Anthony Bradshaw

After reaching prior highs simply above $220 throughout the first half of April 2020, the SPDR Gold Shares Belief (NYSEARCA:GLD) has had a particularly troublesome time sustaining these lofty valuations – and the ensuing short-term volatility that has been seen after this bearish rejection has many traders questioning if the large bull run that now we have seen in funds tied to the underlying worth of valuable metals has lastly come to an finish.

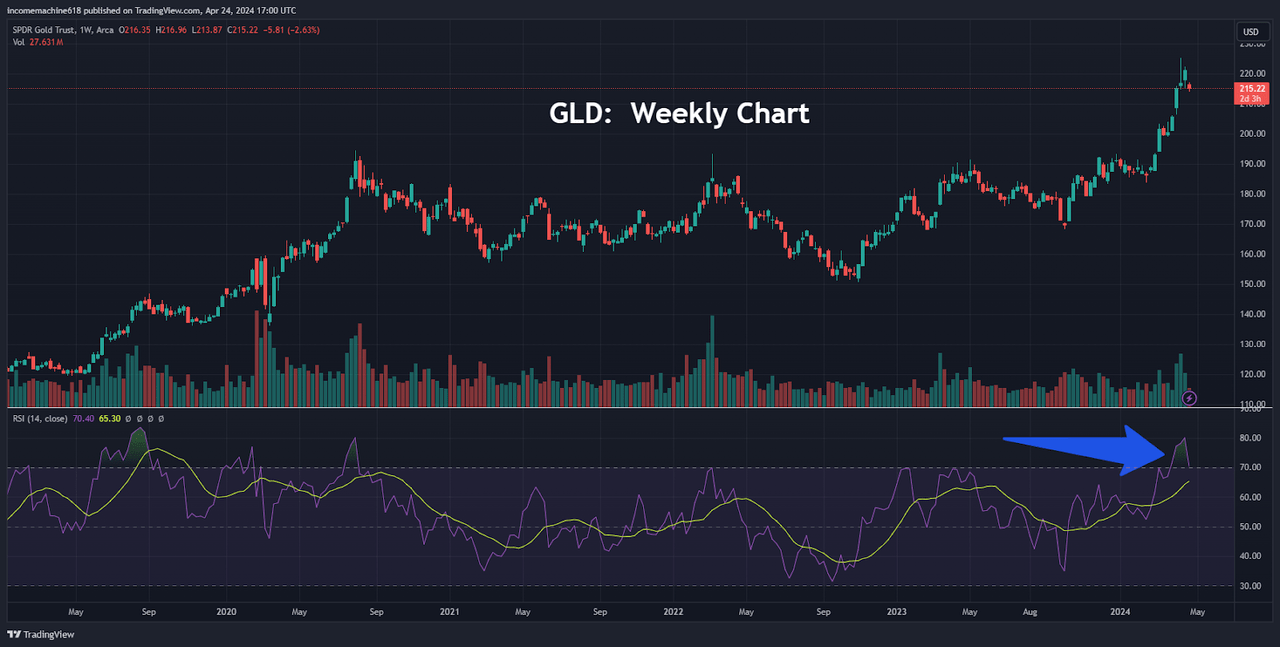

GLD Overbought Technical Indicator (Earnings Generator through TradingView)

When wanting on the SPDR Gold Belief ETF’s current value historical past, one clear attribute that may be cited as a trigger for concern could be discovered within the Relative Power Index (RSI), which is a carefully watched momentum indicator that was designed to sign overbought and oversold situations in market property. Particularly, GLD’s current breakout exercise despatched fund valuations into extremely overbought territory – at ranges which had not been seen since early August 2020 (in a previous market transfer that precipitated prolonged declines towards the lows simply above $150 in October 2022).

However whereas a majority of these technical indicators do have their deserves, many of those alerts could be distorted by the broader pattern exercise that characterizes the value motion that may be seen throughout particular intervals of time.

On this case, GLD was basically caught in a long-term sideways pattern that was outlined by a broader vary of lower than $40. In different phrases, what might need gave the impression to be risky exercise primarily based on indicator readings really resulted in comparatively minor value strikes when it comes to precise market value variations.

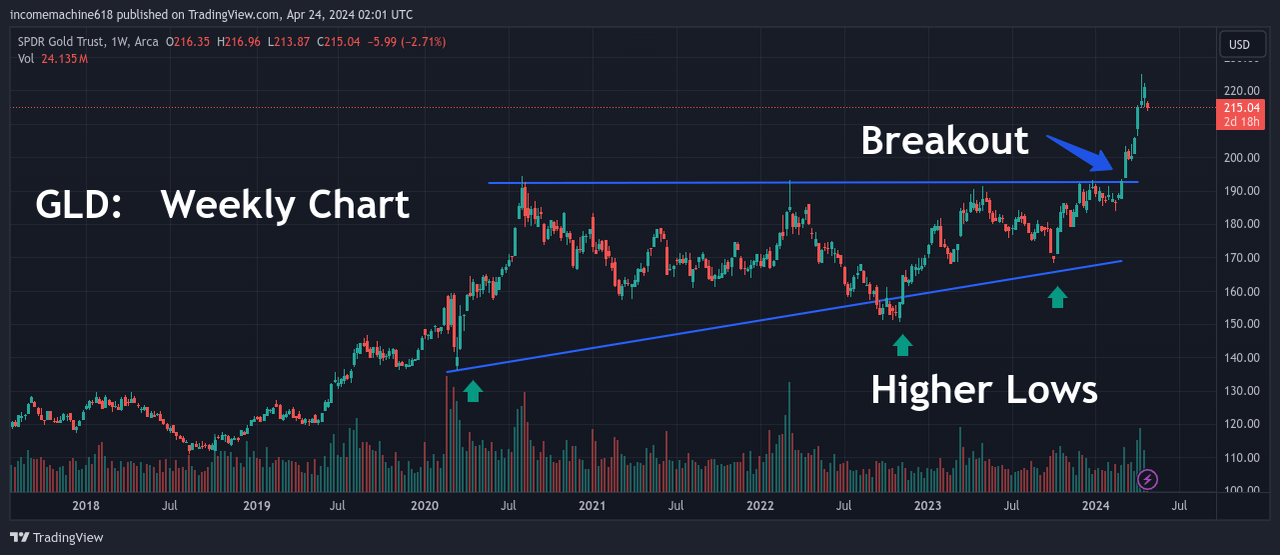

Lengthy-term GLD Development Exercise (Earnings Generator through TradingView)

Extra not too long ago, nevertheless, value exercise in GLD has been rather more decisive. In abstract, a sequence of upper value lows (beginning in March 2020) in the end led to a pointy breakout that turned fairly obvious in February of this 12 months.

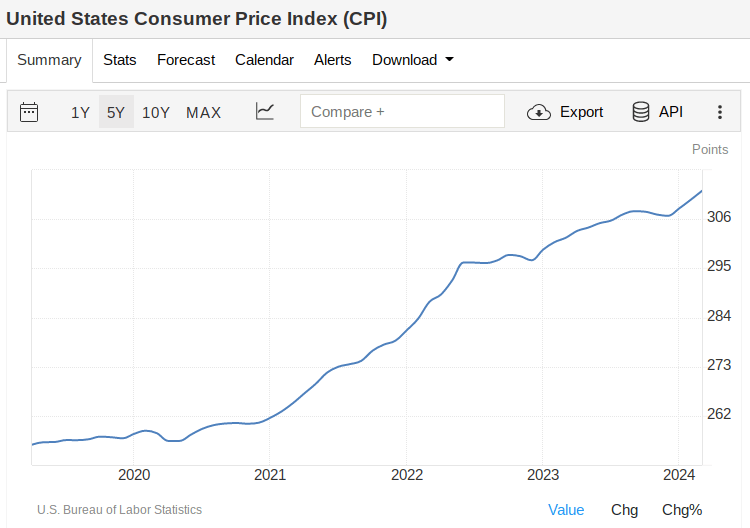

Basically, this decisive pattern exercise could be analyzed from a long-term perspective and these strikes strongly correlate with the rising framework in U.S. shopper inflation knowledge that has characterised the nation’s financial system throughout the identical time frame.

Lengthy-term CPI Tendencies Proceed (Buying and selling Economics / U.S. Bureau of Labor Statistics)

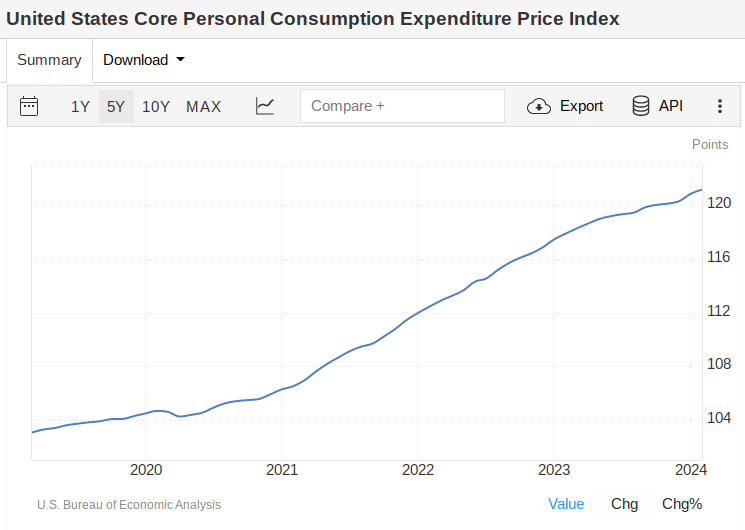

Sadly, these problematic traits in shopper inflation have been fairly obvious irrespective of which knowledge report is used as the idea for the evaluation. Shopper Value Index (CPI) readings are inclined to get essentially the most consideration within the U.S. information media however traits in Private Consumption Expenditures (PCE) are sometimes cited because the Federal Reserve’s most well-liked methodology for analyzing these financial traits and may present a greater indicator of modifications we’re more likely to see in U.S. rate of interest ranges earlier than the top of this 12 months.

Lengthy-term PCE Tendencies Proceed (Buying and selling Economics / U.S. Bureau of Financial Evaluation)

In any case, it is rather troublesome to disclaim the clear confluences that now we have seen with the robust upward spike in U.S. inflation knowledge and the start of the long-term upward trajectory that now we have seen within the SPDR Gold Belief over the identical time frame.

Given the sustained power of those correlations, it makes little sense to commerce GLD from the bearish perspective whereas counting on short-term overbought readings that may be present in value chart indicators (comparable to RSI) so long as these problematic financial traits present no substantive indicators of a sustainable reversal.

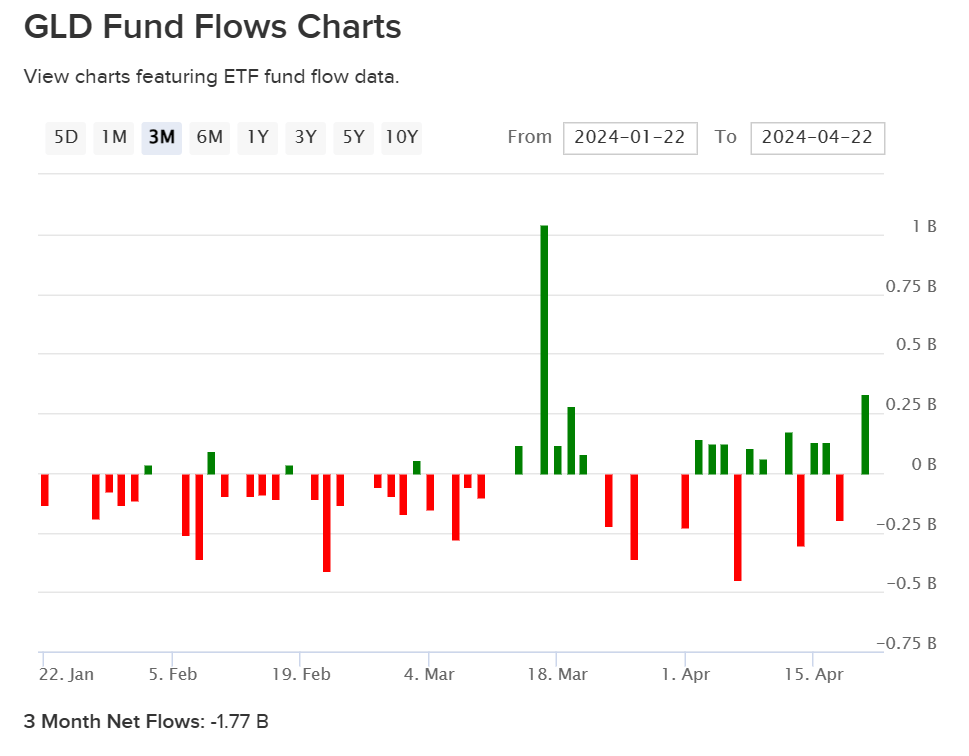

Quick-term GLD Flows Flip Unfavourable (ETFdb)

All of that stated, it’s at all times essential to keep up a balanced view and search for potential causes which could dismantle the bullish arguments for GLD. One space that alerts some trigger for concern could be discovered within the fund flows themselves. Particularly, fund flows within the SPDR Gold Belief ETF have formally flipped into damaging territory if we’re taking a look at investor exercise over the newest three-month interval.

Over this timeframe, GLD investor outflows can now be seen at -1.77 billion and this does lend some credence to the argument that the market may be prepared to gather some earnings after the large bullish run that valuable metals funds have skilled for the reason that starting of this 12 months.

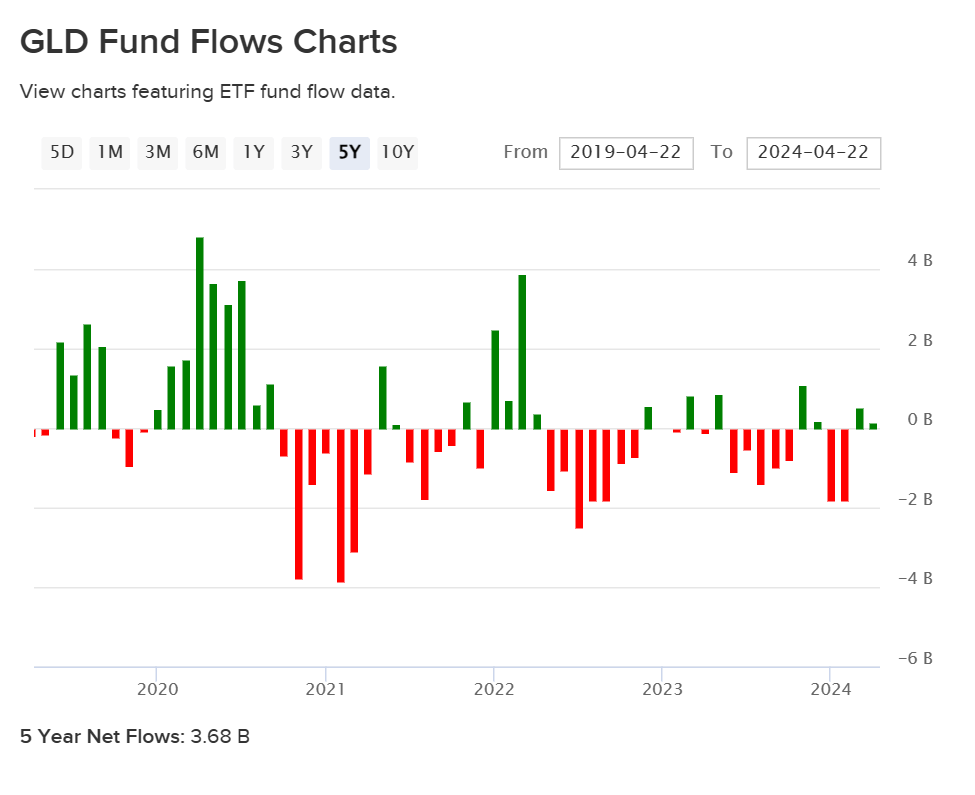

Lengthy-term GLD Flows Stay Constructive (ETFdb)

Nonetheless, longer-term proof calling for continued power within the SPDR Gold Belief ETF could be discovered within the fund flows over the past five-year interval. Over this timeframe, investor exercise stays firmly in bullish territory, with the SPDR Gold Belief attracting optimistic inflows of three.68 billion.

On stability, all of this exercise stays favorable as this implies that the market is just not closely lengthy GLD even whereas the fund remains to be buying and selling at elevated value ranges. In different phrases, current outflow exercise means that extra new consumers are nonetheless accessible to enter the market and drive strikes greater into the top of 2024.

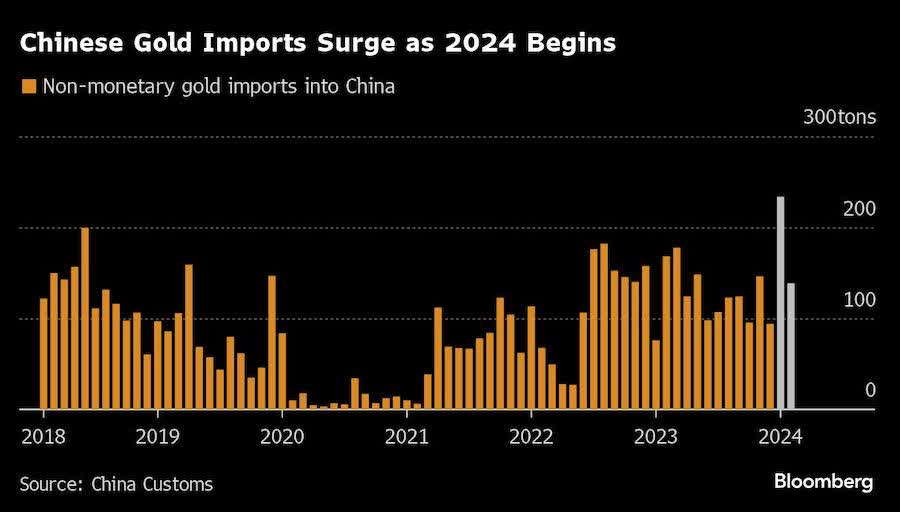

China Purchases Stay Strong (China Customs / Bloomberg)

With robust central financial institution shopping for exercise seen in various areas world wide, we are able to clearly see that broad curiosity on this asset class stays strong and lots of on Wall Road additionally look like onboard with this bullish outlook. After all, most of this shopping for exercise has occurred in China and this has helped generate hypothesis that additional market rallies may very well be susceptible if the Center Kingdom decides to focus its consideration on different areas of the market.

However a big portion of Wall Road’s analyst neighborhood nonetheless appears to be onboard with the optimistic outlook, with some analysts really suggesting that the current April declines could be seen as a wholesome correction in an in any other case steady uptrend. All of this thought of, we’re siding with the bullish facet of the argument and sustaining our lengthy place in GLD as a protecting measure of security in an in any other case risky market.

With navy exercise persevering with in each Ukraine and the Center East, it appears unlikely that the market shall be trying to undertake a risk-off mentality any time quickly. Since GLD tends to be one of many market’s hottest beneficiaries throughout cases of broader geopolitical instability and long-term U.S. inflation ranges present little or no signal of manufacturing a sustainable reversal previous to the 2024 U.S. Presidential election, we predict it makes rather more sense to miss short-term fluctuations in technical value indicators and as an alternative deal with the extra influential points of asset valuation which might be more likely to affect these traits over time.

{kind=link}