The pandemic and ensuing financial disaster have upended any expectations about what well being spending, utilization, and the next monetary efficiency of insurers might need regarded like this 12 months. The unprecedented lower in well being care spending and utilization within the spring led to rising margins and income for a lot of insurers. In the summertime and fall of this 12 months, spending and repair utilization rebounded as sufferers returned for routine and elective care, including to prices related to testing and treating sufferers with COVID-19. Job losses and financial instability have pushed elevated enrollment in Medicaid broadly and will increase in Medicaid managed care however seemingly modest modifications in enrollment within the group and particular person markets to this point.

On this temporary, we analyze third quarter information from 2018 to 2020 to look at how insurance coverage markets carried out financially by means of the tip of September, because the pandemic continued and well being care utilization climbed again in direction of earlier ranges. We use monetary information reported by insurance coverage corporations to the Nationwide Affiliation of Insurance coverage Commissioners (NAIC) and compiled by Mark Farrah Associates to take a look at common medical loss ratios and gross margins within the Medicare Benefit, Medicaid managed care, particular person (non-group), and fully-insured group (employer) medical insurance markets by means of the third quarter of every 12 months. Third quarter information is year-to-date from January 1 – September 30. A extra detailed description of every market is included within the Appendix.

By the tip of September, common margins throughout these 4 markets remained comparatively excessive (and loss ratios comparatively low or flat) in comparison with the identical level in recent times. These findings counsel that many insurers have remained worthwhile at the same time as each COVID-related and non-COVID care elevated within the third quarter of 2020. The outcomes for the person and group markets proceed to point that industrial insurers are going to owe substantial rebates to shoppers once more subsequent 12 months beneath the Inexpensive Care Act’s (ACA) Medical Loss Ratio provision. For Medicaid, utility of threat sharing preparations that many states have in place might in the end cut back total margins calculated within the quarterly information.

Gross Margins

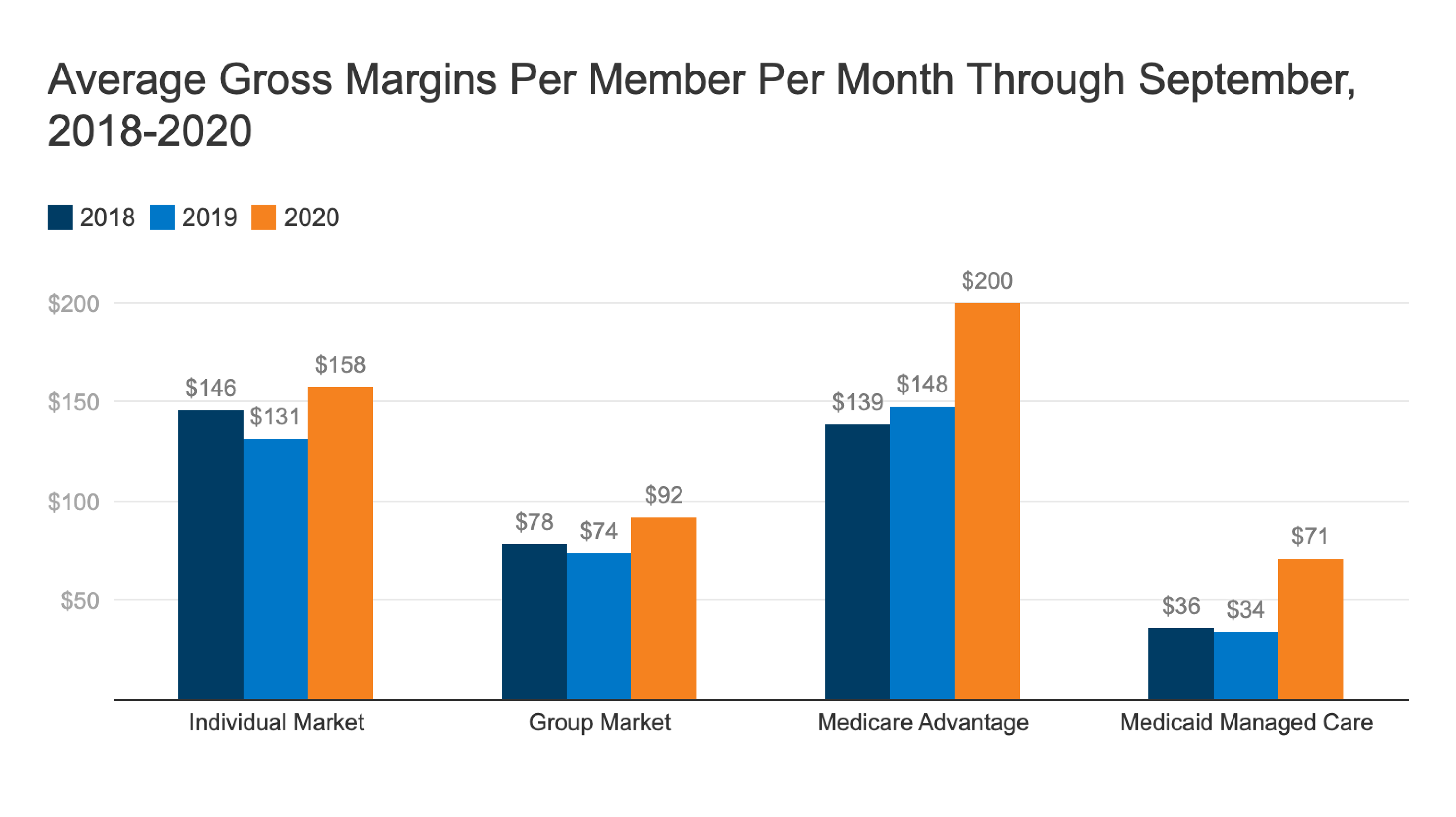

One solution to assess insurer monetary efficiency is to look at common gross margins per member per 30 days, or the common quantity by which premium revenue exceeds claims prices per enrollee in a given month. Gross margins are an indicator of monetary efficiency, however optimistic margins don’t essentially translate into profitability since they don’t account for administrative bills. Nevertheless, a pointy improve in margins from one 12 months to the following, with no commensurate improve in administrative prices, would point out that these medical insurance markets have grow to be extra worthwhile through the pandemic.

Insurers are nonetheless required to cowl the complete price of coronavirus testing and lots of have continued to voluntarily waive out-of-pocket prices for coronavirus remedy. Nonetheless, insurers have seen their claims prices fall and margins improve relative to 2019.

On the finish of the third quarter of 2020, common gross margins amongst particular person market and fully-insured group market plans have been 21% and 24% increased, respectively, than on the identical level final 12 months. Gross margins amongst Medicare Benefit plans have been 35% increased by means of the third quarter in comparison with 2019. (Gross margins per member per 30 days for Medicare Benefit plans are typically increased than for different medical insurance markets primarily as a result of Medicare covers an older, sicker inhabitants with increased common prices).

Common gross margins for managed care organizations (MCOs) within the Medicaid market have been greater than twice as excessive by means of the third quarter of 2020 as they have been by means of the third quarter of 2019 (a 109% improve). Nevertheless, in comparison with the opposite markets, margins within the Medicaid MCO market are decrease as a result of whereas charges have to be actuarially sound, fee charges in Medicaid are typically decrease than different markets. States usually use a wide range of mechanisms to regulate plan threat, incentivize efficiency and guarantee funds usually are not too excessive or too low, together with numerous choices to switch their capitation charges or use threat sharing mechanisms. CMS has offered steerage about choices to regulate funds for MCOs through the pandemic, since states and plans couldn’t have moderately predicted the modifications in utilization and spending which have occurred. Many of those changes that states could make might happen retrospectively and will not be mirrored within the quarterly information.

Medical Loss Ratios

One other solution to assess insurer monetary efficiency is to take a look at medical loss ratios, or the % of premium revenue that insurers pay out within the type of medical claims. Typically, decrease medical loss ratios imply that insurers have extra revenue remaining after paying medical prices to make use of for administrative prices or maintain as income. Every medical insurance market has completely different administrative wants and prices, so low loss ratios in a single market don’t essentially imply that market is extra worthwhile than one other market. Nevertheless, in a given market, if administrative prices maintain largely fixed from one 12 months to the following, a drop in medical loss ratios would suggest that plans have gotten extra worthwhile.

Medical loss ratios are utilized in state and federal insurance coverage regulation in a wide range of methods. Within the industrial insurance coverage (particular person and group) markets, insurers should problem rebates to people and companies if their loss ratios fail to succeed in minimal requirements set by the ACA. Medicare Benefit insurers are required to report loss ratios on the contract stage; they’re additionally required to problem rebates to the federal authorities if their MLRs fall in need of required ranges and are topic to further penalties in the event that they fail to fulfill loss ratio necessities for a number of consecutive years in a row. For Medicaid MCOs, CMS requires states to develop capitation charges for Medicaid to realize an MLR of at the least 85%. There isn’t a federal requirement for Medicaid plans to pay remittances in the event that they fail to fulfill their MLR threshold, however a majority of states that contract with MCOs do require remittances all the time or in some circumstances.

The medical loss ratios proven on this problem temporary differ from the definition of MLR within the ACA and CMS Medicaid managed care ultimate rule, which makes some changes for high quality enchancment and taxes, and don’t account for reinsurance, threat corridors, or threat adjustment funds. The chart beneath exhibits easy medical loss ratios, or the share of premium revenue that insurers pay out in claims, with none modifications (Determine 2). Common loss ratios within the Medicare Benefit market decreased 4 proportion factors by means of the primary 9 months of 2020 relative to the identical interval in 2019, and common loss ratios within the Medicaid managed care market decreased by a mean of seven proportion factors, however nonetheless on common met the 85% minimal even with out accounting for potential changes. Group market loss ratios decreased by a mean of three proportion factors in comparison with the identical level final 12 months.

Common particular person market loss ratios additionally decreased 4 proportion factors in 2020 in comparison with the third quarter of final 12 months. Loss ratios within the particular person market have been already fairly low and insurers out there just lately issued record-large rebates to shoppers primarily based on their expertise in 2017, 2018, and 2019.

Dialogue

Simply as we present in our mid-year evaluation, it nonetheless seems that well being insurers in most markets have grow to be extra worthwhile through the pandemic, although we will’t measure income straight with out administrative price information. Throughout all 4 markets we examined, common gross margins are increased and medical loss ratios are decrease than they have been at this level final 12 months.

The return of elective and routine care this fall, coupled with the continued prices of testing and treating sufferers with COVID-19, contributed to barely increased loss ratios within the Medicare Benefit and group markets within the third quarter in comparison with the second quarter this 12 months, however will increase in claims prices from June by means of September didn’t offset the sharp drop earlier within the 12 months. Common medical loss ratios amongst particular person market plans remained extra secure this previous quarter and are nonetheless nicely beneath the 80% threshold established by the ACA. Loss ratios within the Medicaid MCO market are decrease this 12 months; nevertheless, margins within the Medicaid MCO market are low relative to the opposite markets, and information don’t replicate implementation of present or newly imposed threat sharing mechanisms.

It stays to be seen whether or not spending and use will change considerably in late 2020. Insurers may even see their claims prices fall once more this winter because the pandemic worsens and extra enrollees delay care because of social distancing restrictions or basic worry of contracting the virus. Document numbers of COVID-19 exams and hospitalizations will probably improve claims prices for some insurers although. Insurers are nonetheless typically required to cowl your complete price of COVID-19 testing, and lots of have prolonged their waivers on cost-sharing for COVID-19 remedy by means of the tip of the 12 months. (The affect of COVID-19 hospitalizations on Medicaid MCO funds will fluctuate by state, since states have a number of choices to handle the price of COVID-19 remedy for beneficiaries).

Medicare Benefit insurers that fall in need of required loss ratio necessities for a number of years face further penalties, together with the opportunity of being terminated. Some Medicare Benefit insurers might take this chance to begin providing extra advantages than they at the moment do, that are standard and appeal to enrollees. For Medicaid MCOs, given all of the choices that states have to switch funds and threat agreements through the pandemic, it’s unlikely that these plans will probably be left with sudden surpluses or fail to succeed in their state’s MLR threshold this 12 months.

ACA medical loss ratio rebates in 2021 probably will probably be exceptionally giant throughout industrial markets. Rebates to shoppers are calculated utilizing a three-year common of medical loss ratios, that means that 2021 rebates will probably be primarily based on insurer efficiency in 2018, 2019, and 2020. Particular person market insurers have been fairly worthwhile in 2018 and 2019, so even when insurers have very excessive claims prices within the final three months of 2020, these insurers will probably owe giant rebates to shoppers. Group market insurers can also owe bigger rebates to employers and staff than plans have in typical years, as loss ratios are nonetheless decrease than earlier 12 months.

{kind=link}