slobo

Costco (NASDAQ:COST) continues to develop at an distinctive charge because the agency continues so as to add new retail places, each home and worldwide. The agency has proven power in including new shops, even when situated inside areas with current places. This progress has allowed administration to extend shareholder worth by each dividends and buybacks, growing the quarterly dividend to $1.16/share. I imagine that Costco has a big edge in rising their worldwide retail footprint as their new Shanghai location was met with exceptionally robust reception. The agency can be hitting the pavement in increasing their eCommerce platform with improved y/y gross sales of 18.2% inside the phase. Although COST shares commerce at a big premium at 30.14x TTM EV/EBITDA, I imagine the agency’s operational excellence and constant progress justifies this excessive premium. I charge COST shares with a BUY advice with a value goal of $760/share.

Please learn my preliminary December 31, 2024 thesis masking Costco.

My thesis on Costco stays as a BUY advice with a richer value goal of $760/share. I imagine that I undervalued Costco’s dynamic price-savings technique, which has additional pushed power in membership renewal charges and a extra devoted buyer base. I imagine the improved retention charge from 90.50% to 92.9% supplies robust proof for this. Full disclosure, I purchased a Ninja 12-piece cookware set and a chopping block on their eCommerce web site whereas updating my firm analysis.

Operations

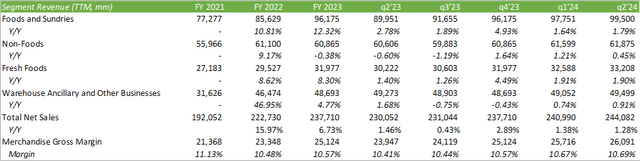

Costco continues to indicate resilience of their progress technique regardless of the excessive ranges of inflationary pressures felt by the customers. Administration has remained adamant in sustaining their worth to households by successfully managing their stock purchases and passing alongside the associated fee financial savings to the customers. This has resulted in a robust renewal charge of 92.9% for q2’24 within the US & Canada with 73.4mm paid family members and 132mm card holders, up 7.8% and seven.3%, respectively. Government membership additionally grew by 636,000 in q2’24 to 33.9mm. In consequence, membership charges grew by 8.2% to $1.111b. Web of gasoline deflation and foreign exchange, identical retailer gross sales grew by 5.8% in q2’24 with vital power throughout their Canadian and worldwide markets. I imagine eCommerce progress is noteworthy as gross sales within the phase grew by 18.4%, suggesting additional power within the agency’s capacity to compete with different massive field on-line retailers.

Company Reviews

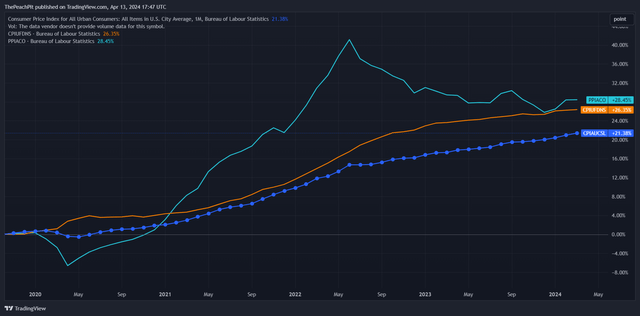

Trying previous q2’24 outcomes, Costco reported an enormous 7.45% enhance in retail gross sales of their March gross sales report, with 28% progress in eCommerce. Contemplating trailing twelve-month gross sales throughout segments, Meals & Sundries and Recent Meals stay a driving power for the corporate’s topline progress. I count on that as customers proceed to be burdened by excessive meals inflationary pressures, retailers like Costco will profit because the agency passes alongside financial savings by procurement alongside to clients as the associated fee advantages move by.

TradingView

This permits the agency to behave extra nimbly within the aggressive, tight margin enterprise. I imagine this has led customers to proceed buying Costco’s signature Kirkland merchandise. By rising their black label footprint, Costco has retained vital flexibility on pricing throughout all premium objects, from batteries to frozen meals. One instance given on the q2’24 earnings name was the agency’s capacity to scale back the worth of their frozen Three-Berry Mix from $14.99 all the way down to $10.99 given the brand new crop pricing. On a monetary foundation, pricing variations have resulted in a 2bps enchancment to gross and working margins on a TTM foundation. I imagine these gradual enhancements play out to Costco’s benefit because it permits the agency the pliability to bolster monetary flexibility whereas sustaining buyer loyalty and satisfaction.

Company Reviews

Costco added 4 new places for a complete of 874, 602 of that are situated within the US. Administration anticipates the power to proceed including round 25 websites per yr earlier than growing their progress charge to nearer to 30. When posed with the priority of cannibalization, administration discerned that offering location optionality inside areas improved whole gross sales between the regional websites. I anticipate that location densification is necessary for Costco because the agency scales places inside the identical areas as present places are oftentimes overrun with crowds, making it difficult for consumers to navigate all through the shops. My private idea is that this may occasionally relieve a number of the nervousness for some consumers and permit for a extra relaxed, much less crowded setting during which to buy. This may occasionally lead consumers to discover extra aisles and hunt down bargains versus executing their buying journey in strict accordance with their checklist. Although I don’t anticipate this to drive massive ticket gross sales like TVs, it might drive gross sales for smaller home equipment, ready meals, alcohol, amongst different objects which will supply extra selection and shelf enchantment.

Costco additionally just lately introduced their choices of weight administration packages by healthcare market supplier, Sesame. This service will value members a quarterly charge of $179 that may embrace video session with a weight-loss specialist, GLP-1, or a weight-loss prescription. I imagine that this may occasionally turn out to be a preferred providing by Costco within the midst of Ozempic hitting the market with a splash.

Company Reviews

By way of monetary efficiency, I count on Costco to proceed to carry out with power throughout all gross sales segments, significantly in Recent Meals and Meals & Sundries. I anticipate power in home equipment as properly, as it is a rising phase for the agency. Mr. Galanti identified on the q2’24 earnings name that equipment gross sales grew north of 20% for Costco when in comparison with flat for the business. I imagine that Costco can supply a singular alternative for equipment gross sales going ahead because the retail websites double as distribution facilities, permitting the agency to execute same-day supply for in-stock objects at their regional location when clients buy by eCommerce. This function may additionally additional drive eCommerce progress for Costco because the agency can modestly compete with different on-line retailers, reminiscent of Amazon (AMZN) and Walmart (WMT). Although Costco doesn’t supply as broad of a spread of companies as these two companies, I imagine Costco’s return coverage bolsters shopper confidence in on-line buying because the agency affords 100% risk-free returns for 90 days for all electronics.

Company Reviews

Regardless of my bullish sentiment on the corporate, managing expectations are vital as the worldwide financial system teeters on recessionary pressures paired with traditionally excessive inflationary charges. Dynamic pricing doesn’t at all times work in favor of the buyer as costs could elevate in periods of upper meals inflation from the producer’s perspective. Increased costs could deter customers from making greater purchases like home equipment and electronics as they focus their budgets on requirements, reminiscent of recent meals and sundries. This may occasionally lead to tighter margins for Costco, decrease gross sales volumes, decrease free money move technology, and better shrink, or spoilage. Contemplating my analysis masking shopper electronics components designers and producers, reminiscent of Qualcomm (QCOM), Broadcom (AVGO), Dell (DELL), Hewlett Packard Enterprise (HPE), and Roku (ROKU), I do anticipate a softening in shopper spend on this class for eCY24 ensuing from these heightened inflationary pressures.

Valuation & Shareholder Worth

My thesis on Costco stays as a BUY advice with a richer value goal of $760/share. I imagine that I undervalued Costco’s dynamic price-savings technique, which has additional pushed power in membership renewal charges and a extra devoted buyer base. I imagine the improved retention charge from 90.50% to 92.9% supplies robust proof for this. Full disclosure, I purchased a Ninja 12-piece cookware set and a chopping block on their eCommerce web site whereas updating my firm analysis.

Please learn my preliminary December 31, 2024 thesis masking Costco.

Company Reviews

Costco continues to reward their shareholders by their buybacks and dividend packages. In q2’24, Costco repurchased 240k shares for $159mm in addition to paying out their $15/share particular dividend on the finish of CY23. Along with the particular dividend, administration elevated the recurring quarterly dividend charge to $1.16/share. I imagine administration will proceed rewarding shareholders with their steadily growing dividend charge together with their periodic particular dividend. Along with this, I imagine that administration will proceed shopping for again shares to compound shareholder worth. Although administration doesn’t present ahead steerage, I imagine administration will elect to distribute their extra free money move. Although I anticipate a slight pull on free money move for eFY24, I do anticipate an upswing going by eFY25. I imagine offering these shareholder values will justify buyers remaining invested within the inventory given the upper valuation.

By way of valuation, COST shares are at the moment priced on the larger finish of their historic valuation at 30.14x TTM EV/EBITDA. Although the valuation could be thought of costly, I imagine the standard of execution Costco brings to the desk justifies their valuation premium. Modeling financials out to 2025, I imagine the inventory may have room to develop at a goal charge of 4% to $760/share. I present COST a BUY advice at 29.39x EV/EBITDA.

The blue-sky situation denoted under would recommend the agency outperforms on new cardholder acquisition, strengthened retention, and stronger gross sales and margins consequently. I imagine that the grey sky situation could be pushed by inflationary pressures and decrease shopper spending at Costco places. The goal denotes my expectations for the agency’s efficiency over the course of the following 1.5 years. I imagine the chance issue supplies a extra doubtless value goal based mostly on these three situations.

Company Reviews

{kind=link}