ipopba/iStock through Getty Photos

Funding Thesis

Digital Turbine (NASDAQ:APPS) has been on a horrible curler coaster experience, the place almost everybody that has been related to its inventory right this moment is extra possible than not holding a loss.

And when your entire shareholder base is probably going to be holding a loss, it does one thing to all stakeholders, together with workers’ motivation, as their stock-based compensation will now be price considerably lower than it was perceived to be price only a yr in the past.

As we speak, Digital Turbine is a shadow of its former self. That being mentioned, I imagine that once we come out of this financial downturn, promoting shares would be the ones that can bounce again first, in the identical approach as they had been the primary to show decrease as macro headwinds mounted in 2021.

Nonetheless, I now revise my EBITDA estimates given this new macro surroundings.

I imagine that APPS is being priced at round 40x depressed EBITDA. Nevertheless, as soon as we get previous the subsequent six months, and the economic system reestablishes its footing, I imagine adtech shares can be amongst the primary to bounce again.

In sum, it isn’t instantly apparent why paying 40x depressed EBITDA might be low-cost, so learn on.

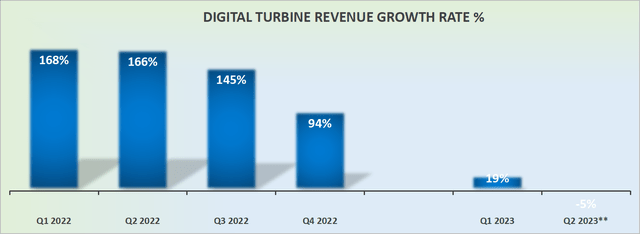

Digital Turbine’s Income Progress Charges Gradual Down

APPS income development charges

As I highlighted in my earlier article, the desk above is Digital Turbine’s income development charges adjusted for its latest change in accounting, from a gross to web foundation.

Realistically, most buyers have come to phrases with fiscal 2023 being a write-off for Digital Turbine.

However as Digital Turbine now has had loads of time to combine its three acquisitions and restructure its enterprise for the brand new financial actuality, I imagine that Digital Turbine may quickly flip a nook.

And this is why.

What’s Subsequent for Promoting Shares?

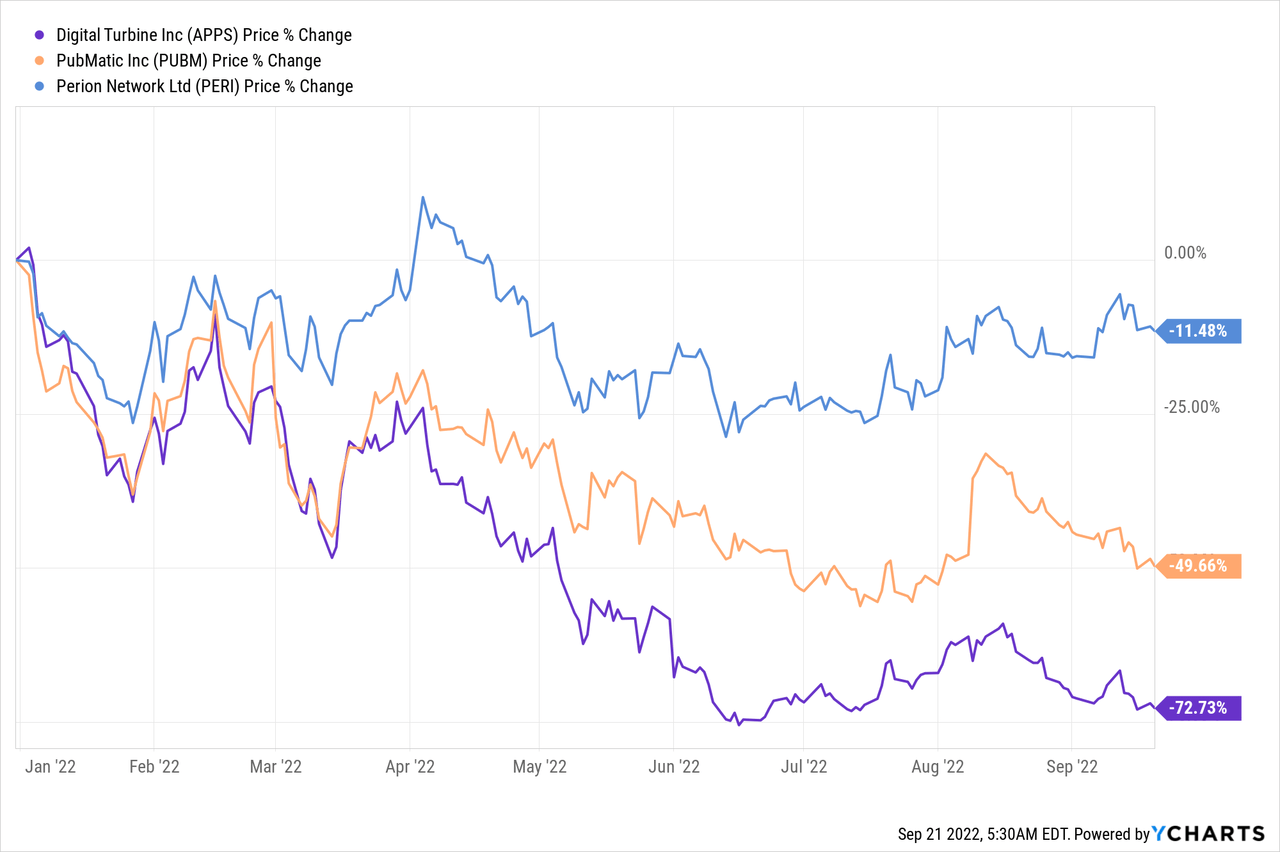

As famous within the introduction, promoting shares had been one of many first sectors to show destructive on this bear market. In actual fact, wanting again, small and medium-cap shares began to show decrease in February 2021.

On the time I strongly believed that the market had received APPS fallacious. I used to be pounding my fist on the desk that the inventory was undervalued.

However as I’ve already said right here, I had to surrender this holding in March 2022. In hindsight, it seems to have been a prescient name, because the inventory proceeded to unload.

Clearly, the market was proper to be anxious about Digital Turbine and different adtech corporations.

As you’ll be able to see above, the entire group has been out of favor with buyers. With Digital Turbine by far faring the worst.

But I cannot be so courageous as to say that the underside for Digital Turbine is right here.

What I can declare is that we’re lots nearer to the underside than the highest. Thus, the risk-reward from this level is considerably extra engaging than it has been at any level prior to now yr.

Here is what we all know now. We’re very more likely to be eyeing up a recession within the US if we aren’t already in a recession.

However we even have to notice that in the identical approach as promoting spending is the primary to get pulled because the economic system slows down, it’s going to even be amongst the primary to get elevated because the economic system will get again on regular footing.

However what’s additionally true is that the inventory market will begin to inflect forward of financial knowledge. Bear in mind, after all of the market is a number one indicator of financial exercise.

Spending Via the Cellphone is a Actual Development

Many Asian markets look like extra predisposed to cellular e-commerce. Lately I echoed Coupang’s (CPNG) assertion that by 2025 Korea is anticipated to grow to be the third greatest eCommerce nation behind China and the US and forward of the UK and Japan.

Thus, there’s an simple pattern for us to spend extra time on cellular gadgets, and even with out a lot additional improve within the variety of handsets, Digital Turbine’s Android base (GOOG)(GOOGL) ought to enable it to proceed to extend its revenues per gadget, a metric that Digital Turbine has up till not too long ago shared with buyers as a way to trace its progress in its working metrics.

Digital Turbine’s CEO Invoice Stone believes that regardless that gross sales cycles have grow to be elongated within the present enterprise cycle, this is not a everlasting shift in promoting budgets.

We’re merely in unchartered territory of slowing financial development plus excessive inflation. However corporations that wish to improve their gross sales might want to spend on promoting to succeed in shoppers the place they discover themselves, on their cellular gadgets.

APPS Inventory Valuation – 40x EBITDA

Digital Turbine is an adtech firm. And one factor that this sector does rather well is report robust free money flows.

That being mentioned, I do not imagine that it is smart to offer any credence to the forecasts that Digital Turbine gave again on its Investor Day this time final yr.

Nonetheless, I do imagine that is fully doable that Digital Turbine’s EBITDA may attain no less than $170 million of EBITDA. Here is the math, fiscal Q1 2023’s EBITDA was $51 million, whereas Q2 2023 is guided for $50 million.

Given the slowing macro surroundings mentioned, it is fully doable that H2 2022 may solely see round $70 million.

That is lower than $195 million reported in fiscal 2022. Nevertheless, the macro surroundings for the subsequent six months is anticipated to be extra restrictive than the identical interval a yr in the past.

Thus, a method or one other the inventory right this moment is priced at round 40x depressed EBITDA.

Consequently, the market has been justified in promoting off this inventory. Realistically, on condition that Digital Turbine is priced at 40x EBITDA the corporate must be delivering sustainable income development and it isn’t.

However, it is possible that after we get previous the subsequent six months of financial malaise, Digital Turbine is nicely positioned to get extra pockets shares from manufacturers seeking to get nearer to the patron.

The Backside Line

There isn’t any denying that cellular promoting is a long-term pattern that’s right here to remain. The one query that is left is whether or not or not Digital Turbine will be capable of efficiently seize sufficient market share.

Proper now, there’s solely concern, uncertainty, doubt, and pessimism.

But, I imagine that anybody that’s studying this has had loads of time to ask critical questions on their APPS funding.

Or put one other approach, I imagine that anybody that wished out from this inventory is both out now, or more likely to be out within the coming weeks, after Q3 2022, as we get into tax loss season.

In sensible phrases that signifies that the marginal vendor of this inventory can be out of this identify over the subsequent month or two. And what’s left can be solely buyers that will not promote at any price. And at the moment, will probably be a really attention-grabbing time to revisit this identify.

{kind=link}