designer491

FPE technique and portfolio

The First Belief Most well-liked Securities and Revenue ETF (NYSEARCA:FPE) is a excessive yield fund paying month-to-month distributions with a distribution fee of 6.01% and a complete expense ratio of 0.85%. It was launched on 2/11/2013 with the target “to hunt whole return and to supply present earnings”.

The fund doesn’t monitor an index. As described by First Belief within the prospectus, it’s actively managed primarily based on “three important areas of study: credit score fundamentals; relative worth; and technical points of the securities, which can embrace, however aren’t restricted to, rate of interest sensitivity, name options, covenants, maturities, buying and selling volumes, liquidity and pricing inefficiencies.”

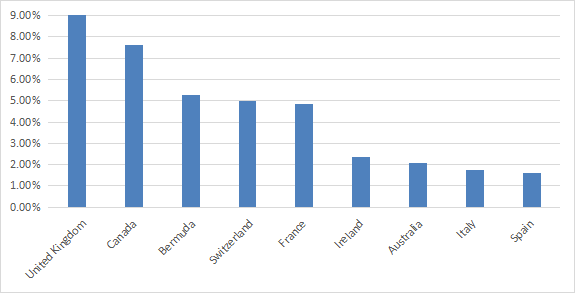

About 54% of asset worth is in securities issued by U.S. firms. The following chart plots weights of the fund’s prime international locations excluding the U.S.

FPE international locations ex U.S. ( chart: writer; knowledge: First Belief)

The following desk lists the 12 holdings which can be above 1% of asset worth (supply: First Belief). Their mixture weight is about 16%.

|

Identify |

CUSIP |

Weight |

|

AERCAP HOLDINGS NV Variable fee, due 10/10/2079 |

00774YAA7 |

2.21% |

|

BARCLAYS PLC Variable fee |

06738EBG9 |

2.16% |

|

Wells Fargo & Firm, Sequence L, 7.50% (WFC.L) |

949746804 |

1.73% |

|

HIGHLAND HOLDINGS BOND 7.625%, due 10/15/2025 |

43103QAA6 |

1.51% |

|

WELLS FARGO & COMPANY Variable fee |

949746TD3 |

1.17% |

|

CREDIT SUISSE GROUP AG Variable fee |

225401AJ7 |

1.14% |

|

GLOBAL ATLANTIC Variable fee, due 10/15/2051 |

37959GAC1 |

1.11% |

|

SOCIETE GENERALE Variable fee |

83370RAA6 |

1.06% |

|

DEUTSCHE BANK AG Variable fee |

251525AX9 |

1.04% |

|

AMER AGCREDIT ACA Variable fee |

02369GAA3 |

1.01% |

|

Financial institution of America Company, Sequence L, 7.25% (BAC.L) |

60505682 |

1.01% |

|

ENBRIDGE INC. Variable fee, due 01/15/2077 |

29250NAN5 |

1.01% |

Efficiency

Since March 2013, FPE has overwhelmed its 3 main opponents in the identical asset class: the iShares Most well-liked and Revenue Securities ETF (PFF), the Invesco Most well-liked Portfolio ETF (PGX) and the SPDR ICE Most well-liked Securities ETF (PSK). It additionally beats a diversified company bond fund: the iShares iBoxx $ Funding Grade Company Bond ETF (LQD). Nevertheless, it’s far behind the fairness benchmark S&P 500 (SPY).

|

since 3/1/2013 |

Complete Return |

Annual.Return |

Drawdown |

Sharpe ratio |

Volatility |

|

FPE |

37.92% |

3.32% |

-38.30% |

0.37 |

7.83% |

|

PFF |

30.07% |

2.71% |

-35.48% |

0.29 |

8.59% |

|

PGX |

28.97% |

2.62% |

-35.41% |

0.28 |

8.18% |

|

PSK |

24.76% |

2.27% |

-32.89% |

0.24 |

8.05% |

|

SPY |

210.85% |

12.21% |

-32.05% |

0.82 |

14.53% |

|

LQD |

14.59% |

1.39% |

-25.44% |

0.15 |

6.87% |

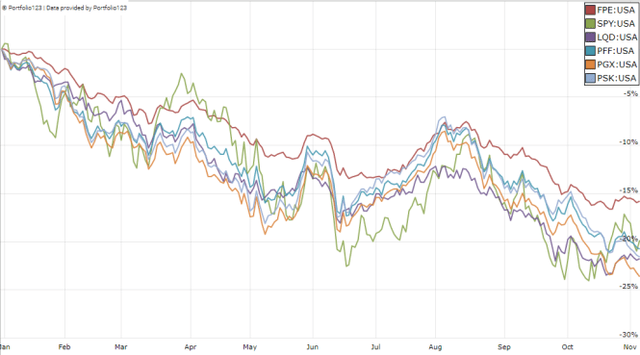

Yr-to-date, FPE beats not solely its opponents, but in addition each the fairness benchmark and the company bond ETF (see subsequent chart).

FPE vs opponents, plus SPY and LQD in 2022 so far (Portfolio123)

The desk above reveals a regarding reality: the annualized return reinvesting all distributions, with out paying any tax on them, is inferior to the distribution fee. This factors to capital decay. It’s confirmed by FPE share worth historical past (with out dividend): it has misplaced about 18% since inception.

FPE share worth with out dividends ( TradingView on SeekingAlpha)

Distribution historical past reveals one other regarding reality: the annual sum of month-to-month distributions went down from $1.13 in 2014 to $0.91 in 2021 (supply). The distribution for the primary 9 months of 2022 is $0.77, so the annual sum could also be about $0.92 this 12 months if it stays on the identical path. Based mostly on 2021 numbers, the loss in annual earnings in 7 years is nineteen.5%. These numbers aren’t as dangerous as for SPFF in the identical interval (evaluate right here), however they aren’t engaging.

In abstract, FPE has performed very effectively relative to its friends in the identical asset class. The difficulty is that, basically, this asset class has suffered capital decay and earnings stream decay for years. I doubt it would do higher sooner or later. The total image for an income-seeking investor should additionally keep in mind the extra drags of inflation fee and tax paid on distributions. This concern will not be particular to most popular inventory ETFs: securities with yields above 6% undergo from capital decay, on common (there are uncommon exceptions). The ten-year common annualized return together with dividends of all ETFs with a yield of 6% or extra is effectively beneath the typical yield.

Easy methods to handle capital decay in excessive yield securities

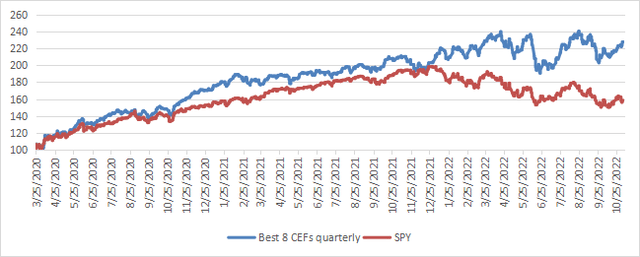

Capital and earnings decay is a structural concern in lots of closed-end funds, like in most high-yield devices. Nevertheless, it isn’t inexorable if one is aware of commerce CEFs as an alternative of utilizing them as buy-and-hold devices. I designed a 5-factor rating system statistically associated to ahead returns throughout the total CEF universe, and began publishing the 8 greatest ranked liquid CEFs in Quantitative Danger & Worth (QRV) after the March 2020 market meltdown. The listing is up to date each week. Its common dividend yield varies round 7-8%. It’s not a mannequin portfolio: buying and selling the listing each week is just too pricey in spreads and slippage. Its goal helps earnings traders discover funds with a very good entry level. Within the desk and chart beneath, I give the hypothetical instance of beginning a portfolio on 3/25/2020 with my preliminary “Finest 8 Ranked CEFs” listing and updating it each 3 months since then, ignoring intermediate updates to restrict transaction prices. Returns are calculated with holdings initially in equal weights with out rebalancing till the following 3-month replace. Dividends are reinvested originally of each 3-month interval.

|

since 3/25/2020 |

Complete Return |

Annual.Return |

Drawdown |

Sharpe ratio |

Volatility |

|

Finest 8 CEFs quarterly |

127.90% |

36.94% |

-20.60% |

1.52 |

20.50% |

|

FPE |

21.90% |

7.85% |

-17.10% |

0.41 |

9.28% |

|

SPY |

59.55% |

19.52% |

-26.29% |

0.96 |

18.79% |

|

LQD |

-7.98% |

-3.13% |

-25.44% |

-0.55 |

9.59% |

This simulation will not be an actual portfolio and never a assure of future return (Information calculated with Portfolio123)

The standard disclaimer says that previous efficiency (actual or simulated) will not be consultant of future return. To be sincere, the “Finest 8” listing is unlikely to carry out as effectively in a close to future as since March 2020. The 2020 meltdown and restoration resulted in worth dislocation and distinctive alternatives within the CEF universe. The 2022 downturn was additionally a supply of alternatives in power and infrastructure funds. That is unlikely to be reproducible sooner or later. Nevertheless, I feel a discount-driven rotational technique in CEFs has a significantly better probability to guard each capital and earnings stream in opposition to erosion and inflation than any high-yield passive funding like FPE. Dates and lists might be checked in QRV submit historical past.

{kind=link}