Michele Tantussi/Getty Pictures Information

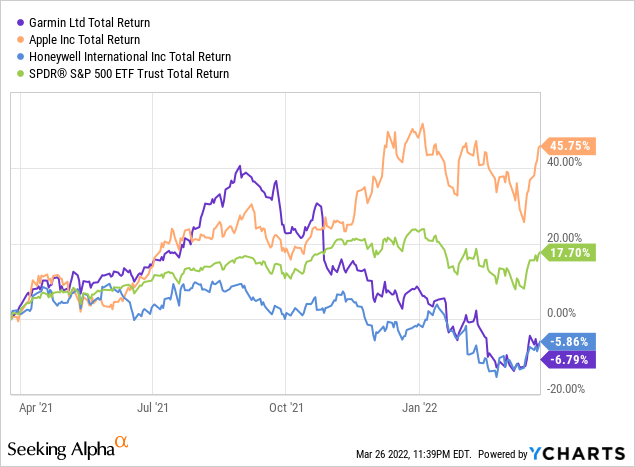

Over the past twelve months, Garmin (NYSE:GRMN) has seen 6% of shareholder worth worn out whereas the broader market S&P 500 was up 18% and Apple (AAPL) gained practically 50%. That is significantly shocking provided that Garmin grew income practically 20% y-o-y to ~$5 billion, led by robust double-digit returns throughout all segments. Whereas Garmin is well-known for its GPS gadgets, it has underappreciated potential in wearable know-how (suppose digital watch) and health purposes. Though Apple often is the chief in something pocket-sized know-how, Garmin is customized to additional penetrate the wearable house. At 17.5x ahead earnings, a dividend yield of two.3%, and wholesome gross margins of 58%, at first blush, it’s a worth play relative to Apple, which trades at 26.6x with solely 43% gross margin. The margins between the 2 aren’t precisely comparable, however the truth that Garmin is ready to generate superior gross margins to Apple definitely says one thing in regards to the high quality of its merchandise within the market.

In line with Searching for Alpha information, the Avenue is usually optimistic on the inventory. Almost 75% charge the inventory a “purchase” or “robust purchase”. This sentiment is significantly extra bullish than again in June 2020 when solely 25% put the inventory in “purchase” territory. A part of the shifting optimism has to do with robust tailwinds in smartwatches and the “better-for-you” health financial system. Fourth quarter outcomes had been much better than anticipated because of stable margins, and the corporate managed provide chain challenges higher than many others. Income CAGR since 4Q2019 is 12%, reflecting a enterprise with stable fundamentals regardless of the discounted valuation. Administration is now anticipating 20% y-o-y development in 2022 for Outside, with important traction in journey watches

DCF Evaluation Signifies Vital Upside

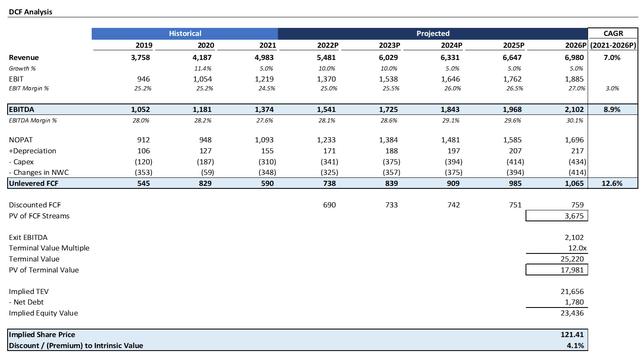

To get a way of the corporate’s intrinsic worth, I ran a DCF evaluation. No DCF evaluation can present an ideal image of future returns for shareholders; nevertheless, they will present an illustrative “story” of the chance of various situations. In my DCF evaluation, I assumed 10% income development in 2022 staggering to five% by 2026. I additionally assumed EBIT margins increasing modestly by 200 bps over the following 5 years. Capex, improve in web working capital, depreciation, and taxes had been flat-lined for simplicity.

Supply: Created by writer utilizing information from Yahoo! Finance

Assuming a terminal EBITDA a number of of 12x and a 7% low cost charge, the inventory is barely undervalued. As a lot as I might love the inventory to be undervalued to name it a “true” worth play, the reality is that worth is tough to return by in right now’s market, interval. Thus, at this level, I discover it enticing to merely put money into an organization that isn’t materially overvalued. It is very important notice that Garmin’s a number of has ranged considerably over the previous 15 years from 8x to 15x, so the 12x estimate I’m utilizing is inside vary.

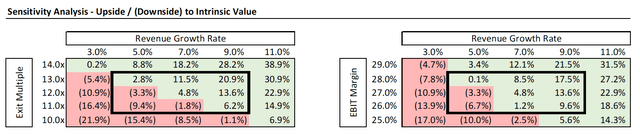

Supply: Created by writer utilizing information from Yahoo! Finance

Looking on the sensitivity evaluation, issues look extra rosy. Even when the inventory had been to contract to the low finish at 10x and development involves a halt at GDP ranges of three%, there’s 20% draw back right here—not too worrisome provided that this assumes “the worst” and is offset by the 7% annual returns inherent within the low cost charge. If the inventory had been to develop at a 11% clip and see its a number of contract to 13x from right now’s 16x degree, the inventory would have 30% overvalued. Accordingly, I imagine Garmin has very favorable threat/reward.

Upside Catalysts

There are a number of catalysts that would get Garmin to shut its low cost to intrinsic worth. First, decongestion of the provision chain is essential. The supply of digital parts is making this a difficult atmosphere for everybody, though I think the market is discounting this cyclical challenge an excessive amount of into the long-term forecast. Fortuitously, Garmin has a vertically built-in footprint that it might probably leverage to extra agilely navigate the provision chain than a few of its opponents can. Second, I’m additionally bullish in regards to the firm’s Lily smartwatch product and the launch of the all-new Intuition 2 Sequence in two sizes. Demand for Garmin’s smartwatches have been important to date, and I imagine it’s positioned to additional acquire market share and eat away at Fitbit and Apple’s iWatch. Normally, Garmin’s Outside section advantages from the secular shift in the direction of more healthy life (or at the least, makes an attempt at them). The pandemic drove loads of curiosity in energetic life and figuring out, and I anticipate this development solely persevering with to develop.

I’m additionally extraordinarily optimistic in regards to the firm’s auto place. Full yr income grew 26% final yr, and yearly an increasing number of automobiles are that includes Garmin’s know-how. BMW lately unveiled their imaginative and prescient for in-car leisure, the place Garmin will begin manufacturing for later this yr earlier than ramping up considerably in 2023.

Why I Might Be Mistaken

There are a number of components that mood my optimism. Firstly, in right now’s mega-cap tech craze, will probably be exhausting for Garmin to garner a lot consideration even when it did hearth on all cylinders. Robust competitors within the smartwatch house additionally hinder the flexibility to have a lot foresight in top-line development. Administration has additionally said that it’s trying to improve costs; in gentle of the competitors, this gained’t essentially be a “test the field” type of train. Lastly, whereas the corporate’s long-run potential in auto seems to be promising, the short-term shall be difficult provided that it comes with decrease margins. Provided that a lot of the enchantment of the inventory is in its margins, it’s due to this fact ironic that the excessive development catalyst provides an opposed combine change from this attitude. Lastly, there could also be a stronger-than-expected pullback in demand for biking merchandise as pandemic-fueled demand tempers.

Conclusion

It’s exhausting to seek out any really undervalued inventory in right now’s market. However, Garmin stands out as a development play at an inexpensive valuation with a fabric upside story. With a shareholder pleasant capital allocation coverage and robust secular tailwinds in wearable know-how, Garmin is effectively positioned to leverage its vertical integration to generate outsized returns. The inventory’s underperformance relative to the broader market is out of line provided that operational execution has typically been robust, margins stay stable, and development alternatives proceed to show actionable. With giant outside occasions like half marathons and 10Ks returning, you may anticipate finding a resurgence in Garmin’s merchandise, which is recent from some revolutionary launches. So, though Apple could proceed to keep up the main notion out there, Garmin’s merchandise stay top-of-line and poised for future outperformance.

{kind=link}