By Lindsay Weekes

on April 13, 2022

Tax day: a time that strikes each concern and hope within the hearts of so many. Most individuals pray for a refund, however is that truly one thing you must need? Whereas it might probably really feel good to get an enormous chunk of change within the mail, constantly getting a refund yr after yr can really harm your funds. Maintain studying to seek out out why you don’t need a tax refund.

Give it some thought. This isn’t “free cash,” it’s YOUR cash! You loaned it to the U.S. authorities all year long, and it’s simply now coming again to you. The federal government took out a mortgage out of your paycheck, and are available tax day, it will get to pay that again interest-free! You’d by no means maintain your cash in a financial institution that supplied 0% curiosity, proper? And but right here you’re.

In line with the IRS, the common 2018 tax refund was $1,865, which works out to overpaying your taxes by about $155 per thirty days. What might you do with that further $155? Pay somewhat further in the direction of your debt? Make investments? Keep away from pulling from financial savings or utilizing a bank card for surprising bills? Let’s be sincere: many individuals use their tax refunds (and different massive windfalls) as an excuse to purchase issues they don’t want. And even for those who use MOST of it responsibly, you’re nonetheless shedding out on some critical money.

How a lot cash are you shedding, precisely? That is determined by what you would have been utilizing it for for those who’d by no means provided that mortgage to Uncle Sam.

Listed below are two examples of issues you would do with that further month-to-month money that will prevent in the long term.

Save on curiosity by paying down your bank card

Let’s say you owe $3,000 and you’ve got a 15% APR. Should you often pay $100 per thirty days, you will find yourself owing $3,784 (that’s 21% curiosity) and it’ll take you three years and two months to pay that debt. However, for those who might enhance your month-to-month cost with the $260 you’re at the moment paying in taxes, you’d solely pay $3,188 (solely 6% curiosity) and you’ll have the ability to repay the cardboard in 9 months! Even for those who used your return to repay the bank card, you’ll nonetheless be overpaying curiosity to the tune of just about $600.

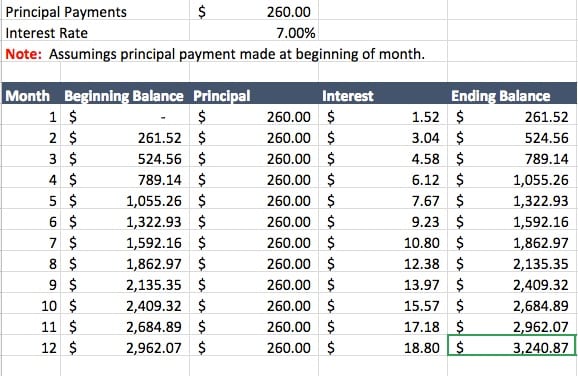

Begin (or add to) a retirement account and reap the compound curiosity

Some individuals put their return right into a retirement account, however doing so could make you lose out on a yr’s price of curiosity. Should you begin a retirement fund with a 7% return and put in that $260 per thirty days, on the finish of the yr you’ll have $3,240.87, a full $120 greater than you’d get for those who simply put in your $3,120 in without delay. And that’s solely yr one! It will get compounded yr after yr:

So, how can I cease getting such an enormous refund?

To be able to reap the benefits of these sorts of financial savings, you’ll must fill out a brand new W-4. That is the shape your employer makes use of to determine how a lot tax to withhold out of your paycheck. This consists of your marital standing, and any dependents you’re financially accountable for, and it provides workers the power so as to add an extra quantity they want to withhold. Ask your employer for a brand new kind and fill it out. You’ll want to determine how a lot to withhold, so use this IRS Withholding Calculator to determine it out. You’ll want final yr’s tax return and your final pay stub to start out. That is additionally a great time to ensure you are submitting accurately. Not too long ago married? New Child? Make sure that your tax kinds mirror your life adjustments. (Additionally: If you find yourself having to pay IN on tax day, remember to try our roundup of the most effective bank cards for taxes!)

To reiterate, this solely works if you’re going to use the cash to save lots of. Should you aren’t going to make use of the cash each month to spend money on your future, take the lump sum in April. And it’s in all probability not well worth the problem in case you are solely getting just a few hundred {dollars} again, however in case you are anticipating the common or extra, this might enable you to construct your monetary future somewhat sooner.

Would your moderately get your tax refund month to month? Tell us within the feedback!

{kind=link}