The Good Brigade

Overview

My suggestion for Constellation Manufacturers (NYSE:STZ) is a purchase ranking, as I proceed to count on sturdy efficiency within the foreseeable future. The sturdy demand momentum appears to have continued into 1Q25 (1CQ24), which units FY25 (CY24) to a really sturdy begin. Whereas Beer’s phase gross margin appears poor on a headline foundation, EBIT truly fared fairly properly. With the incremental value financial savings and working leverage from extra quantity gross sales, I imagine Beer’s EBIT margin can maintain itself at this degree (with the potential to enhance). Observe that I beforehand rated purchase ranking as I anticipated sturdy efficiency by way of FY25 and that 4Q24 might outperform steering as 4Q23 was a simple comp quarter.

Latest outcomes and updates

STZ reported a really sturdy 4Q24 quarter, as I anticipated, the place whole web gross sales grew 7.1% to $1.998 billion, all pushed by the beer phase development of 10.9%, offset by a 5.6% decline in Wine & Spirits. Robust Beer efficiency didn’t finish on the prime line. Whereas Beer’s value of products offered noticed some inflation, resulting in gross revenue rising slower than 10.9%, Beer’s EBIT grew quicker than 10.9%, suggesting very sturdy working leverage (Beer EBIT grew 11.9%). On the backside line, blended EPS noticed $2.30, which beat consensus estimates of $2.12 by ~8.5%. STZ’s sturdy efficiency proved that my view of the enterprise was proper, particularly the beer phase, and I proceed to imagine STZ can proceed to trip on this momentum because it has visibility to sturdy quantity development and margin restoration.

STZ outcomes get even higher once we dig deeper into the drivers of Beer’s sturdy phase efficiency. Firstly, beer depletions got here in at 8.9%, which, when adjusted for the additional promoting day, underlying efficiency was nonetheless very sturdy at 7% when contemplating that the trade noticed a tricky begin to the 12 months given poor climate situations within the states. The market was clearly frightened about this, because the share value fell sharply in January from ~$260 to close $240. The amount efficiency confirmed that STZ is resilient even in opposition to this dangerous climate, and it seems that quantity demand momentum continued into 1Q25 as administration cited “sturdy efficiency” to begin the 12 months. For administration to say that 1Q25 is “setting us off on a extremely strong 12 months” means that they’re seeing no main indicators of slowdown. Furthermore, STZ is seeing low-double-digit share incremental shelf house good points at retail by way of the spring resets, which ought to present a sell-in increase to STZ as they should speed up delivery to refill these new shelf good points to satisfy demand. All in all, these components are main me to imagine STZ goes to see a powerful FY25 as properly for its beer phase.

Positive. We clearly take into consideration our March outcomes with our total expectations for the 12 months. However I might say, March was very per what our expectations had been. Everybody ought to remember that March has two much less promoting days, April has two extra. So we internally have a look at it as type of the combo plan of these two months. With that mentioned, we had a really comfortably sturdy March, as we anticipated that we might, and assume it is setting us off on a extremely strong 12 months, as we mentioned, per what we mentioned on the Investor Day in New York.

in my major remarks, low double-digit shelf house is what we anticipated to get, and that is, actually, what we’re getting in spring resets. Clearly, it varies everywhere in the map relying, however that is roughly what the whole quantity is within the mixture. And once more, that is no less than as a lot as we anticipated. We’re very happy with the place that landed. From 4Q24 earnings name

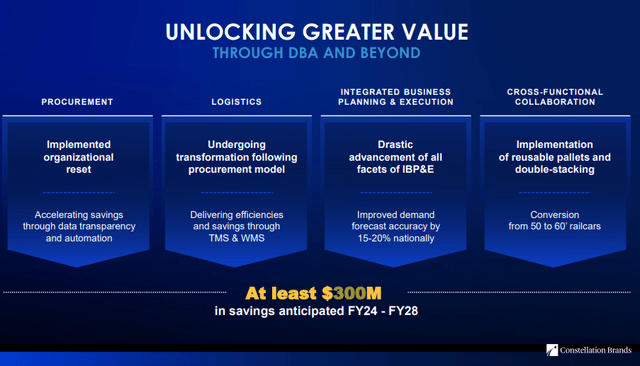

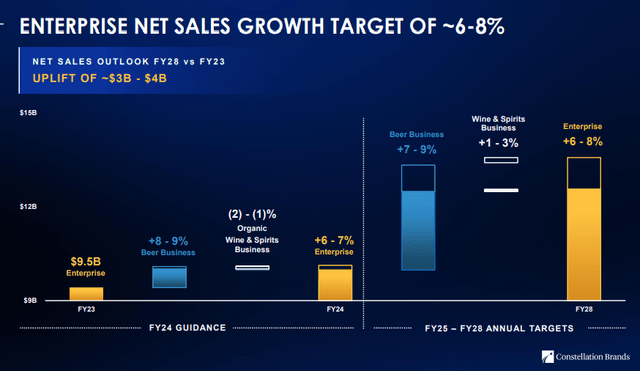

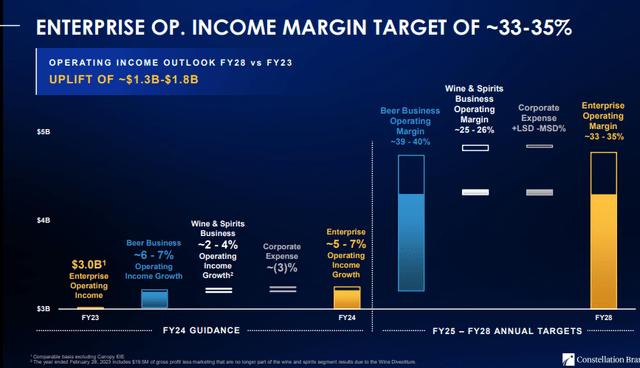

As I famous earlier, the one disappointing side is the decline in gross margin for the beer phase from 50.8% to 49.8%. I do not assume buyers ought to be too frightened about this, as on a like-for-like foundation (adjusting for the VAT accrual write-off), gross margins would have been 50.8%, according to 4Q23. With this thought in thoughts, it truly paints an excellent higher image for EBIT margin, which noticed 40bps growth on a reported foundation however would have been 140bps with out the VAT accrual write-off. Nonetheless, the spotlight right here is that STZ has managed to proceed realizing productiveness financial savings (that was talked about in the course of the November Investor Day). I’m constructive that margins can no less than maintain themselves at this degree, with the potential to develop as STZ ought to profit from the price financial savings initiatives carried out in FY24 and incremental tasks as a part of the outlined $300 million financial savings by way of FY24-FY28. Lastly, there may be the inherent working leverage to take into consideration. As STZ goes to proceed rising beer volumes, there ought to be a margin profit there as properly.

STZ

Valuation and danger

Writer’s valuation mannequin

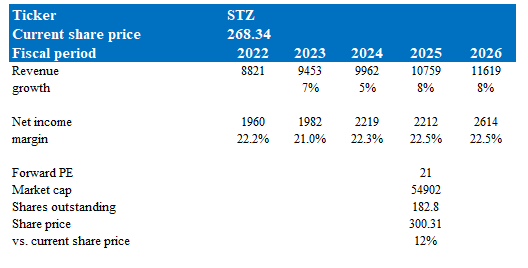

In keeping with my mannequin, STZ is valued at $300 in FY25, representing a 12% improve. This goal value relies on my development forecast of 8% in FY25 and FY26, which relies on administration long-term steering that I feel is achievable given the efficiency to date. On web margins, I’m not modeling an aggressive growth in margins, as administration steering is for minimal EBIT margin enhancements. I’m leaving any upside within the margins as further upside. Given these expectations, I’d count on STZ to commerce no less than at its historic common ahead PE degree (21x). I feel the rationale why the market has not re-rated the valuation is as a result of they’re frightened about Beer’s phase gross margin efficiency. Finally, as STZ reveals EBIT margin enchancment (or sustains at this degree), this concern ought to go away and multiples ought to go up.

STZ

STZ

Threat

Wine & Spirits continues to be disappointing, with income down 5.6% and EBIT down 13.1% in 4Q24, exhibiting little indicators of enchancment. If this continues to slowdown, seemingly because of the macro atmosphere forcing shoppers to eat cheaper alternate options, it might proceed to function a headwind to gross sales. The excellent news is that this can be a a lot smaller portion of the enterprise (~20% of EBIT), in order it declines, the incremental impression turns into smaller.

Abstract

Summarizing this put up, the advice for STZ stays a purchase because of the continued sturdy efficiency within the Beer phase. Regardless of a slight dip in Beer’s gross margin, the phase’s EBIT margin grew, indicating sturdy working leverage. Administration’s feedback concerning a “very comfortably sturdy March” and “low-double-digit shelf house good points” additional solidify the constructive outlook for FY25. Whereas Wine & Spirits continues to underperform, its smaller measurement minimizes the draw back danger. With a value goal of $300, I imagine gives compelling upside potential because the market acknowledges its sustained momentum.

{kind=link}