Scott Olson

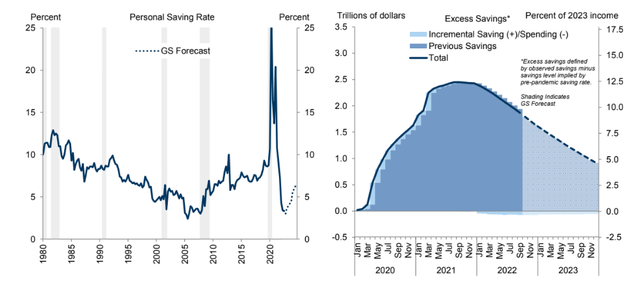

All eyes shall be on the patron in 2023. With sturdy retail gross sales numbers in current months, however dwindling extra financial savings from the pandemic, the U.S. Private Saving Charge has collapsed to decade-plus lows. The hope is {that a} delicate touchdown within the labor market will assist cushion the blow of potential month-to-month job losses subsequent 12 months – small web retractions within the NFP numbers can be acceptable in comparison with steep labor market declines seen in previous recessions. Because it stands, shoppers hold spending, however there are indicators of buying and selling all the way down to lower-cost retailers.

Greenback Tree (NASDAQ:DLTR) reported robust outcomes on Tuesday, however tepid steering and rising prices are large dangers. Is the inventory a purchase now? Let’s browse the aisles.

Client In Focus: Saving Charge Down, Extra Financial savings Falling Arduous

Goldman Sachs Funding Analysis

Based on Financial institution of America World Analysis, Greenback Tree is likely one of the largest greenback retailer chains in the USA, with over $25 billion in revenues in 2020. The corporate operates 15,685 shops in 48 US states and 5 provinces in Canada beneath the Greenback Tree, Household Greenback, and Greenback Tree Canada banners, and shops carry an assortment of consumables, basic merchandise, and seasonal merchandise.

The Virginia-based $6.9 billion market cap Basic Merchandise Shops trade firm inside the Client Discretionary sector trades at a excessive 22.0 trailing 12-month GAAP price-to-earnings ratio and doesn’t pay a dividend, in response to The Wall Avenue Journal.

The agency reported beats on the highest and backside strains on Tuesday morning, however shares traded sharply decrease as price pressures stick with the well-known greenback(ish) retailer. Weak earnings steering was additionally a bearish wrongdoer.

Greenback Tree has important near-term headwinds from rising labor prices to larger delivery charges to visitors restoration headwinds. Inflation and a weakening client usually are not constructive traits, regardless of the pure and apparent trade-down impact amongst middle-income households.

Additional draw back dangers embrace rising competitors from different greenback shops and low cost retailers – notably within the dog-eat-dog meals retail space. SNAP profit cuts is a priority, too. Upside potential, although, stems from higher same-store gross sales development, improved margins resulting from class spending shifts, and even a loosening of tariffs.

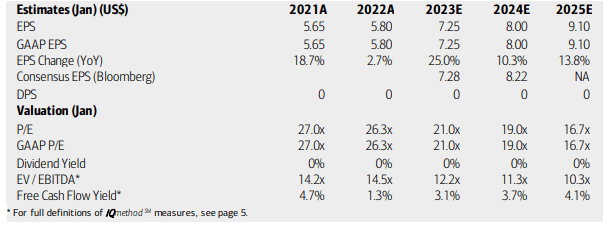

On valuation, analysts at BofA see earnings having grown under the speed of inflation in 2022, however then a pointy acceleration is seen subsequent 12 months together with sturdy per share revenue development in 2024 and 2025. The Bloomberg consensus forecast is much more sanguine on EPS within the subsequent two years.

Nonetheless, each the working and GAAP P/Es stay at a premium to the market, although according to the richly valued Client Discretionary sector. DLTR’s EV/EBITDA can be excessive, however the agency is free money circulation constructive. The agency’s ahead PEG ratio is 1.2, considerably under its 5-year common of two.0. General, the valuation is sweet contemplating its development prospects.

Greenback Tree: Earnings, Valuation, Free Money Movement Forecasts

BofA World Analysis

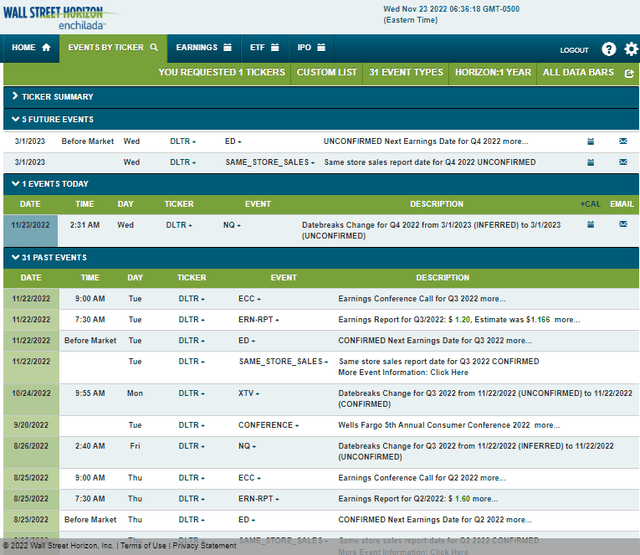

Trying forward, company occasion information supplied by Wall Avenue Horizon present an unconfirmed This autumn 2022 earnings date of Wednesday, March 1 BMO. The calendar is gentle till that occasion, nonetheless.

Company Occasion Calendar

Wall Avenue Horizon

The Technical Take

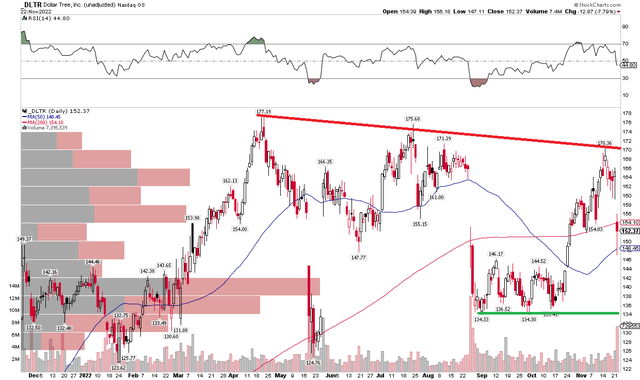

DLTR has a messy, rangebound chart within the final 12 months. However that is not essentially a foul factor on this weak 12 months for the broad market and, particularly, the Client Discretionary sector.

I see resistance at a downtrend line off the April excessive – shares met sellers there in July and once more simply in November earlier than its Q3 earnings outcomes hit the tape. There’s help, although, at $134 (and the longer-term chart reveals a powerful zone round $120 that ought to maintain up).

General, I want to see the inventory breakout above the $170 stage and make new all-time highs above $177 to assist solidify a brand new bullish transfer. Till then, the inventory is solely meandering in a broad vary with volatility. I would look to purchase the dip on a transfer to $140 – discover the excessive volume-by-price that begins there. A sell-stop order under $134 would make sense for a positive threat/reward. Earnings needs to be taken on an method of the mid-$160s.

DLTR: Shares Consolidating, However Nonetheless Outperforming The Broad Market

StockCharts.com

The Backside Line

I like DLTR valuation right here given the expansion outlook, however main macro dangers pose a risk to earnings subsequent 12 months. It may be too quickly to purchase the inventory, however shopping for on weak spot over the subsequent six months may show to be a great play. The PEG ratio is engaging. The chart, although, is solely in consolidation mode. I would watch for a breakout earlier than getting lengthy.

{kind=link}