baona/iStock by way of Getty Photographs

Animal spirits have come off the boil currently, however these are nonetheless early days for deciding if risk-on sentiment for equities has hit a wall or is in a holding sample that permits markets to consolidate the features of late. The evaluation arises from a set of ETFs to gauge the chance urge for food, based mostly on costs via yesterday’s shut (Apr. 24).

A key issue that would create bother for shares is the return of reflation pressures. Thus far, equities have been comparatively resilient. However additional deterioration in bond costs will possible create stronger headwinds.

This overview updates a profile from earlier this month, which discovered that the risk-on bias for equities was intact. Greater than two weeks later, the signaling hasn’t modified a lot, which is to say that the current weak spot in markets has been comparatively gentle to date.

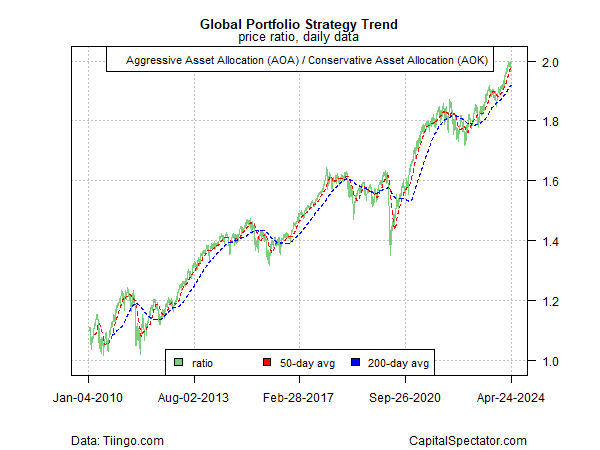

Let’s begin with a big-picture profile based mostly on an aggressive international asset allocation portfolio (AOA) vs. its conservative counterpart (AOK). For the second, this development continues to defy gravity and stays close to a document excessive—an indication that threat urge for food stays sturdy.

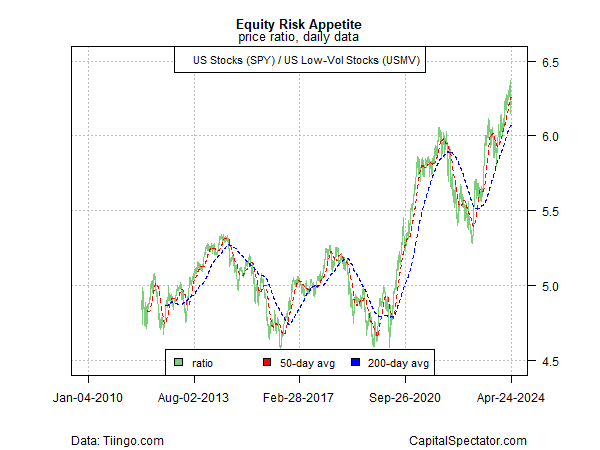

For US shares, a pullback in threat urge for food is a little more conspicuous currently, however the risk-on development nonetheless appears to be like strong by way of a comparability of US equities (SPY) vs. a low-volatility subset of shares (USMV).

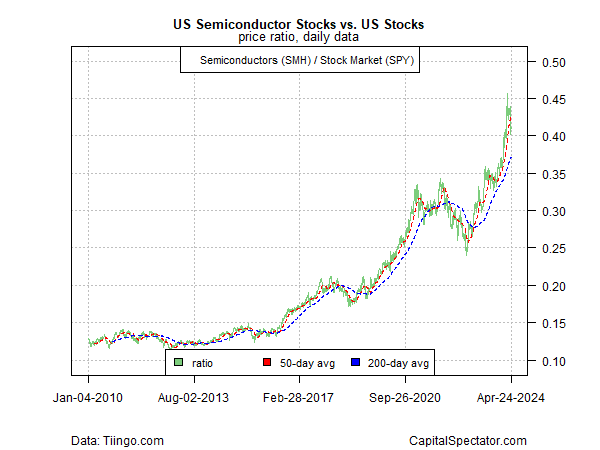

A key bellwether for monitoring the US threat urge for food can also be holding up reasonably effectively throughout the current bout of promoting, based mostly on the ratio of semiconductor shares (SMH) (a business-cycle proxy) vs. a broad measure of US equities (SPY).

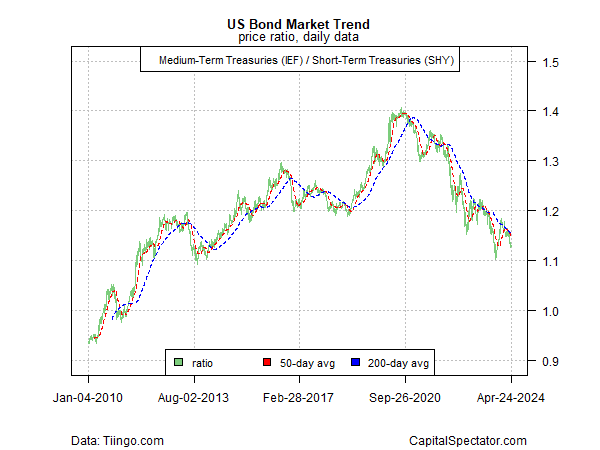

The bond market, nevertheless, stays a bearish outlier within the present setting, based mostly on medium-term authorities bonds (IEF) relative to their shorter-term counterparts (SHY). The current slide on this ratio means that US fastened revenue stays firmly in a risk-off situation.

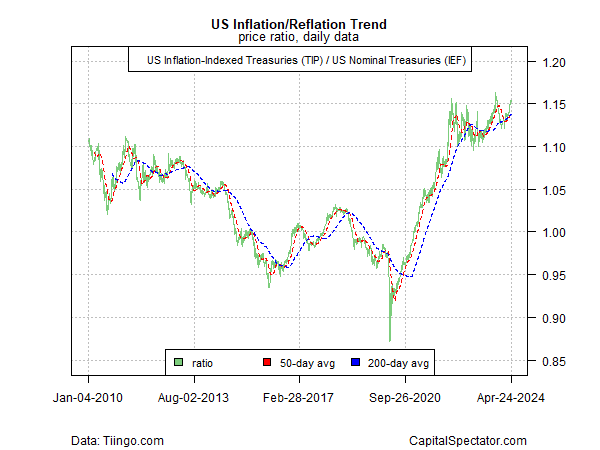

A vital part of the headwind for bonds is the trace that reflationary threat could also be brewing anew, based mostly on the ratio of inflation-indexed Treasuries (TIP) vs. medium-term authorities bonds (IEF). This indicator has rebounded just lately, which means that the bond market will proceed to wrestle.

Will the fallout for bonds spill over into the equities market? For the second, there’s been minimal collateral harm for shares. But when the bond market continues to deteriorate, it’s exhausting to think about that shares received’t ultimately pay a worth.

Authentic Submit

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.

{kind=link}