Jeff T. Inexperienced/Getty Photos Information

Perma-Repair Environmental Providers (NASDAQ:PESI) is an organization specializing in nuclear and blended waste administration remedy and providers. Whereas the corporate was stymied for 2 years by the Covid-19 pandemic, the long run has by no means seemed brighter. As Covid-19 has moved from pandemic to endemic, we’re seeing a “return to regular” in most of society, together with authorities companies which were a number of the slowest to make this transition.

However for PESI, it seems the “return to regular” shall be disproportionately bullish. I’ll spotlight beneath a number of key indications supplied by administration on its latest 4Q21 convention name, which align with publicly accessible knowledge on these issues. For many who want for a short background on the corporate, I like to recommend my earlier introductory article on the corporate. For many who may desire much less element than this text, or to listen to my thesis by way of audio, you may tune in to my latest 10-Minute Podcast with Breakout Traders.

In brief, I consider PESI stays on observe to attain the monetary targets I outlined in that prior article. If PESI is ready to try this, I consider the corporate’s shares may probably triple from the present $5.50/share vary inside a comparatively brief interval (i.e. the following 12-18 months).

PESI’s Latest Previous

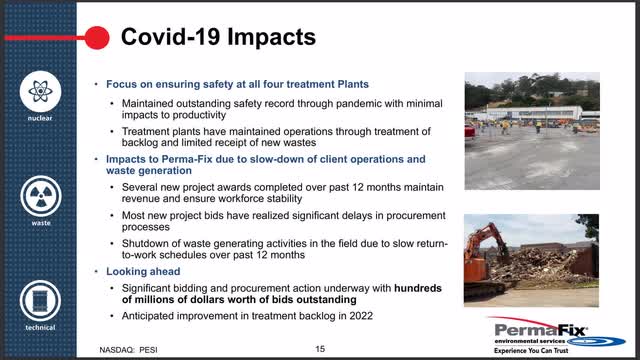

As famous, Covid-19 issues considerably and negatively impacted PESI over the previous two years. As a result of PESI’s work depends on waste being created, the corporate was hit hardest by the pandemic in 2021. All through 2020, the corporate was in a position to work by means of prior backlog of waste, however since not as a lot waste was created in 2020 as throughout a standard 12 months, enterprise momentum slowed in 2021. Luckily for the corporate and its buyers, the worst of this case appears to be within the rearview mirror. In reality, primarily based upon a number of knowledge factors I’ll focus on on this article, I consider PESI is not going to solely “return to regular,” however will far exceed its pre-2020 operational and monetary efficiency ranges.

Return to Regular – And Past

On the latest 4Q21 name I linked within the introduction, CEO Mark Duff famous he was “extremely inspired” by the pent-up demand PESI is seeing in its Therapy Phase. Whereas noting some initiatives have been delayed in 4Q21, he commented “they’ve all been mobilized now to full operation in direction of the tip of this (i.e. 1Q22) quarter.”

PESI Investor Presentation

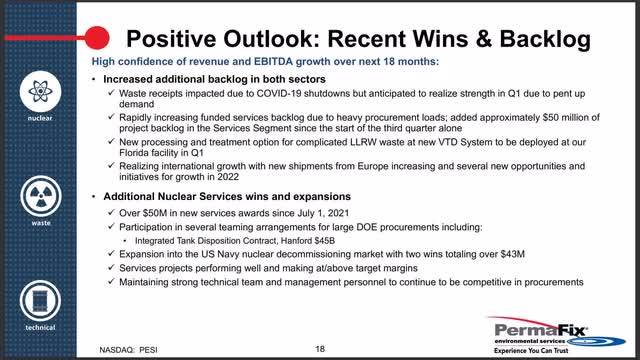

The CEO continued by sharing some key metrics on bidding exercise, which he indicated has a direct influence on the corporate’s income. In accordance with Duff, the corporate was bidding on round 15 contracts per thirty days in December 2021. Nonetheless, in March 2022, the corporate bid on 28 initiatives—nearly 100% extra than simply three months in the past! Previous to this huge improve, Duff stated 20 bids a month was “fairly good,” whereas additionally noting that Q1, and March specifically, are “all the time our slowest” by way of waste receipts and gross sales. So, given this vital uptick throughout what is often the slowest quarter, Duff expressed he’s “very inspired” by the progress on the Therapy aspect of the enterprise.

The Providers Phase can also be seeing abnormally excessive demand, with venture backlog standing at roughly $66M. In response to a query I requested Duff on the 4Q name, he clarified that backlog is outlined for the Providers Phase as work that’s (1) underneath contract and for (2) funded contracts. In different phrases, as he famous, backlog is just for initiatives with which the corporate has “a really excessive diploma of confidence.” Additional, Duff famous that income is often acknowledged from backlog inside 6-18 months of the contract being awarded. He concluded by stating “the vast majority of that [backlog] shall be [recognized as revenue] this 12 months. There could also be $5-10M that might stumble upon the following 12 months.”

To place this backlog of $66M in perspective, in FY21, PESI acknowledged $39.2M of Providers Phase income. Deducting out even $10M from the backlog and transferring it into 2023 income, we nonetheless see that the backlog alone represents 43% topline development! Any new enterprise gained in the course of the 12 months will solely make that quantity larger.

PESI Investor Presentation

The ultimate macro tailwind value mentioning right here is the approval of the 2022 federal price range. That price range allocates $900M in an incremental funding improve over final 12 months throughout the Division of Vitality’s (DOE) Workplace of Environmental Administration. Duff “consider[s] this extra funding will assist elevated waste remedy and different initiatives by means of 2022.”

Associated to that, Duff highlighted that PESI has been actively bidding on numerous new administration & working (M&O) sort nuclear providers initiatives throughout the DOE that can possible be introduced later this 12 months. He famous: “A few of these initiatives are fairly appreciable in dimension and [would] characterize a considerable improve in sustainable income for a few years.” So on high of an already anticipated 40%+ improve in Providers section income from backlog alone, PESI has yet one more appreciable development alternative with these attainable M&O nuclear providers initiatives.

Whereas many of the United States is “returning to regular,” it seems PESI shall be exceeding its personal pre-pandemic “regular.” I’ll focus on in additional element a number of the particular initiatives and areas which are prone to profit PESI and its shareholders within the close to future.

TBI – Hanford Web site

By far probably the most profitable attainable future venture that I hope to see in PESI’s near-future pertains to the Check Mattress Initiative (“TBI”) on the Hanford nuclear website. I wrote about a number of the background particulars of this venture in my earlier article. In brief, if PESI’s bidding conglomerate wins the enterprise of the DOE on the Hanford website, PESI may greater than double its pre-Covid annual income on that venture alone.

In accordance with a report from the Nationwide Academy of Sciences, PESI’s grouting and elimination methodology of coping with the waste at Hanford would save taxpayers $95B (sure, billion, not million!) over the multi-decade lifetime of the venture. Due to this, and due to the environmental advantages of PESI’s course of, sources inform me that the Senators from Washington state (the place Hanford is situated) and the Consultant from that district are supportive of PESI’s course of to assist clear up the Hanford website. As well as, there are native, influential enterprise leaders publicly and vocally supporting PESI’s course of due to the environmental and value financial savings.

PESI Investor Presentation

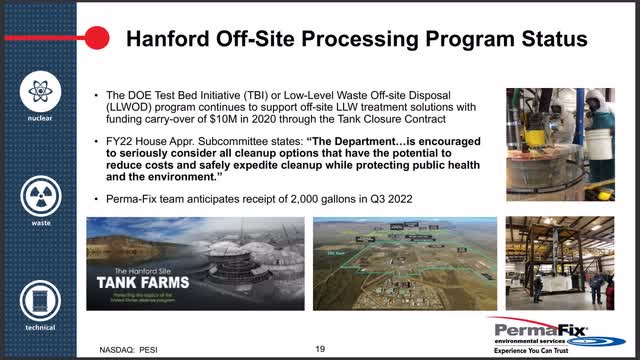

On the 4Q name, CEO Duff referred to 2 quotes from a March 25 Weapons Complicated Monitor weekly publication: “In public feedback, the DOE’s supervisor for the Hanford website just lately acknowledged, and I quote, ‘I will surely prefer to execute the Check Mattress Initiative as early as we feasibly can.’ He went on to state that funds at the moment are accessible for each set up and elimination of the wanted gear.” Duff continued: “In related feedback, [a regulator from] the Nuclear Waste Administration for the Washington State Division of Ecology acknowledged and, once more, I quote, ‘We’ve TBI as a precedence. As soon as an utility is distributed our approach, if now we have to tug assets from one other program, we are going to with a purpose to course of that utility.’ As you may see, TBI has definitely change into a precedence at each the federal and the state ranges in Washington.”

As additional proof of this venture turning into a precedence, Duff cited the just lately enacted federal spending invoice that features a further $7 million particularly allotted for the Check Mattress Initiative in 2022. In that vein, he commented that the second section of PESI’s demonstration will embrace extraction cargo and transportation of two,000 gallons of tank waste to PESI’s facility in Richmond, Washington. He stated DOE officers have acknowledged the cargo of this waste to PESI’s facility ought to happen by late summer season 2022. Following that, PESI expects the DOE to award the Hanford website extra completely in Q422. In accordance with Duff: “They appear to be on observe for that. That they had orals earlier this month, they usually’re on their approach. So hopefully, they follow that schedule. That shall be necessary to us and all the opposite bidders as properly.”

To be clear, an award for the Hanford website cleanup could be profitable for PESI and its shareholders. However even when PESI by no means earns one other dime from the Hanford website, their present core enterprise is predicted to develop considerably, primarily based on a number of different initiatives I’ll now spotlight beneath.

US Navy De-Commissioning

One other thrilling development alternative for PESI outcomes from the de-commissioning of submarines by the U.S. Navy. I detailed this in my prior article. However since that point, it seems the Navy is planning to de-commission two further ships within the subsequent 12 months, a reality highlighted by investor, Ross Taylor, within the 4Q21 convention name Q&A. In response to Taylor’s probing, CEO Duff famous there are 9 ships coming, and one or two shall be nuclear subs, on which PESI’s workforce will work.

Duff emphasised: “There’s not a whole lot of different industrial contractors on the bottom [that can do what we do]. So we’re fairly assured we’ll have shot on the work.” Nonetheless, Duff cautioned: “It should be troublesome to foretell [the amount of work] within the subsequent two quarters. However definitely, by the tip of Q2, we’ll have a greater schedule of what is arising.”

To offer a way of the materiality of this work to PESI, I need to draw consideration to Duff’s following feedback: “[The first ship] is within the $40 million to $50 million vary [and] might be one of many smallest jobs. And I feel there’s a whole lot of ships in between, between $50 million and $200 million every. All of it will depend on the extent of contamination.” As you may see, even “one of many smallest jobs” is extremely materials to PESI, representing properly over 50% of PESI’s FY21 income.

Worldwide

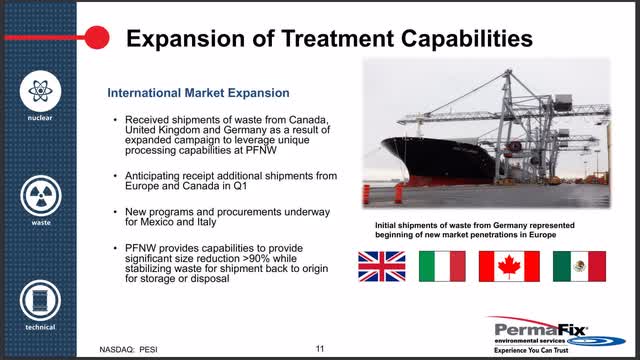

Yet one more development alternative for PESI is within the worldwide market, most particularly in Europe. To this finish, in early March, PESI introduced a three way partnership with Westinghouse UK concentrating on waste remedy in Europe. Whereas PESI is getting this operation up and operating, they are going to be transport and treating waste from Europe at their American services.

In response to my questions on European alternatives, CEO Duff talked about on the This autumn name that PESI is receiving a second cargo from Germany proper now. He additional famous the corporate is receiving two different waste streams from two totally different nations in Europe (he was unwilling to supply additional particulars on the particular nations concerned).

PESI Investor Presentation

General, Duff commented they’re 10-12 “very particular waste streams” that he believes they will deal with “within the subsequent 18 months.” He stated the worth of these is between $500,000 and $20M per venture. And, in fact, further alternatives will open up as soon as the three way partnership facility opens with Westinghouse UK (possible in 18-24 months).

MATOC Alternatives

The ultimate development alternative value noting for PESI presently pertains to multi-award job order contracts (“MATOCs”). As detailed in my earlier article, PESI has been named on a number of of a lot of these contracts for a number of totally different initiatives, with some budgeted to spend as much as $95M. These MATOCs permit a small, choose group of firms to bid on job orders with restricted competitors. In brief, as soon as an organization has been named on a MATOC, it’s faster and simpler for them to be awarded an order that falls underneath the MATOC’s purview.

In accordance with Duff, PESI anticipates awards from these contracts to start in 2Q22 or 3Q22. These MATOCs present but additional upside for PESI.

Dangers

By far the largest threat to PESI pertains to the highly-regulated and delicate atmosphere wherein they work. If PESI have been to make a serious environmental mistake, the corporate might be materially fined. General, the corporate maintains a robust document of security and safety, however that is all the time a threat in PESI’s sort of enterprise.

The second threat value mentioning is that any resurgence of the Covid-19 virus may delay PESI’s progress. Whereas this threat appears comparatively low proper now, I don’t consider we will fully low cost the chance till we get by means of what is often known as “the flu season” with out Covid turning into an enormous downside.

The third threat value noting is that PESI operates underneath a number of fixed-rate construction contracts. Errors made in calculating their charges versus what it really finally ends up costing PESI may materially alter PESI’s margins and, thus, backside line.

Valuation

In my introductory article to PESI (linked within the introduction) I supplied an in depth mannequin for the corporate for 2022-2024. My valuation for the corporate has not materially modified, so I’ll merely reiterate a few of my key assumptions right here, in addition to my income and EPS estimates from my mannequin. If you wish to see all the small print that helped me arrive at these numbers, I like to recommend you refer again to that article.

2022 Assumptions & Estimates

I consider PESI will return to pre-Covid income and margin numbers on its core enterprise. Along with that, I estimate the corporate will add round $10M in new worldwide work; $20M for MATOCs; and $20M from submarines. The Hanford website, I predict, shall be comparatively immaterial to PESI’s 2022 numbers, though I feel the inventory may very properly rally if the corporate’s bidding conglomerate wins the Hanford contract that might be introduced late in 2022. In reality, if that occurs, it might not shock me to see PESI acquired by a a lot bigger firm for a hefty premium to market costs at the moment.

In any case, primarily based on these assumptions, I present PESI incomes $155M in income with EPS of $1.22/share. EBITDA is estimated to be $20.4M. My truthful valuation for these expectations would result in me valuing PESI at $15.20-18.35/share. This represents roughly 200% upside from present costs.

Whereas I’m not “predicting” that PESI will triple throughout the subsequent twelve months, I consider that even when my mannequin is overly optimistic, you may see loads of upside from the $5.50/share worth at which shares have just lately been buying and selling. To that finish, I see PESI having the ability to earn round $0.75/share if they’re merely in a position to return to their 2020 income numbers (roughly $100M in income).

PESI Investor Presentation

2023 Assumptions & Estimates

I anticipate 2023 would be the 12 months when PESI actually begins to take off from a income and EPS standpoint. Nonetheless, as I famous within the subsection above, the inventory worth may transfer materially earlier than that if PESI wins the Hanford website contract. The rationale for that’s that if PESI wins that contract, they’ll nearly definitely deal with no less than 300,000 gallons of waste from Hanford, at roughly $70/gallon income, in 2023.

Along with Hanford selecting up, I’d anticipate the worldwide enterprise to start growing and for the submarine work to maneuver larger as properly. You’ll be able to see these respective sections above to study why I feel it is a cheap assumption.

With all these components taken into consideration, I estimate FY 2023 income for PESI of $220M, EPS of $2.00/share, and EBITDA of $31M. The midpoint of my truthful valuation calculations is round $26.85/share, almost 400% returns from present costs.

2024 Assumptions & Estimates

My estimates for 2024 are almost unbelievable if one doesn’t run the maths and do the analysis. If PESI wins Hanford, they anticipate to have the ability to deal with no less than 1M gallons of waste per 12 months (possible ultimately extra) as soon as the venture is totally operational. My 2024 estimates take that into consideration, in addition to assuming modest will increase in worldwide and submarine enterprise.

All of those assumptions lead me to estimate PESI’s 2024 numbers as $285M of income, EPS of over $3.00/share, and EBITDA of $46M. These numbers would lead me to valuing PESI at round $40/share, properly over 600% larger than in the present day’s costs.

Conclusion

I perceive it appears not possible, at first look, to examine a waste administration and providers firm going from FY21 income of $72M to FY24 income of $285M. Nonetheless, my assumptions and estimates are clearly defined and primarily based on publicly accessible knowledge that helps them. There are clearly some ways PESI and its buyers can succeed that’s someplace between $5.50/share and the $40/share risk I point out by 2024.

However one factor is evident to me: PESI is value a core place in my portfolio, most particularly at this $5.50/share stage. The corporate is popping out of a once-in-a-lifetime headwind (a worldwide pandemic), with a number of tailwinds to assist them sail ahead. The corporate’s present Providers backlog alone signifies no less than 40%+ income development from that section, earlier than factoring in attainable new contracts. As well as, they seem to have materials alternatives for brand spanking new enterprise associated to worldwide growth, MATOCs, and the de-commissioning of U.S. Navy submarines. On these prospects alone, the inventory is probably going a purchase at $5.50/share. However add to that the Hanford website risk, and I consider PESI is a no brainer to be in a small-cap portfolio.

{kind=link}