felixmizioznikov

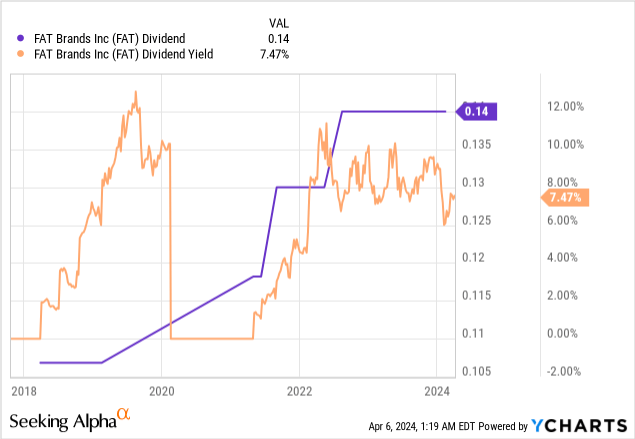

FAT Manufacturers (NASDAQ:FAT) has at all times provided a novel investing paradigm. It is a loss-making $126 million market micro-cap firm providing a big dividend yield towards a rising specter of debt and a liquidity place beset by consecutive quarters of money burn and a rising debt burden. FAT final declared a quarterly money dividend of $0.14 per share, left unchanged sequentially and $0.56 per share annualized for a 7.47% dividend yield. FAT owns 18 quick informal and informal eating restaurant manufacturers together with Twin Peaks, Smokey Bones, Fatburger, and Johnny Rockets. The corporate is in intense development mode with its opening of 125 new shops in 2023 set to be adopted by an extra 150 models in 2024 towards a improvement pipeline of 1,200 models.

I used to be bearish on the commons and the Sequence B preferreds once I final coated the ticker. Whereas each are up since then, the underlying bearish thesis has remained sticky. FAT generated fiscal 2023 fourth-quarter income of $158.6 million, up a outstanding 52.8% over its year-ago comp and beating consensus estimates by $8.2 million. Whole income for 2023 at $480.5 million was up 18% year-over-year with FAT now buying and selling for 0.26x occasions its 2023 gross sales. Nonetheless, the corporate’s long-term debt burden stays a fabric barrier to worth creation right here, ending the fourth quarter at $1.1 billion, up $152 million from the year-ago comp. Additional, there’s one other $42.6 million in present debt each set towards money and money equivalents together with restricted money of $76.3 million on the finish of the fourth quarter. There may be one other $15.58 million in non-current restricted money.

Stockholders’ Deficit, Dividend Protection, And Money Burn

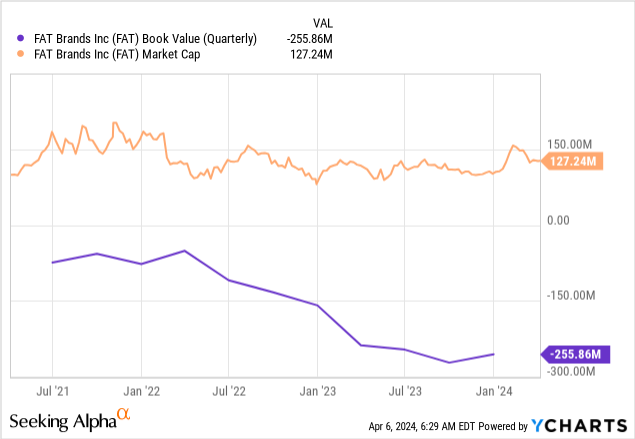

FAT’s whole stockholders’ deficit stood at $255.86 million on the finish of the fourth quarter, a deterioration from a deficit of $159.18 million a yr in the past. This deficit is being pushed by continued losses as inflation, larger wage prices, and better curiosity expense on debt get aggregated. FAT spent a fabric $33.3 million throughout the quarter on paying curiosity on its debt with adjusted EBITDA at $27 million throughout the fourth quarter, up from $19.6 million a yr in the past. Web earnings was unfavourable at $26.2 million throughout the fourth quarter. This determine was an enchancment from a lack of $70.8 million within the year-ago interval. It means the corporate’s $2.34 million per quarter dividend has no protection, rendering it completely precarious and its continued payout an anomaly towards its money burn and the sustained development of its long-term debt.

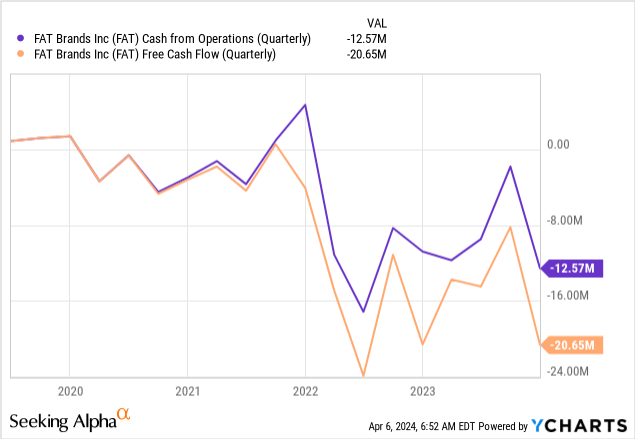

Money from operations was unfavourable at $12.57 million throughout the fourth quarter, up from a burn of $10.8 million a yr in the past with FAT’s whole money burn throughout 2023 at $35.6 million. This burn profile has not improved towards the ramp-up in working models for the reason that pandemic. The Fed’s combat with inflation has made FAT’s debt costlier at an important stage of its development. Whereas this may finally be parred again this yr, probably on the June FOMC assembly, FAT’s underlying profitability is ready to stay unfavourable for some time. The corporate’s present liquidity stability supplies sufficient runway for greater than a yr of operations however the continued use of debt to develop this runway presents a considerable danger for FAT.

The Twin Peaks IPO Liquidity Occasion

FAT is seeking to offload its fast-growing model Twin Peaks by an IPO anticipated within the second half of 2024, with administration stating throughout their fourth-quarter earnings name that they hope it’s a 2024 third-quarter occasion. There have been 14 new Twin Peaks lodges opened in 2023 to deliver its whole on the fourth quarter finish to 109 lodges. FAT solely acquired the model in 2021 and has since expanded models by 33%. The corporate’s development pipeline contains an extra enlargement of 113 lodges. Twin Peaks is FAT’s strongest model with an AUV at roughly $6 million. The momentum behind the model led FAT to accumulate Smokey Bones in October final yr to transform roughly 61 places into Twin Peaks lodges. The uncertainty would be the IPO worth for Twin Peaks with the model essentially included inside the $126 million market cap zeitgeist for FAT.

There may be roughly $272 million of Twin Peaks debt held on FAT’s stability sheet that could possibly be shed within the occasion of the unit IPO, however this quantities to roughly 25% of its whole debt burden. The post-IPO entity would wish to boost tons of of hundreds of thousands in further fairness on prime of the debt for the deal to make a fabric distinction to the trajectory of FAT’s at present torrid funding profile. Therefore, each the widespread shares and the preferreds stay a promote with continued quarters of money burn set to see FAT’s liquidity dip additional and debt balloon.

{kind=link}