Brett_Hondow

It was one other robust earnings season for the restaurant {industry} (EATZ), with lowered gross sales leverage resulting from weaker site visitors tendencies mixed with one other quarter of elevated wage/commodity inflation. Nonetheless, regardless of the softer outcomes, most informal eating names shrugged off the dangerous information. In Dine Manufacturers’ (NYSE:DIN) case, the inventory posted stable outcomes, however its post-earnings rally was interrupted by a resumption of the cyclical bear market within the S&P 500 (SPY).

Whereas the backdrop for informal eating shares stays difficult resulting from a good labor market, rising meals prices, and a weaker shopper, Dine Manufacturers’ franchisees are in stable form and positioned effectively from a requirement standpoint. It’s because it advantages from a a lot decrease common verify than manufacturers like Outback Steakhouse (BLMN) and Purple Lobster, that means that even with taking value, it stands out as an inexpensive choice for households/{couples} anxious to get out for leisure. Given this enviable positioning, I see DIN as a good buy-the-dip candidate if we see additional weak spot.

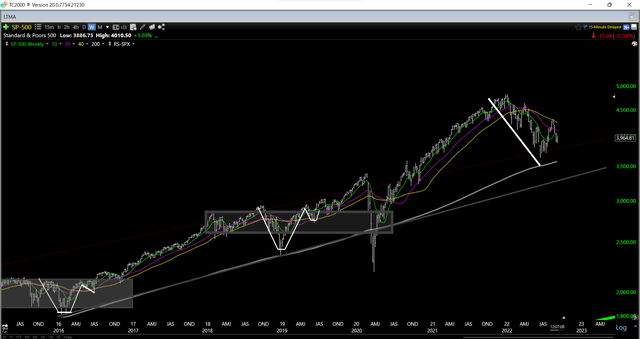

S&P 500 Weekly Chart (TC2000.com)

Q2 Outcomes

Dine Manufacturers launched its Q2 outcomes final month, reporting quarterly income of $237.8 million, a 2% enhance from the year-ago interval. This was helped by low single-digit comparable gross sales progress at each of its manufacturers, with Applebee’s reporting 1.8% comp gross sales progress (12.5% vs. 2019) and IHOP reporting 3.6% comp gross sales progress. Notably, off-premise gross sales (supply and pick-up) stay sticky for each manufacturers, with Applebee’s and IHOP exiting the quarter with over 21% combine from off-premise and weekly gross sales of $13,900 and $8,300, respectively.

Applebee’s Menu Choices (Firm Presentation)

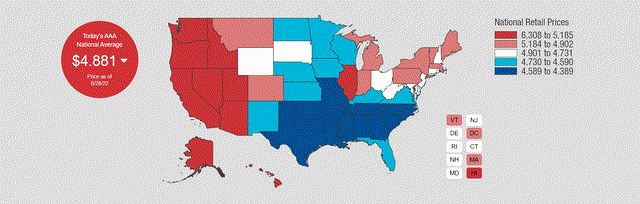

If we have a look at Dine Manufacturers’ income development beneath, it could be weaker than a few of its friends, however gross sales have held up fairly effectively, contemplating the headwinds. Like different firms, Dine Manufacturers famous that it did see some pullback from its lower-income visitor later within the quarter, with the stable April and Could gross sales partially offset by spiking fuel costs later within the quarter. Thankfully, fuel costs have declined significantly from their peak above $5.00/gallon, enhancing to $3.75/gallon this week. Given this affect on discretionary budgets, this might arrange Dine Manufacturers for a greater September than deliberate, with fuel inflation cooling off faster than anticipated.

Nationwide Fuel Costs (AAA Fuel Costs)

Dine Manufacturers – Quarterly Income (Firm Filings, Creator’s Chart)

Digging into operations somewhat nearer, Applebee’s is planning to increase its Cosmic Wings digital model to its Applebee’s core menu, much like what Denny’s (DENN) is doing with It is Simply Wings. It is also persevering with with strategic discounting vs. freely giving {dollars}, providing a dozen shrimp for $1.00 when company order a steak, and bringing again All You Can Eat with a wing deal, providing All You Can Eat boneless wings for $12.99. At IHOP, the corporate famous that its Worldwide Financial institution of Pancakes launch exceeded expectations, with 2 million loyalty members (30% new to the model) now incomes ‘PanCoins’.

IHOP Restaurant (Firm Presentation)

Prices & Earnings Development

Sadly, whereas gross sales had been stable and Applebee’s is extra protected than friends with its main franchise mannequin within the informal eating house, commodity prices remained elevated in Q2. Commodity inflation got here in at 22%, and whereas it’s going to enhance to low teen ranges in H2, it impacted adjusted EBITDA within the interval. The mix of elevated G&A and inflation led to an 8% dip in adjusted EBITDA (66.1 million vs. $71.7 million) regardless of the slight enhance in income. Dine Manufacturers famous that the rise in G&A was associated to travel-related prices to help franchisees and strategic progress initiatives.

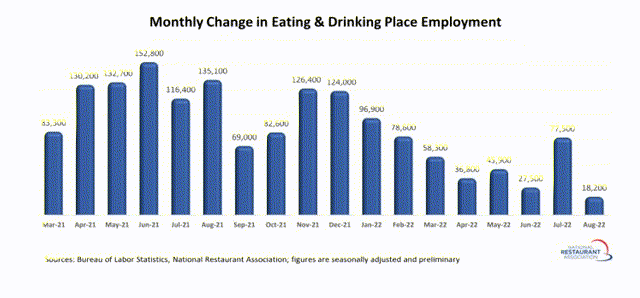

Month-to-month Consuming & Ingesting Employment (Nationwide Restaurant Affiliation, BLS)

On the constructive aspect, whereas staffing stays a problem industry-wide, IHOP noticed a rise in eating places open at common working hours, with 91% now working at normal hours. This could assist common unit volumes and will likely be a tailwind as extra of the system returns to a 24/2 and 24/7 format. Lastly, on the subject of unit improvement, the corporate noticed six web new openings within the interval and can see unit progress speed up in 2023. Shortly after quarter-end, IHOP introduced new offers in Saudi Arabia and Qatar, with 9 openings anticipated in these two nations later this decade.

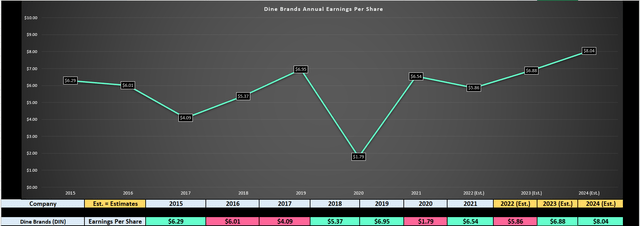

Dine Manufacturers – Earnings Development (YCharts.com, FactSet, Creator’s Chart)

Given the rise in income offset by inflationary pressures, Dine Manufacturers noticed some stress from an earnings standpoint. Throughout Q2, it reported quarterly EPS of $1.65, a 15% decline year-over-year. This has pushed annual EPS estimates down to simply $5.86 for FY2022, which is able to translate to a double-digit decline vs. FY2021 ranges and push earnings again close to FY2018 ranges.

Nonetheless, with an aggressive share buyback program in place (~921,000 shares or 5% of float repurchased in Q2 alone) and unit progress, we should always see a stable restoration subsequent yr. In truth, based mostly on FY2024 annual EPS estimates of $8.04, new highs are on deck. So, whereas annual EPS has struggled since COVID-19, this seems to be to be an aberration within the long-term uptrend. Let us take a look at the inventory’s valuation beneath:

Valuation & Technical Image

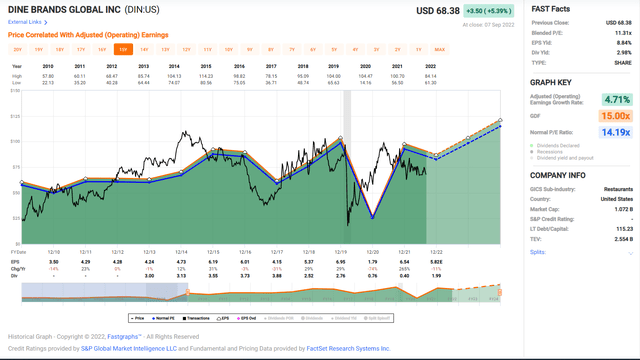

As proven within the beneath chart, Dine Manufacturers has traditionally traded at ~14.2x earnings, and it at present trades at simply 12.0x earnings at a share value of $70.30 (FY2022 annual EPS estimates: $5.86) and 10.2x FY2023 estimates ($6.88). This may counsel a shopping for alternative in a standard surroundings, with DIN buying and selling at a reduction to its historic a number of with a beautiful dividend yield (~3.00%). That mentioned, the {industry} stays challenged even when Dine Manufacturers’ franchisees stay wholesome. Given these headwinds, I feel a extra conservative earnings a number of is 12.1x earnings (15% low cost to 15-year common).

Dine Manufacturers – Historic Earnings A number of (FASTGraphs.com)

Based mostly on FY2023 annual EPS estimates of $6.88 and a extra conservative earnings a number of of 12.1, I see a good worth for Dine Manufacturers of $83.20, translating to a 26% upside on a complete return foundation vs. its 18-month value goal. Nonetheless, these earnings estimates may very well be conservative if Dine Manufacturers continues its aggressive tempo of share buybacks, with ~5% of the float repurchased in Q2 alone. Therefore, it seems to be nearer to a 30% upside to its 18-month goal value in an upside state of affairs, which assumes a conservative a number of for the inventory.

That mentioned, I want a 30% low cost to honest worth to justify coming into new positions, and even with an 18-month goal of $86.30 (dividends paid plus honest worth), the low-risk purchase zone for the inventory strikes as much as $60.40, which might require a ten% dip from present ranges. Clearly, the inventory would not have to say no to this degree, however that is the place I’d view DIN as being in a low-risk purchase zone and worthy of beginning a brand new place.

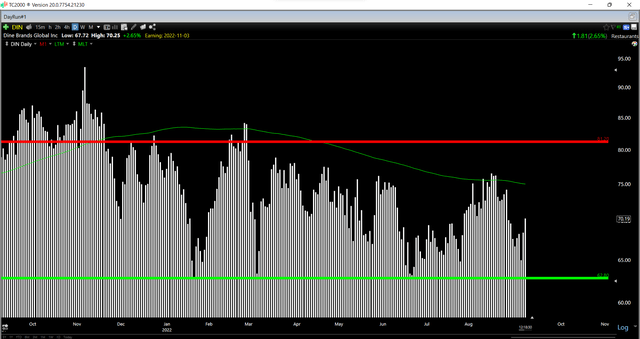

Dine Manufacturers – Each day Chart (TC2000.com)

Notably, this space traces up with the technical image, which exhibits an up to date help degree of $61.00 – $62.80, with incessant shopping for on this space suggesting clear demand from traders and the corporate (buyback program) at these ranges. So, whereas I’m impartial on Dine Manufacturers at $70.30, after a 13% rally since June, I’d count on any pullbacks into this technical help and worth zone to offer shopping for alternatives ($60.40 – $62.80).

Abstract

Dine Manufacturers put collectively a stable Q2 efficiency given the industry-wide headwinds, and we may see a greater Q3 than some had been anticipating, given the fast decline in fuel costs. Nonetheless, even when inflation stays sticky and commodity prices stay elevated, Dine Manufacturers continues to profit from its asset-light mannequin and its worth proposition relative to different informal eating manufacturers. Based mostly on this superior positioning, I’d view pullbacks beneath $62.80 as shopping for alternatives, with essentially the most engaging purchase zone being $60.40 or decrease.

{kind=link}