBT (earnings earlier than taxes). Specifically, I argued that:

As a number one inventory within the telecom sector, Comcast is buying and selling at its secular backside valuations. Beneath present circumstances, it’s equal to a ten%+ fairness bond with coupon progress built-in should you take into account their perpetual progress and Buffett’s 10x Pretax Rule.

Searching for Alpha

Quick-forward to now, the inventory has delivered a strong return, as seen on the chart above. It has loved a powerful value rally on high of beneficiant dividend payouts.

In opposition to this background, the thesis of this text is that the inventory has develop into a fair stronger match for the 10x EBT rule regardless of the big value rallies. Thus, within the the rest of this text, I’ll argue for an upgraded score on the inventory from BUY to STRONG BUY. And my argument can be anchored on three pillars: engaging valuation, long-term progress outlook, and near-term catalysts.

CMCSA inventory trades at 7x EBT solely

In tandem with the value developments since my final writing, CMCSA’s earnings have grown fairly a bit as properly. As such, the inventory at present trades at 9.53x of FWD EPS, as seen within the chart beneath. My projection for its efficient tax charges is round 26% within the subsequent few years. As additionally seen within the chart beneath, consensus EPS estimates for CMCSA inventory level to an EPS of $4.24 for FY 2024. At a 26% tax fee, its implied EBT for FY 2024 would then be ~$5.72 per share. On the market value of $40 as of this writing, this interprets right into a P/EBT ratio of solely 7x.

Now it’s a very good time to introduce Buffett’s 10xEBT rule so we will higher contextualize the 7x EBT. For readers who by no means heard about it, my weblog article gives an in depth account. The gist is highlighted beneath for simple of reference:

The grandmaster paid ~10x pretax earnings for a lot of of his largest and greatest offers. The record is a very lengthy one, starting from Coca-Cola, American Categorical, Wells Fargo, Walmart, Burlington Northern, and the newer Apple. That is hardly a coincidence as a result of:

- The very best fairness investments must be bond-like. Once we converse of bond yield, that yield is pretax. So, a 10x EBT would offer a ten% pretax earnings yield, instantly corresponding to a ten% yield bond. Any progress can be a bonus.

- A second purpose why the rule makes good sense is that after-tax earnings don’t mirror enterprise fundamentals. Taxes can change attributable to components that haven’t any relevance to enterprise fundamentals, and there are many methods for an organization to optimize its tax obligations.

As such, an EBT a number of of 7x is just reserved for shares which can be completely unwell or stagnant in my thoughts. Nonetheless, within the case of CMCSA, I see the other – I see each wholesome progress within the close to time period and long run. Consensus estimates appear to share the identical view. As seen, their estimates suggest a CAGR of 8.1% for its EPS progress within the subsequent 5 years. Subsequent, I’ll clarify why I believe such a projection could be very believable.

Searching for Alpha

CMCSA inventory’s long-term progress prospects

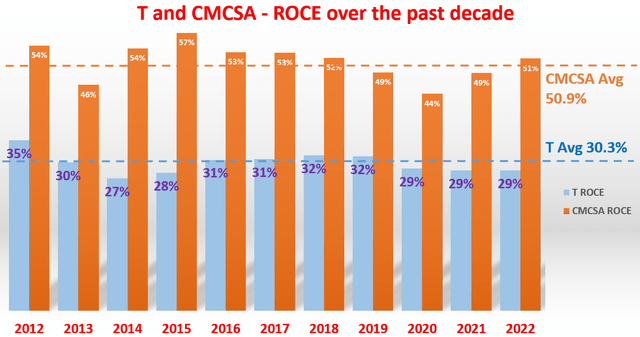

My technique for estimating progress charges in the long run includes using ROCE and reinvestment charges. The main points are offered in my different articles, and I’ll simply quote the ultimate numbers right here:

The tactic includes the return on capital employed (“ROCE”) and the reinvestment fee (“RR”). The ROCE for CMCSA has been round 51% in the long run as seen within the chart beneath. Its RR is about 10% on common. With these inputs, CAT’s perpetual progress fee can be ~5.1% (51% ROCE x 10% RR = 5.1%). Word this quantity is the actual progress fee with out inflation. To acquire a notional progress fee, one would wish so as to add an inflation escalator.

If we assume a mean inflation escalator of two.5%, this could convey the nominal fee to 7.6%, fairly near the CAGR of 8.1% implied within the consensus estimates talked about above.

Creator

CMCSA inventory’s near-term catalysts

Now, let me swap the main target to the near-term catalysts. There are a couple of sturdy catalysts within the subsequent 1~2 years that might enhance CMCSA firm considerably in my opinion. The highest one on my record is the broadcasting of the Summer time Olympics. This yr’s Olympics occasion is scheduled to kick off in Paris on July twenty sixth and final by way of August eleventh. CMCSA expects its Peacock to supply “essentially the most complete streaming vacation spot ever for the Olympic Video games.” The second near-term catalyst includes the U.S. presidential election later this yr. I anticipate these occasions to create tailwinds for the corporate’s promoting income from the fanfare related to the Olympics and likewise elevated political marketing campaign spending.

Lastly, the final catalyst on my record includes the debut of Orlando’s Epic Universe, which is scheduled for 2025. In accordance with administration, Epic would be the first main amusement park to open within the U.S. in years. It covers greater than 480 acres and options 4 themed lands linked to one another by a singular gateway. Extra particularly, Epic consists of in style company-owned and licensed franchises, together with Nintendo’s Tremendous Mario Brothers, Harry Potter, and characters from the How To Prepare Your Dragon movie collection.

Draw back dangers and ultimate ideas

On the draw back, CMCSA faces largely the identical set of dangers frequent to its telecom friends. As well as, there are additionally some dangers which can be extra explicit to CMCSA however to not different telecom shares. The dangers which can be frequent to CMCSA and its friends embody value competitors, regulation adjustments, and likewise intense infrastructure prices. Right here I’ll deal with the dangers which can be extra peculiar to CMCSA. Given its historical past and legacy operations, Comcast is more likely to expertise additional weak point inside the conventional cable enterprise. Such legacy companies are extra delicate to the disruptions of latest applied sciences. In the USA, video subscriber losses have averaged over two million a yr since 2022 as a result of rising recognition of each cheap streaming providers and social media platforms like TikTok, YouTube, and Instagram. CMCSA is responding with its personal Peacock streaming platform.

Nonetheless, Peacock continues to be in an early stage in my opinion and its future stays unsure. It made notable progress in 2023, with the overall variety of paid subscribers rising 50% to roughly 30 million. Nonetheless, the service has but to report an working revenue. In the meantime, Peacock continues to face intensifying competitors from streamers that get pleasure from a lot larger scale, with Netflix and Disney+ main the pack when it comes to variety of subscribers.

To conclude, the upside dangers far outweigh these draw back dangers in my opinion. As such, this text argues for an upgraded score on CMCSA to Sturdy Purchase regardless of the big value developments since my final protection. The upgraded score was primarily primarily based on three concerns: engaging valuation, long-term progress outlook, and near-term catalysts. Regardless of latest value rallies, the inventory’s valuation stays very engaging because of earnings progress. Its P/EBT ratio is just 7x for FY 2024, a a number of solely reserved for terminally unwell/stagnant shares in my thoughts. But, I see strong progress catalysts in each the close to time period and long term. Specifically, consensus projected progress charges recommend a CAGR of 8.1% over the subsequent 5 years, which could be very believable to me because of its sturdy ROCE and reinvestment charges sustained by its sturdy money era.

{kind=link}