iantfoto/E+ through Getty Pictures

Introduction

Distribution Options Group (NASDAQ:DSGR) has shortly come up on the radar of extra traders, and rightfully so. Run by CEO Bryan King, who has a prolonged funding administration background, through quite a lot of acquisitions along with their Lawson merger in 2022, the group has added a great quantity of worth to the enterprise through M&A since their merger.

Adjusted for the inventory cut up, the inventory is up ~75% on a 1-year foundation and is now starting to commerce at a stage extra applicable for his or her future prospects. Nonetheless, I feel traders can earn affordable returns-on-capital at at present’s share worth of ~$35. Wanting forward, there are a selection of inner alternatives, DSGR has to develop the enterprise through cross-selling and the associative working leverage. With just a little potential assist from a macro rebound in some verticals, we might see EBITDA develop materially over the approaching few years.

Lawson: Constructive Outlook

Lawson posted This autumn gross sales development of 1% to achieve $110M, all of which was natural. For many who are new, Lawson, which operates by means of totally different manufacturers, is an MRO distributor within the U.S., distributing principally fastening gear, fluid energy objects, auto provides, after which a tail of different varied merchandise their prospects use. These prospects embrace producers, auto restore retailers, authorities/navy after which a tail of others. Particularly, their auto restore enterprise is tied to their Kent Auto enterprise, which distributes merchandise to aftermarket restore/collision retailers.

As they famous on the decision, their Kent Auto enterprise grew as did their authorities/navy enterprise, however this was offset by declines of their core enterprise, which refers to their non-strategic accounts. Full-year development benefited from worth, however that wasn’t attributed to This autumn development, so if something, we are able to in all probability consider it being a small contributor in This autumn.

The auto enterprise really may need taken market share. If we have a look at LKQ Corp. (LKQ), their North America wholesale enterprise posted mid-single-digit natural development in This autumn. Nonetheless, Lawson isn’t solely akin to an LKQ, as LKQ sells extra auto-specific elements whereas Kent Auto is promoting instruments used within the restore operations. To this finish, seeing AutoZone (AZO) report roughly flat home same-store gross sales in Q2 FY24 and Advance Auto Components (AAP) report a low-single-digit comparable retailer lower in This autumn 2023 means that maybe Lawson is certainly outperforming the market at present. On the decision, too, they reported their Kent Auto enterprise signing on new prospects whereas additionally rising pockets share with their current prospects.

For the remainder of their enterprise, which is essentially manufacturing and development after authorities/navy and auto, it’s not unreasonable to suppose that they’re battling macro headwinds. Fastenal (FAST) identified softening manufacturing enterprise, and the manufacturing PMI was sub-50 up till the beginning of 2024. This was one thing Grainger (GWW) known as out in mid-2023, too. If we flip to Wesco (WCC), they’re reporting declines of their development publicity in This autumn 2023.

With that context, let’s zoom out. Attractively, the Lawson enterprise has constantly grown pre-COVID, rising high-single/low-double-digits each year. Whereas sure, there have been acquisitions in each 2018 and 2019, neither of these contributions appear to have been large enough to essentially change that development fee a lot. So, it appears to me like they run a aggressive operation.

There’s some materials ongoing inner change occurring inside Lawson that must be thought of going ahead (and which partly explains at present’s outcomes). As they famous on the Q3 name, they’ve been including accounts reps and inside gross sales reps to their Lawson enterprise all through 2023. Understandably, then, this has resulted in additional publicity driving extra enterprise they convert leads. Now, as identified, their web headcount was down year-over-year because the aforementioned additions mirror extra reorganizing of their reps than additions.

It definitely has resulted in a extra productive common gross sales rep, clearly. And so they’re rolling out a brand new CRM within the first quarter of 2024 to extend effectivity. As Bryan laid out on the decision, they’ve advanced from pondering they should develop the enterprise by including extra ft on the road to now specializing in rising pockets share, basically. Due to this, they’ve decreased their gross sales drive concentrate on these prospects, and have as a substitute shifted to including assist behind outdoors gross sales reps to begin rising gross sales per buyer. Consequently, I’m not shocked then to listen to they’re rising pockets share at their auto accounts – this may be a pure consequence.

This dialog then dovetails into margins, clearly. In This autumn, Lawson posted 11.3% phase EBITDA margins, up from 10.7% within the prior 12 months. Contributing to this was an enchancment of their working leverage, not as a result of items elevated – evidently, they have been according to final 12 months – however as a result of they took prices out – recall headcount being down, web.

Over time, there needs to be some pure margin leverage. As we addressed above, if it’s the case that they’ll be trying to now develop gross sales per buyer extra so than by signing new prospects, that ought to end in materials leverage as you don’t really want so as to add any prices for that incremental sale. Sure, they’ve had so as to add some prices – inside gross sales assist – to assist this development initiative, however that’s principally behind us now, per my understanding. I.e., This autumn prices mirror that assist/value burden.

So, assuming at present’s softness in sure verticals is certainly market associated and never a aggressive difficulty, to the extent then that they’ll begin capturing elevated gross sales per buyer, at present’s low-teens margins ought to develop. They’ve traditionally talked about high-20% incremental EBITDA margins for Lawson, which can be what they confirmed on the decision, and this does not in any respect seem unreasonable.

Lawson earns a mid-50% gross margin, so assuming these prices are variable (of which not all, however most, can be), and that they’ll leverage half of their opex base, which isn’t unreasonable contemplating that you just don’t have so as to add a brand new salesperson or G&A price to promote 10% extra per buyer, I can certainly see then posting mid-20% incremental EBITDA margins.

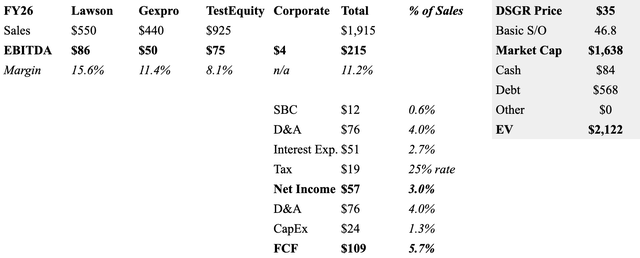

Right now’s $110M in This autumn gross sales are decrease than normalized given the less promoting days in This autumn, so this interprets into one thing like $465M in annual run fee income. Adjusted for that, one thing like a 14% EBITDA margin would make sense. Ought to gross sales develop at ~6% on common, they’d be posting gross sales of ~$550M in FY26. In the event that they earn an incremental 25% margin on that, that will indicate EBITDA of ~$86M.

Gexpro Providers: Temporal Headwinds

Their Gexpro phase is just a little totally different from Lawson. Whereas Lawson is distributing varied C-class MRO elements, Gexpro distributes manufacturing elements – suppose machining gear, bolts, o-rings, and so forth. By way of 2,800 provides, they’re serving round 1,900 totally different prospects – about ¾ of their gross sales are within the U.S. – with lots of their prospects being renewable vitality tied producers – suppose turbine and photo voltaic panel producers – industrial energy, transportation, after which a tail of different verticals. Common Electrical (GE), as an illustration, is certainly one of their key prospects, representing over 20% of gross sales per feedback at their Investor Day, with their high 20 prospects representing 75%.

Gexpro posted a income decline of ~7% to ~$92M, all of which was natural. Gross sales have been down from decrease project-based renewables demand after which their semiconductor vertical. The remainder of their enterprise elevated over 6% with industrial energy and non-project renewables enterprise rising. Relating to the renewables vertical, the dichotomy tends to revolve across the value-added companies – that’s, the decreased undertaking work refers to performing fewer value-added tasks like kitting, as an illustration.

In step with their non-project work, in This autumn, GE’s pointing to increased renewable vitality gross sales from elevated wind turbine gross sales after a comfortable 2022. Now, Gexpro is tied to manufacturing and never what GE delivers (acknowledged as a sale), so it’s not an ideal proxy, but it surely’s a great learn. Notably, although, GE’s anticipating renewable to see development in 2024 per their Investor Day feedback. Though, SP World really has photo voltaic panel demand declining in 2024.

As for his or her semiconductor vertical, the place revenues have been down 50% for the 12 months, I’m not likely seeing this within the public knowledge. I’m seeing third-party stories that semiconductor gross sales have been down throughout 2023, however that the second half of 2023 reported optimistic comps. Certainly, TSM reported gross sales down 1.5% in This autumn and NXP reported low-single-digit gross sales development in This autumn. So, perhaps they’re dropping some share, perhaps not – it’s laborious to inform.

They known as out destocking usually, so which may be contributing to the outsized adjustments. The historical past of the enterprise, nonetheless, would recommend share losses are in all probability unlikely. Not solely do they supply end-to-end options to multinational firms like GE, which implicitly validate their competitiveness, however their buyer retention is 98% (per feedback at their Investor Day). Additionally, at their Investor Day, they supplied an anecdotal instance of a buyer of theirs requesting increasingly more packages with Gexpro, which I wouldn’t discover according to a structural ROI difficulty.

Additionally they talked concerning the profit from cross-selling into Resolux’s and Frontier’s prospects, each acquired in the beginning of 2022. Resolux had 7 OEM prospects that Gexpro didn’t have (3 on the time) so by combining them and including Frontier, this (1) expanded their product breadth and (2) added new prospects to cross-sell into. And so they took benefit of them – their win fee for product packages almost tripled due to this all-in-one worth proposition (once more, Investor Day knowledge). So, it’s laborious to suppose they’re dropping market share – they need to as a substitute be taking market share at present.

Margin-wise, they posted 9.5% phase EBITDA margins, down from 10.8% within the prior 12 months. They known as out pricing contributing to Gexpro’s development in mid-2023, however nothing since then, so it’s unlikely there was any materials headwind or tailwind right here. We all know, nonetheless, that working leverage was a headwind with their unit volumes down – outdoors of product and transportations prices, there’s a great quantity of labor utilization, each by way of gross sales reps and by way of technicians offering companies. After which combine was a headwind too as their tech/semiconductor vertical, which carries increased margins as famous on the decision, declined quicker.

Wanting forward, there’s an analogous margin development alternative right here. We are able to see the leverage inherent within the enterprise – they posted 11.3% margins on $104M in gross sales in Q3, as an illustration – however think about the aforementioned feedback about providing bigger packages to prospects – to the extent they’re profitable extra of those than earlier than – i.e., rising gross sales per buyer – that needs to be capturing excessive incremental margins. And never solely that, however combine ought to enhance per what I feel are extra macro points than aggressive inside their semiconductor vertical.

So, at present’s $92M in gross sales interprets into round $380M yearly adjusted for This autumn seasonality and ~10% EBITDA margins. Possibly they see demand worsen just a little additional in 2024 – they’ve seen a cloth enchancment of their renewables book-to-bill fee – however these are all GDP+ end-markets by way of manufacturing, so post-trough development needs to be nearer to mid-single-digits. Then there needs to be some uplift from cross-selling. Operating related math as earlier, ought to they develop at 5% over the subsequent 3 years, that’s FY26 gross sales of ~$440M. Gexpro earns slightly below 30% gross margins, so between pure labor utilization and improved combine, maybe 20% incremental EBITDA margins are OK – below this situation, they’d be posting gross sales/EBITDA of ~$440M/~$50M.

Over time then, if it’s simply macro associated, they need to develop because the end-markets develop – these are all GDP+ growers. They may soften within the coming 12 months (2024) and that could be a near-term threat per the aforementioned GE outlook, however administration, nonetheless, is not actually pointing that proper now, so it is not likely clear there’s imminent softening.

TestEquity: Close to-Time period Questions

TestEquity is just like the opposite 2 segments in that they too function a distributor, however as one would infer from the identify, they get extra into check and measurement gear and associated provides (amongst different ancillary merchandise). They really have their very own line of check chambers manufactured in-house, which they’ll each promote and hire. They promote to quite a lot of manufacturing operations – aero, protection, semiconductors, electronics manufacturing, and so forth. – with 85% of gross sales generated within the U.S. Certainly, there’s overlap with producers that Gexpro sells to. Aero & protection and electronics manufacturing characterize about 60% of gross sales.

This autumn income elevated over 80% to ~$191M, which included ~$97M of Hisco gross sales – excluding that, and natural gross sales have been down ~11%. Unpacking this, there have been definitely some market headwinds. First, they reported some destocking occurring at their prospects as famous earlier – one thing noticed extra broadly – in order that’s exaggerating the comp.

However second, right here too, there have been in all probability some macro headwinds. Recall that that is higher-cost gear – these are large, cumbersome machines in some circumstances; it’s not solely MRO sort of product that they promote inside Lawson, though there’s some. As such, there’s a level of discretionary-ness in right here such that if demand is weaker, they’ll defer purchases a la a shopper deferring a brand new automotive buy when budgets tighten. To this finish, this knowledge speaks to world traits whereas most of their prospects are U.S. primarily based, but it surely’s not shocking to see that versus 2022, electronics manufacturing is certainly softer, so you’ll be able to think about some prospects are deferring spend.

Now, per our work on AstroNova (ALOT), the aero & protection aspect of the enterprise is seeing increased demand ranges with whole industrial airplane manufacturing being increased, however that’s not what they’re reporting – they’re reporting softness right here from gear deferrals. I suppose there may very well be some deferrals from elevated uncertainty usually, however they admit on the decision to dropping market share by not taking down costs to ranges supplied by their opponents who have been liquidating extra stock. They didn’t level out a particular product line or vertical behind this, however both manner, it’s contributing to their gross sales decline.

Additionally, my sense is that it’s certainly a temporal downside. Sadly, it’s a bit laborious to get any learn on market share, structurally talking, as a result of there aren’t any good comps. However we are able to see that after posting gross sales development in 2021, they posted natural development of ~12% in 2022, in order that wouldn’t be according to share loss. At their investor day too, they talked about having varied prospects pull them into different areas, one thing we’d unlikely see in the event that they have been dropping share due to an inferior ROI.

Much like the opposite segments, they need to’ve been benefiting from cross-selling following the acquisitions accomplished in 2022. Much like Gexpro, there’s not a lot alternative to cross-sell TestEquity’s vary of merchandise into their different segments – perhaps just a little overlap with Gexpro – however there’s some alternative intra-segment. Certainly, that is one thing they’ve known as out as occurring.

Moreover, now that they’ve acquired Hisco (mid-2023), which offers fabrication companies, specialty supplies, repackaging options, and so forth. to producers, they’ve extra alternative. Hisco successfully has stuffed out their product lineup for these prospects, significantly the manufacturing part, and even offers them extra chemical substances options that they’ll cross-sell into a few of their different OEM prospects who cope with chemical substances.

And this’ll enhance margins too. They posted 6.2% phase EBITDA margins, down from 9.9% within the prior 12 months. It definitely may very well be that they introduced their costs down just a little to be extra aggressive, however evidently, they didn’t carry them down sufficient, therefore the share loss, so it is laborious to deduce there was an excessive amount of influence right here. And there may need been a mixture headwind too as they known as out fewer capital tasks particularly and added Hisco (low-7% margins).

The majority of the degradation, nonetheless, was from working deleverage, which clearly resulted in much less labor utilization through gross sales reps, service reps, again workplace workers, and warehousing mounted prices. Concurrently although, going ahead, they’re beginning to rationalize the 2 companies which goes to end in duplicate value elimination. They anticipate to eradicate ~$10M in annual prices, which solely started in This autumn.

All in all, at present’s $191M quantities to ~$800M yearly when adjusted for This autumn seasonality. If it’s true that at present’s points are macro-driven and never a aggressive difficulty, contemplating the GDP+ nature of those verticals plus cross-selling alternatives, mid-single-digit gross sales development is achievable right here too. That may take that $800M to $925M by FY26. With a low-teens incremental EBITDA margin, value eliminations, and blend enhancements, I estimate they may very well be incomes ~$75M in EBITDA by FY26.

Valuation: Compelling

We haven’t talked about capital allocation, however that’s a brilliant spot. None of that is too shocking both – the enterprise is run by a group with an in depth background within the funding administration enterprise, in order that they know the way to consider valuations. E.g., They paid simply over 7x trailing EBITDA for his or her 2022 cohort of acquisitions, which per my math, works out to one thing like a 10-12x NOPAT a number of (after SBC, tax, and capex) given the comparatively low capex depth. Clearly, that is slightly enticing contemplating the post-acquisition synergies we anticipate them to understand too, thus resulting in low-teens+ IRR.

They only paid $267M for Hisco in mid-2023, which additionally got here at a lovely a number of. On a trailing foundation, they paid round 9x EBITDA, which quantities to one thing like 16x NOPAT by my math. And right here once more, they’re going to choose up quite a lot of synergies, that are going to carry this a number of down materially.

There’s at all times the danger that an acquisition pans out poorly, however I feel this threat is mute over time given a big sufficient pattern of M&A. Assuming they’ll preserve making acquisitions then going ahead, they deserve a premium FCF a number of. What would constrain them right here isn’t the variety of targets, however these are keen to promote at enticing valuations.

The largest threat, I feel, to their valuation is simply timing with respect to macro-related headwinds. I.e., Ought to current persist longer-than-expected, that’ll clearly carry down their intrinsic worth. There’s additionally the likelihood although that their current TestEquity aggressive depth is extra structural slightly temporal. And there is additionally the execution threat – it is not a assure that their inner salesforce or cross-selling initiatives are profitable. Each of those are most unlikely, however dangers nonetheless that one needs to be aware of.

Added all up, per what I laid out earlier, here is what I get:

Inner Estimates

Web then, they’re at the moment buying and selling at ~15x my estimate of FY26 FCF.

Find out how to worth this? Nicely, if we assume that every one money goes to shareholders through dividends and repurchases, I’d say one thing like a 20x FCF a number of is justifiable – that will indicate long-term earnings development of mid-single-digit which is seemingly achievable with their working leverage.

Nonetheless, DSGR breaks my typical valuation technique of valuing companies on natural development as a result of they’re going to maintain pursuing M&A. To this finish, although, if they’ll preserve redeploying a lot of the FCF into M&A on the returns they’ve been attaining over time, a a number of increased than 20x FCF is warranted. E.g., in the event that they submit a median of $70M in money yearly or $210M over 3 years, and redeploy $200M in M&A at mid-teens IRR, they might definitely add one thing like $15-20M in FCF yearly rising alongside the enterprise. $17.5M at a 20x FCF a number of would quantity to incremental $350M in worth by FY26, not $210M.

So, the way in which I’m enthusiastic about this one is to take what I feel they’ll organically earn in FY26 – ~$109M – and ascribing a premium a number of that I feel displays their elementary natural outlook plus possible M&A upside over time. To this finish, then, a a number of between 20-25x – say, 22.5x – appears affordable. 22.5x $109M will get me to a market cap of ~$2.45B – add within the money generated within the interim of ~$200M thereabouts, and low cost that sum again 3 durations will get me to a good worth at present of ~$42/share.

Conclusion

Put collectively, DSGR presents a compelling alternative at present at their present costs. As soon as we get previous among the macro headwinds, and so they begin layering on inner gross sales rep development and cross-selling, they need to begin to see extra materials development. Coupled with their inner alternatives to develop margins and clever capital allocation deserving of a premium a number of, it’s conceivable that DSGR finally ends up a materially greater enterprise than at present and price much more.

{kind=link}