Abu Hanifah

Introduction

Whereas many corporations search progress from acquisitions, typically the alternative is required to revitalize an organization. Within the coming years, a number of excessive profile spin-offs might be occurring within the healthcare business as progress stalls among the many giants. Whereas it’s unknown how every spin-off transaction will find yourself influencing returns of the mother and father or new corporations, there’s some information we are able to take a look at to keep up lifelike expectations shifting ahead.

The main future transactions are as follows:

-

Johnson & Johnson (JNJ) Shopper phase

-

Common Electrical (GE) HealthCare

-

3M (MMM) Well being Care

-

Novartis (NVS) spin of Sandoz subsidiary

-

Labcorp (LH) scientific growth division

-

Danaher (DHR) Environmental and Utilized Options phase

Analytics of Spin-offs and Splits

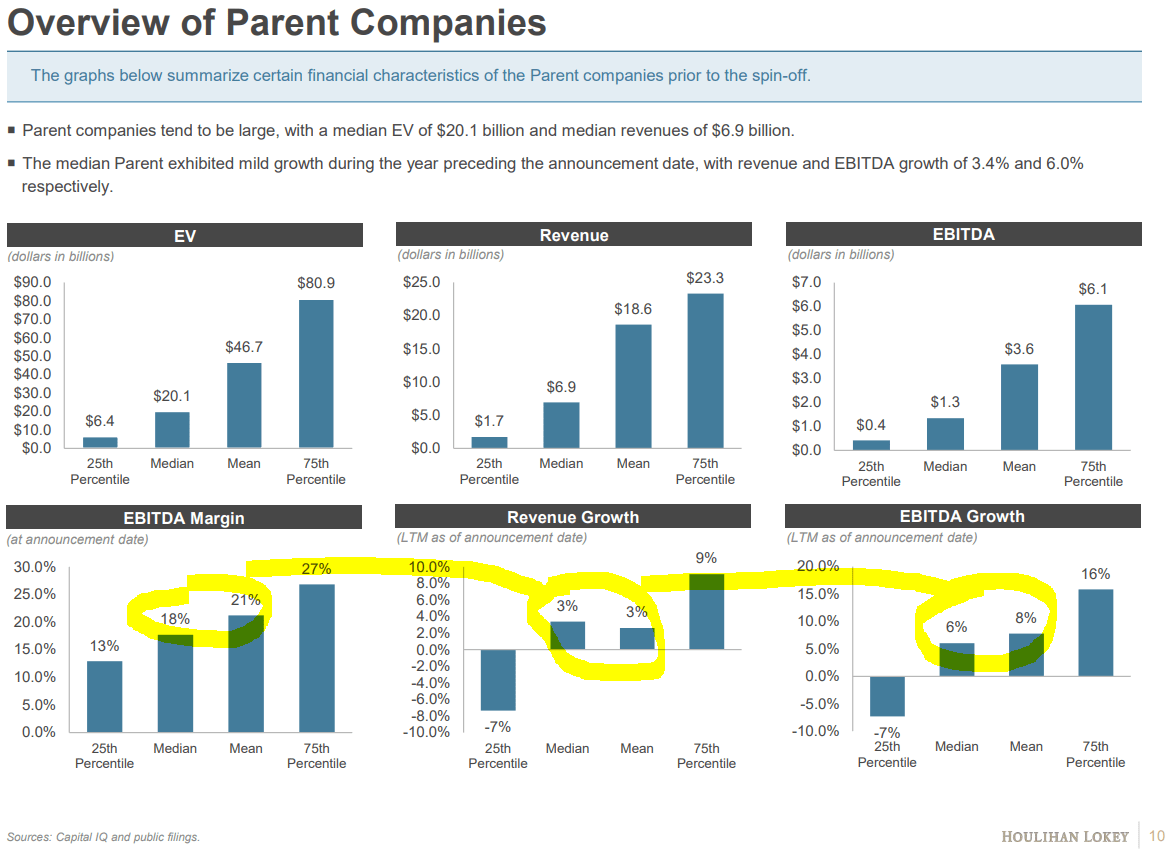

Monetary advisor Houlihan Lokey (HLI) not too long ago revealed a report of spin-offs over the previous three years, and the info therein succinctly summarizes the info driving current spin offs, and subsequent efficiency. Whereas there are distinct patterns and averages that we are able to depend on to generalize the approaching transactions, I imagine it’s pretty simple to find out the winners and losers primarily based on this information and a qualitative evaluation of every firm. However first, let’s take a look at the analytics of current spin-offs between 2019 and 2021.

The primary necessary issue to know is that spin-offs usually are undertaken by giant organizations, between $20 and $46.7 billion in enterprise worth. One other distinction is that these corporations are usually at a mature stage of their life: gradual income progress, and a concentrate on rising profitability. The issue is that this enterprise fashion typically comes with some points such because the regular accumulation of debt, monetary stagnation, and lackluster monetary efficiency.

Buyers definitely aren’t at all times cautious of those points because the dividends proceed to stream, and cap beneficial properties are considered pointless. Nonetheless, corporations understand that with the intention to drive progress and longevity, modifications to the enterprise construction should happen, and a technique to take action is thru a spin-off.

HLI 2022 Spin-Off Transaction Research

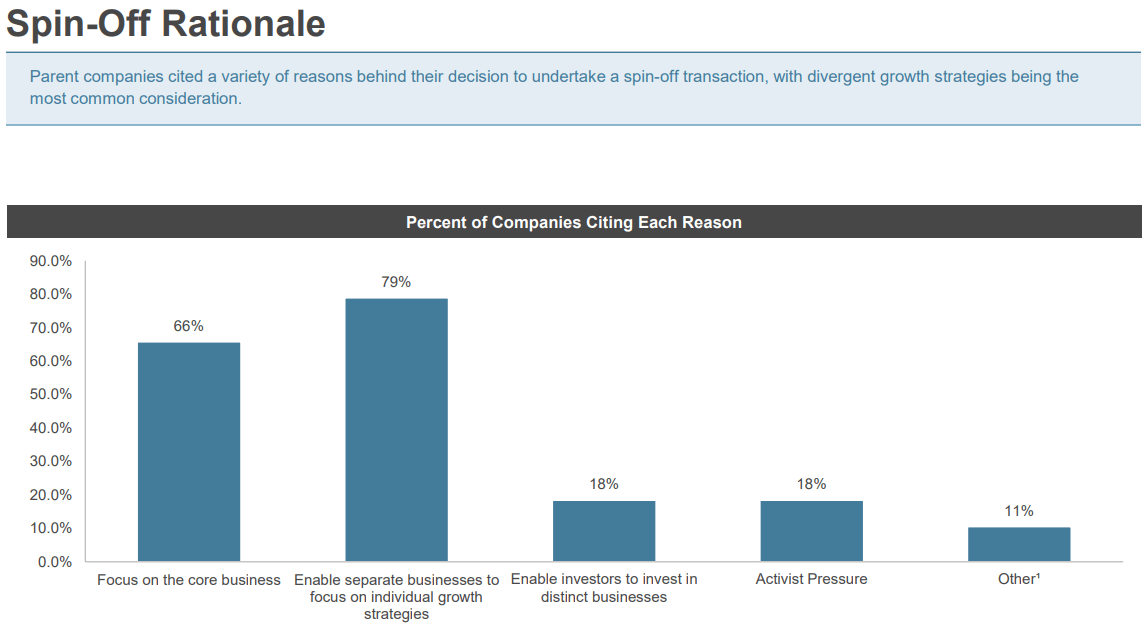

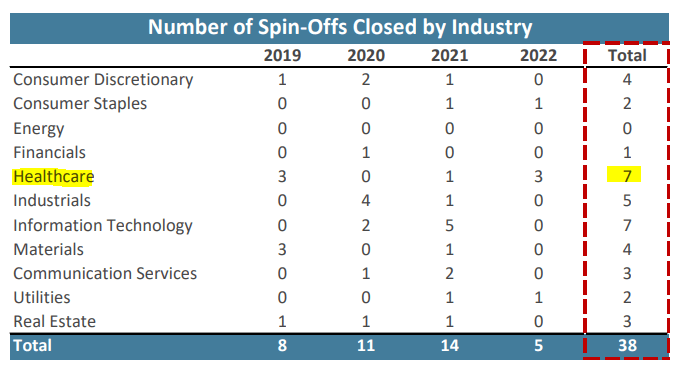

Put in enterprise phrases, administration usually cites a “concentrate on the core enterprise” and enablement of “separate companies to concentrate on particular person progress methods” because the core causes for a spin-off. There’s often by no means one particular person cause for a break up, and different components embrace excessive leverage, activism, political strain, and extra. Because of the various reasoning, spin-offs usually are not restricted to particular person sectors, however healthcare has been seeing a excessive amount of late. In the course of the research’s time interval, seven out of the thirty eight spin-offs have been from throughout the healthcare business. I’ll talk about the main healthcare transactions beneath.

HLI 2022 Spin-Off Transaction Research HLI 2022 Spin-Off Transaction Research

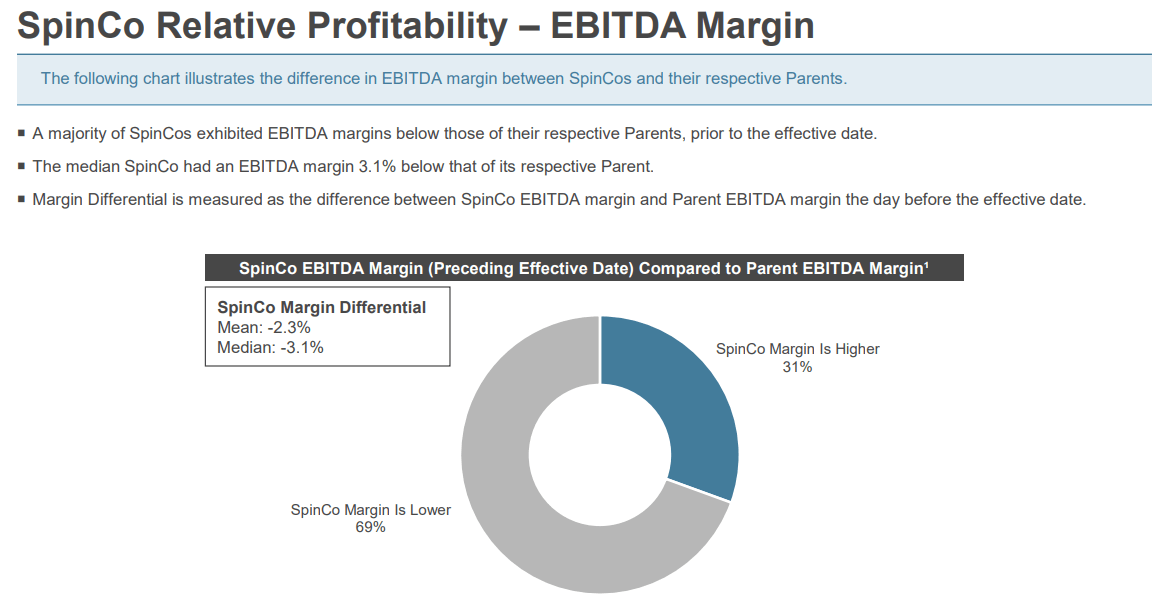

Whereas each spin off is totally different, just a few monetary patterns emerge. Over two-thirds of the SpinCos, or spun off belongings, see a decrease EBITDA margin when working on their very own. This highlights the sample that the majority belongings which can be spunoff are weak and underperforming. Nonetheless, this isn’t true for leverage, and HLI’s information does point out that leverage is in truth decrease for the SpinCos. This contradicts the widespread delusion that SpinCos are saddled with the mother or father firm’s debt, however the SpinCos nonetheless see poorer monetary efficiency.

HLI 2022 Spin-Off Transaction Research

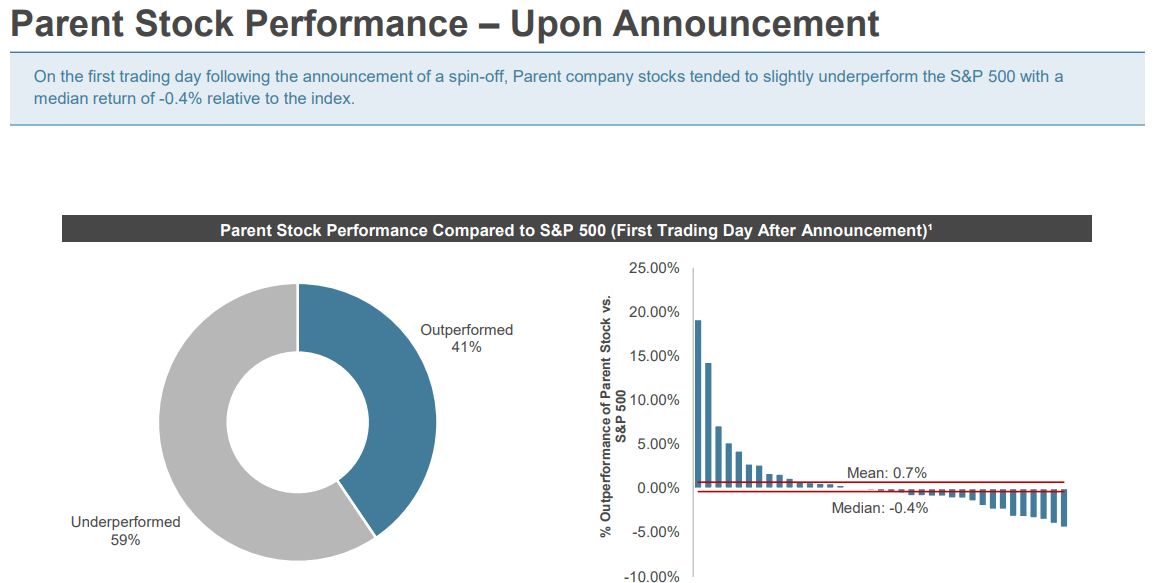

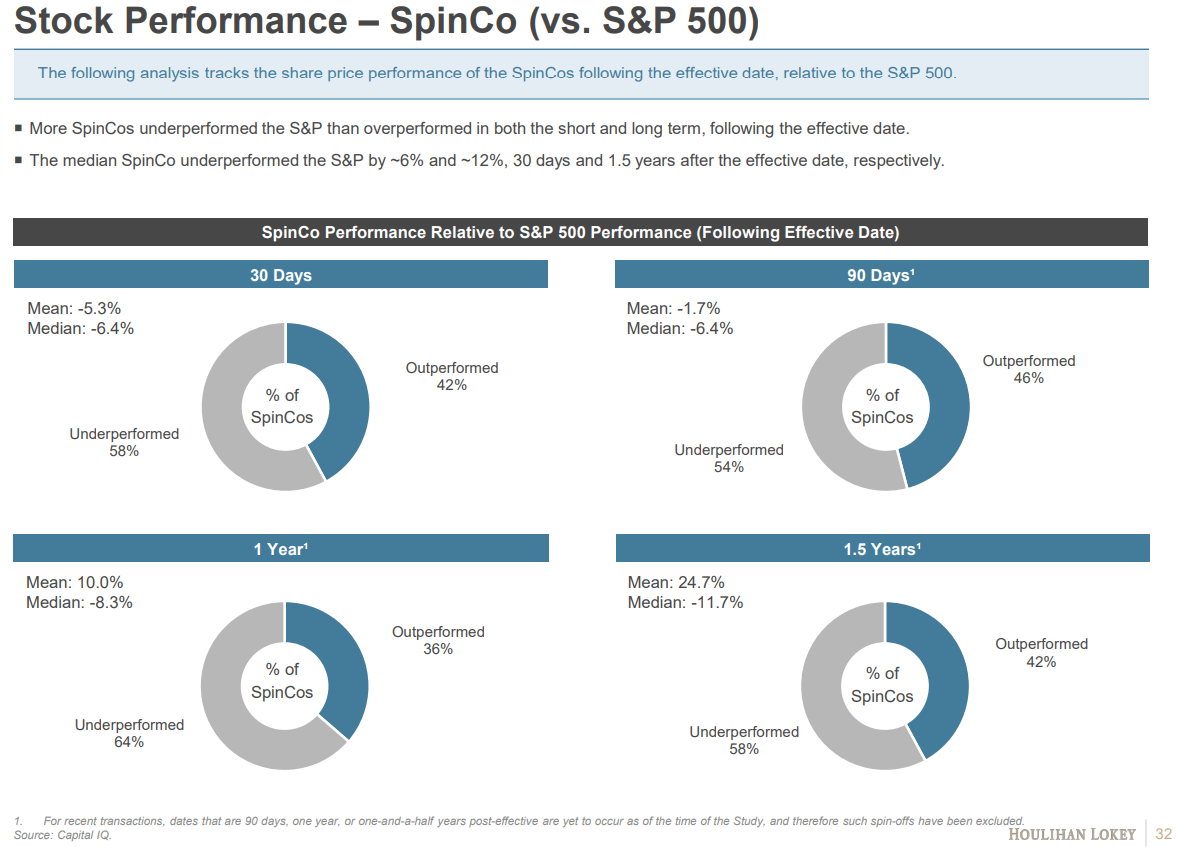

As proven within the two charts beneath, monetary efficiency earlier than and after a break up is blended. Due to this fact, we can’t conclude whether or not the announcement of a break up, and ensuing modifications to financials, are instantly associated to the announcement or a continuation of historic efficiency traits (relative to S&P 500). Nonetheless, what we are able to see is that the info does recommend that SpinCos do underperform after the break up happens.

With virtually two-thirds of SpinCos underperforming the S&P 500 at varied time intervals after the transaction, we have now extra proof that the SpinCos are weaker than the mother and father on common. The issue is, there’s nonetheless a large variance in efficiency, so an evaluation of every particular person transaction will seemingly show extra insightful than utilizing analytical information and averages.

HLI 2022 Spin-Off Transaction Research HLI 2022 Spin-Off Transaction Research

Latest Spin-offs Accomplished

There have been 5 main healthcare business spinoffs over the previous three years. Utilizing 20-20 hindsight imaginative and prescient, I’ll present fast summaries of the explanation why the gadgets have been bought off, and the way they’ve carried out since.

Merck (MRK) and Organon (OGN)

Merck has been dealing with detrimental progress for the reason that monetary disaster of the late 2000s till 2018. Nonetheless, the approval of blockbuster remedy Keytruda opened up the door to vital money flows. This was not sufficient, and the corporate determined to spin off non-core, older therapies into a brand new firm. As reliance on Keytruda elevated, administration has used the money from the spin-off to considerably enhance capex, M&A, and R&D. Whereas it would take a while for these results to change into mirrored within the financials as revenues, I really feel this was an instance of a useful spin off.

Organon shareholders have entry to an organization with a reasonably steady profile, primarily targeted on girls’s well being merchandise and biosimilars (the alternative transaction from AbbVie (ABBV) /Allergan). Whereas worthwhile, the largest challenge might be discovering progress whereas saddled with a market cap’s value of debt (~$9 billion). Was the debt a part of the subsidiary earlier than, or a part of Merck? Who is aware of, but it surely definitely limits OGN’s prospects within the intermediate time period (Merck’s debt has gone up for the reason that spin-off so maybe it has not been forcefully positioned upon OGN’s shoulders).

Danaher and Envista (NVST)

Danaher, a diversified medical machine and consumables producer spun-off their dental gear phase in 2019. Since then, NVST has returned 24% whereas DHR noticed a complete return of ~110%. DHR appears to have been the winner on this deal as financials are at a excessive level: earnings progress above 10% on common, debt discount, rising revenue margins, and extra. The identical cannot be stated with Envista as progress is gradual and debt is flat. Nonetheless, NVST is doing higher than Organon, and I anticipate this may proceed as the corporate figures their operations out.

Eli Lilly and Elanco (ELAN)

One other case of an underperforming SpinCo is with Elanco, the previous LLY veterinary science subsidiary. Whereas a pop in progress throughout the pandemic as pet homeowners elevated exponentially, evidently the fad is discontinuing and progress is now a difficulty. Following a number of downgrades, the corporate is now buying and selling 54% beneath the spin-off value approach again in mid 2018. Nonetheless, instances could also be altering once more as activist investor group Sachem Head took a stake. In the meantime, LLY continues to be the most effective performers in pharma due to their nonetheless diversified platform (and a few COVID remedy advantages). Watch that valuation although!

Pfizer (PFE) and Upjohn/Viatris (VTRS)

One of many more moderen and main spin-offs, Pfizer’s elimination of Upjohn continues to mirror the sample that the SpinCo has a excessive likelihood of underperforming. Mylan, the corporate Upjohn merged with, was already in a downward development, and the current sale of their joint biosimilars phase has precipitated shares to drop over 50% for the reason that 2020 merger. Controversy, particularly when appeared by means of the lens of a spin-off firm, at all times will result in detrimental sentiment.

On this case, sticking with Pfizer would have definitely been the higher possibility. Nonetheless, Pfizer has had its personal points with progress, and the spin-off did little to enhance the financials (outdoors of COVID advantages). Buyers should look beneath vaccination and COVID remedies to seek out future revenues, and in line with the share value (down 18% ytd whereas most pharma is up), are having hassle doing so.

McKesson (MCK) and Change Healthcare (CHNG)

Wish to lastly see an instance the place a SpinCo performs simply in addition to the mother or father firm? Look no additional than healthcare tech supplier Change Healthcare who was spun off from McKesson in mid 2019. Each corporations are up huge since then, with MCK capturing up 160% and CHNG up 70%. Apparently, CHNG’s upside has been restricted by the truth that they’re presently within the technique of being acquired by UnitedHealth (UNH), and if not so, I anticipate Change would have carried out much better.

I personally disagree with McKesson’s current bull run as efficiency is comparatively poor, however buyers definitely predict a turnaround. Change has its personal points, as progress has not fairly reached targets and appear to be plateauing already. Maybe the acquisition by UNH actually was the perfect consequence for buyers? Regardless, each corporations have achieved properly the previous three years in comparison with the SpinCos already coated. As such, we are able to see that there isn’t any actual predictive energy when anticipating a spin-off, however I’ll strive my greatest to evaluate the approaching transactions.

Coming Spinoffs and Splits

Johnson & Johnson Shopper

Johnson & Johnson is lastly parting methods with their shopper phase. Present progress is fueled by innovation in drug discovery, whereas legacy belongings are solely seeing lawsuits, competitors, and deteriorating margins. I see this break up as favorable, however will probably be necessary to evaluate the phrases rigorously.

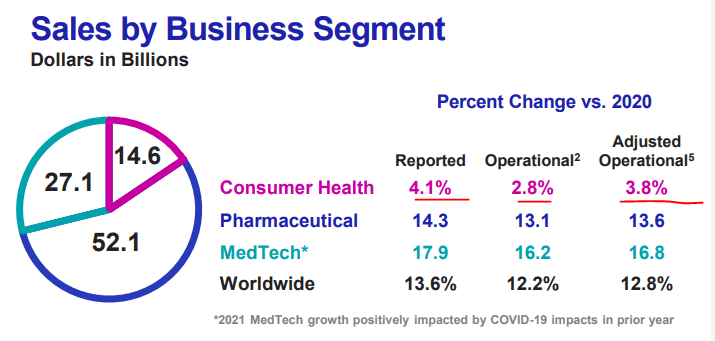

On one hand, earnings will develop considerably because the core JNJ firm focuses on novel medicines and medical gadgets. With a median progress fee as much as 4x that of the patron well being phase, progress may even be improved. If you’re pleased with JNJ’s present efficiency, then relaxation assured that it has almost all been the results of the prescribed drugs and MedTech, as shopper revenues are solely ~15% of the overall.

However, the normal merchandise that offered a margin of security, lots of which buyers have grown comfy with, and this will impression the corporate valuation. Each new corporations will definitely be far totally different than what it was previous to the break up. Nonetheless, I really feel assured that the core JNJ would be the superior asset and the elimination of lagging shopper well being merchandise will result in vital monetary enchancment. As this happens, the valuation will as soon as once more mirror the unbelievable place the core JNJ holds.

Due to this fact: Keep away from SpinCo, and look ahead to falling valuation of JNJ within the short-term.

JNJ Investor Presentation JNJ Investor Presentation

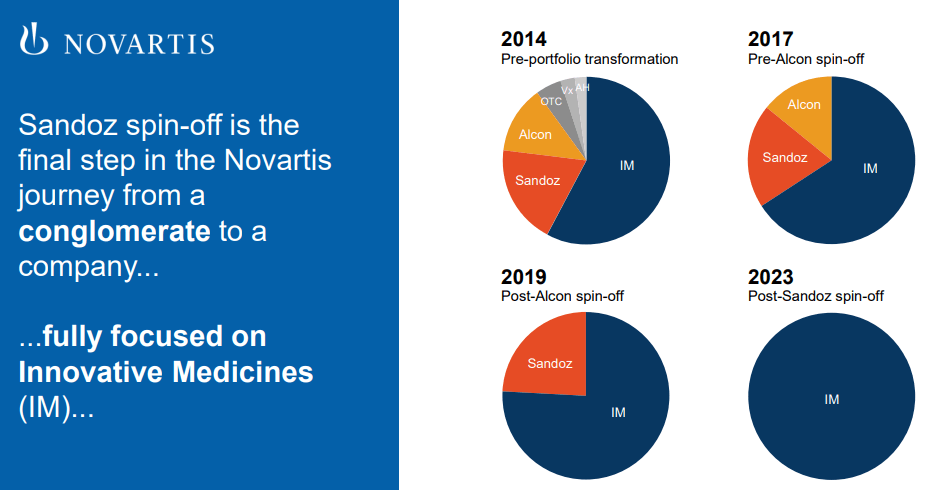

Novartis and Sandoz

Sandoz is Novartis’ giant generics and biosimilar medication producer, and it’s fairly clear that could be a sensible choice for the 2 entities to half methods. There’s little synergy between generics and novel drug growth, and so administration believes that operational effectivity will enhance throughout each corporations. For Novartis, this implies increased margins from revolutionary medication gross sales and continued reliance on R&D, whereas Sandoz could have a extra steady progress profile of decrease margin merchandise.

The spin-off is more likely to happen easily as Novartis has additionally not too long ago separated their Alcon (ALC) eye well being unit efficiently (a reasonably well-performing SpinCo). Over the previous three years, Novartis has seen vital earnings progress, and that is set to proceed after the subsequent spin-off they’ve deliberate. Sandoz is fascinating, as they are going to be one in all Europe’s largest generics producers and have pretty various progress alternatives due to biosimilars. Simply watch each corporations’ valuations and progress as Europe faces a number of headwinds (and NVS has had a number of lawsuits this summer season as properly).

Due to this fact: Novartis ought to see significant monetary enchancment and Sandoz could also be a worthwhile endeavor, nonetheless, I’d look ahead to short-term weak point to create a possibility.

Spin-off Investor Presentation

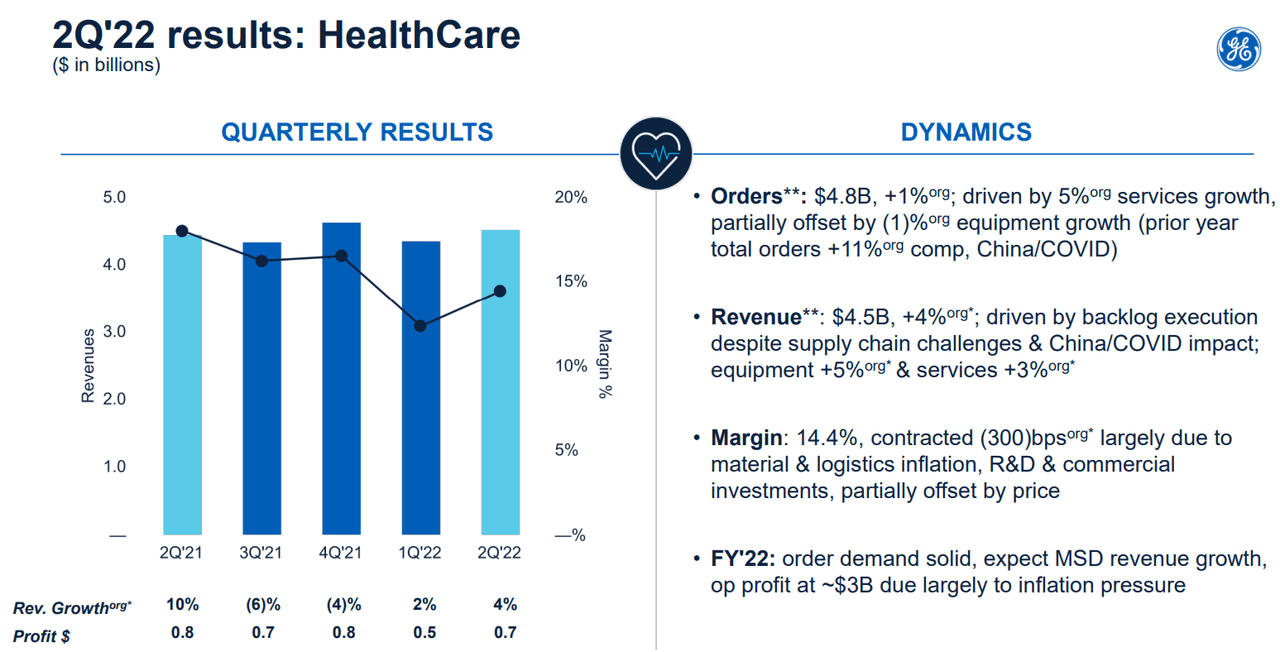

GE Well being Care Phase

GE has a storied historical past of R&D throughout many industries, together with Healthcare gear and consumables. As the corporate suffers progress points, administration determined it was greatest to separate into three complete corporations. The healthcare phase could have over $16 billion in revenues per 12 months, however progress is plateauing resulting from provide chain and different pandemic points. Additionally, like GE as a complete, margins are slowly falling with time, though the healthcare phase provides the very best margins of the group. I imagine enhancements are doable upon the conclusion of the transaction.

Due to this fact: GE Healthcare could be thought of by itself as a steady play on healthcare gear and know-how, however solely as soon as buying and selling alone.

2Q22 Investor Presentation

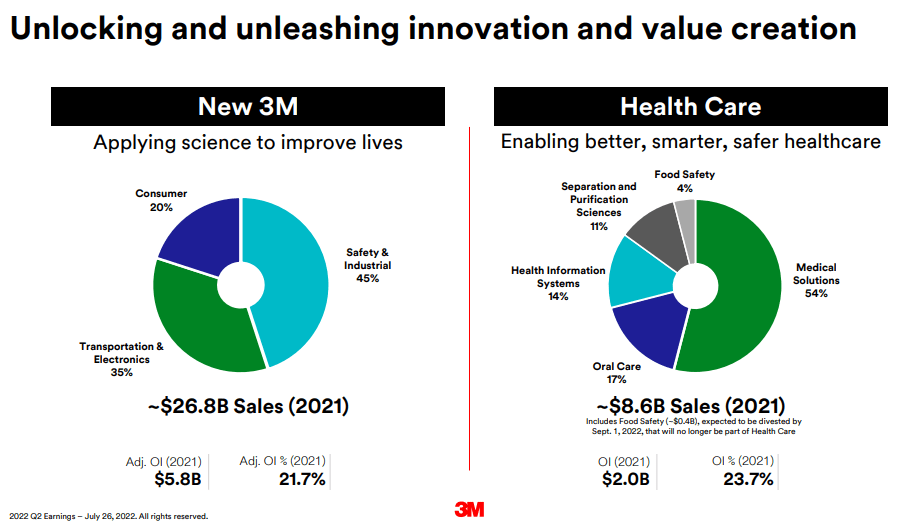

3M and their Well being Care Phase

3M, a reputation to keep away from in my eyes, is trying to restart their progress by spinning off their healthcare unit. At roughly one fourth of whole revenues, the influx of money to 3M will have to be reallocated considerably if the corporate needs to keep up their dividend. Additionally, I miss out on the advantages of the spin-off, apart from the truth that the HC unit might earn a excessive valuation at time of sale. The phase is performing properly by means of time, and even is in an upward development as COVID subsides and elective procedures return.

Regardless, MMM is shifting ahead with this transaction, and I discover the Well being Care unit is worthy of additional consideration. 3M doesn’t have vital quantities of debt, and I don’t worry in regards to the SpinCo being held down by pointless leverage. Nonetheless, it’s unknown whether or not litigation will comply with the SpinCo, as some lawsuits have demanded that the spin-off doesn’t happen. If issues go south, watch 3M’s value to fall as progress is minimize 25%, income damage as a excessive margin phase is eliminated, and the dividend heads to the chopping block.

Due to this fact: I’d keep away from each 3M and the SpinCo in the meanwhile.

3M Investor Presentation

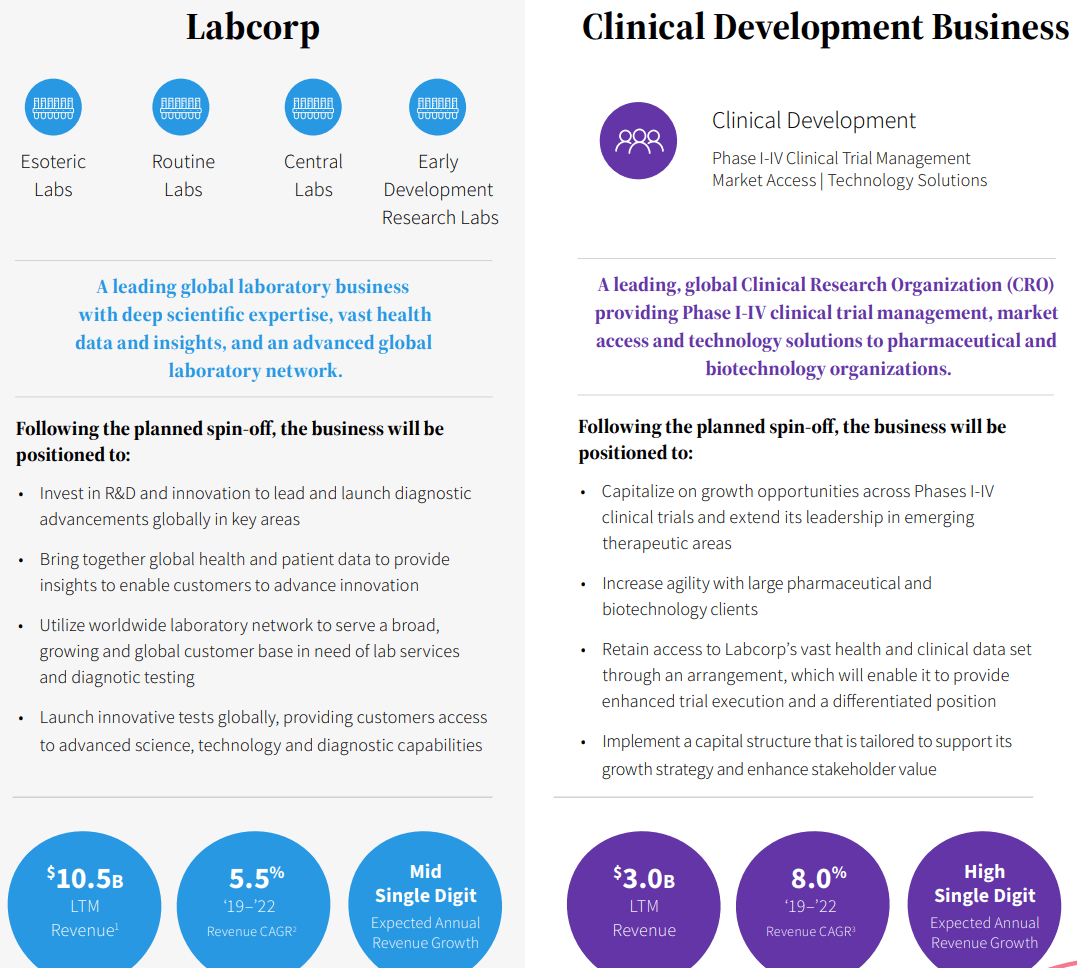

Labcorp’s Medical Growth Enterprise

Labcorp is lastly exiting scientific analysis (aiding drug builders with their scientific trials) and focusing fully on lab work. This comes lower than a decade after Labcorp acquired scientific analysis group Covance for over $5 billion in 2014. That is one other fascinating spin-off that appears to be eradicating the stronger phase, slightly than eradicating a lagging asset. Whereas laboratory evaluation and operation usually are not much like a CRO, I battle to see how a joint firm can’t succeed.

When it comes to the SpinCo, monetary efficiency might be anticipated to be higher as progress is nearer to 10% than 5% with the legacy enterprise. Whereas administration could also be attributing poor earnings efficiency from 2014 to 2020 on the scientific growth enterprise, I’ll proceed to imagine that low-margin lab work will not be an attractive enterprise. Additionally, the CRO might be dealing with stiff competitors from Thermo Fisher (TMO), IQVIA (IQV), ICON (ICLR), and Syneos Well being (SYNH). Being tossed again in with the sharks might proceed to inhibit efficiency of the SpinCo.

Due to this fact: I anticipated joint synergies to result in sturdy efficiency, and splitting doesn’t enable for that to happen. On their very own, each are weak.

Labcorp Web site

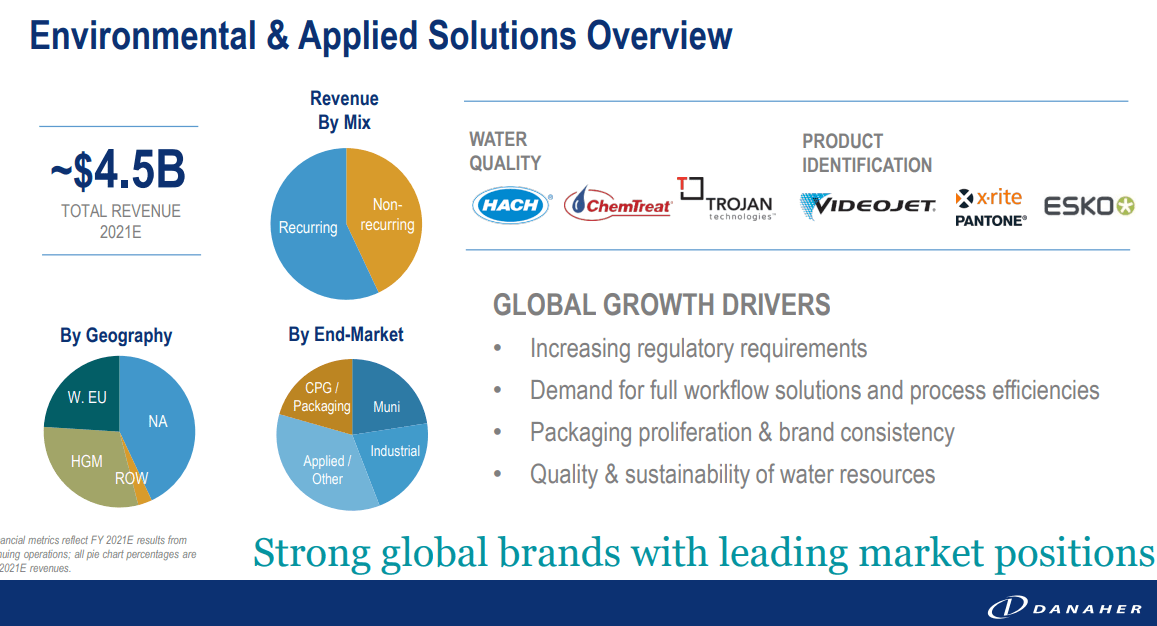

Danaher’s Environmental & Utilized Options Phase

Danaher is lastly taking their focus fully on human well being. With the spin-off of their water high quality and product identification companies (for now known as EAS), DHR will lose roughly $4.7 billion in revenues, or barely greater than 15% of whole revenues (FY21). Much like a pharmaceutical parting methods with their generic or shopper segments, I really feel this spin-off could have a web constructive impact on Danaher as their concentrate on core segments. Margins may even enhance because the EAS phase 20-25% working margins against 25-35% for diagnostics and life sciences segments.

Nonetheless, the EAS SpinCo might be a pressure in their very own proper with multi-billion in revenues and earnings per 12 months, a various vary of subsidiaries, and a number of progress catalysts. As a fan of Danaher on a standard day, I’m viewing this transaction as constructive, however I might be scrutinizing the approaching monetary information. I’ll at all times be a proponent of various companies slightly than targeted ones, however DHR is aware of carry out properly, and I ought to have some religion.

Due to this fact: DHR is a purchase as SpinCo is more likely to be the perfect performing asset of all upcoming SpinCos, and DHR ought to be capable of proceed their upward development in each income and earnings progress.

DHR 2021 Annual Presentation

Conclusion

Whereas the previous 5 years noticed a number of spinoffs of lagging and underperforming belongings, the approaching wave is sort of totally different. As an alternative, we see that just a few underperforming giants wish to discover progress catalysts by spinning off their stronger belongings and utilizing the excessive worth money inflows to fund their final dying breath. As such, I look bearishly on many of the mother or father corporations, however every SpinCo could also be thought of on their very own.

This goes towards the info discovered by Houlihan Lokey who observed the overall sample is that the SpinCos are inclined to underperform the mother or father corporations, and this information is beneficial in sustaining lifelike expectations. Variance is excessive, however I imagine it’s best to not be too enthusiastic about any SpinOff. Because the market stays in a downtrend I’d advocate ready for information to fill in and reassess every transaction rigorously. In truth, if you don’t maintain any of the above corporations, as I do not, I’d advocate staying on the sidelines for now. If fascinating information factors come up, I’ll remember to comply with up, however for now, take your time to do your homework.

Thanks for studying. Be happy to share your ideas beneath.

{kind=link}