Juanmonino/iStock Unreleased by way of Getty Photographs

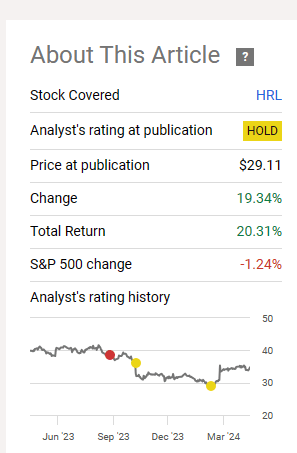

In our final replace for Hormel Meals Company (NYSE:HRL), we steered that the bears had been pushing deep into oversold territory and dangers for a countertrend transfer had been excessive. We anticipated a bounce, one which ought to reset sentiment and put together the inventory for the subsequent huge transfer decrease. Particularly, we mentioned:

Markets seldom transfer in a straight line although the final 15 weeks within the SPY appear to recommend in any other case. HRL’s drop has been fairly excessive for a shopper staples firm and whereas there are headwinds, the sentiment appears to be like extraordinarily one-sided. Relative to its 200 day shifting common, HRL was solely decrease on a handful of events. The setup appears to be like good for a bounce that clears away the surplus pessimism.

Supply: “Peak Pessimism, Purchase For A Commerce And Then Hit The Fade.”

That labored effectively, and HRL outperformed the S&P 500 (SP500) by over 20% in two and half months.

Looking for Alpha

We now offer you three the explanation why it is advisable refocus on the longer-term story and exit the worthwhile play.

1) Lofty Valuation

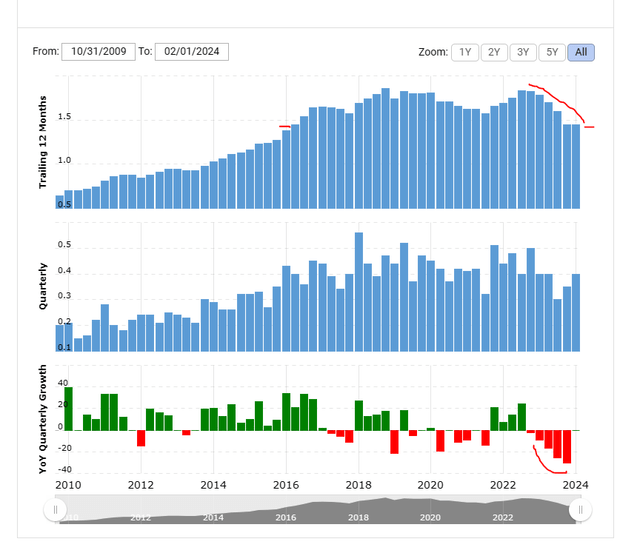

Even for those who imagine the estimates on the market, HRL is buying and selling far too costly for an period of 5% rates of interest. At 22X earnings for this yr, it’s important to be an actual believer in SPAM. As the image beneath reveals, even these earnings are literally contracting from the yr prior.

Looking for Alpha

Not solely are these contracting, however stay effectively beneath ranges since in lots of earlier years. The chart beneath reveals the trailing four-quarter figures and offers a way of how unhealthy the deterioration has been.

Macro Developments

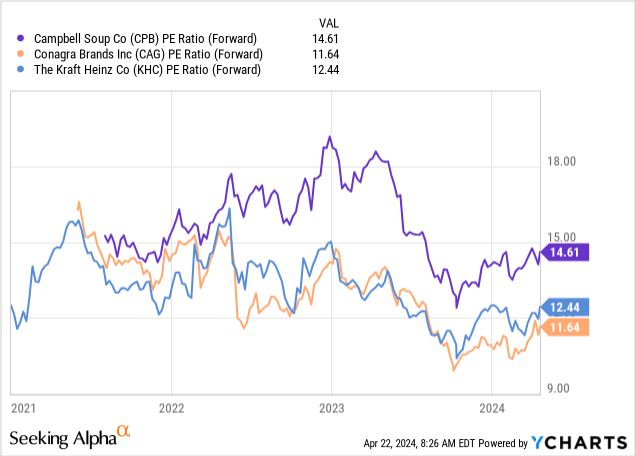

The utmost you need to pay for a enterprise like that is about 15X earnings. In case you assume that’s too pessimistic, listed here are three examples of shopper staples shares which have accomplished a greater job than HRL, all buying and selling underneath what we simply steered.

15X the $1.60 will get you to $24.00. 15X the 2025 estimate of a $1.69 will get you $25.35. We do not assume the earnings estimates are overly optimistic right here, so we can’t deduct factors for that. However the valuation path stays firmly decrease.

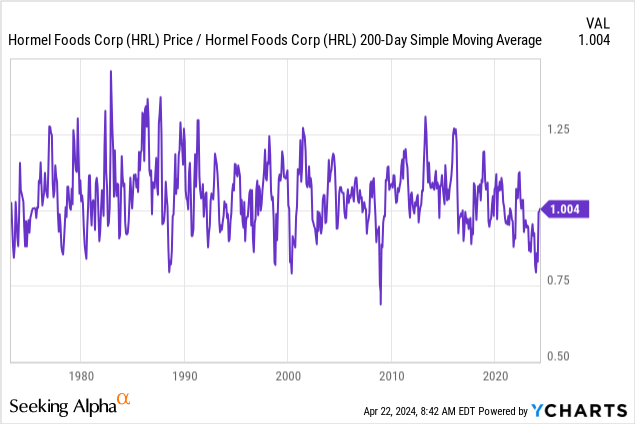

2) Oversold Circumstances Relieved

In our final protection, we had pointed to the 200-day shifting and the truth that HRL was 20% beneath it, as a key motive to dial again the bearishness.

We at the moment are grazing that 200-day shifting common as soon as extra, and that is the purpose the place we count on the dominant pattern to reassert itself.

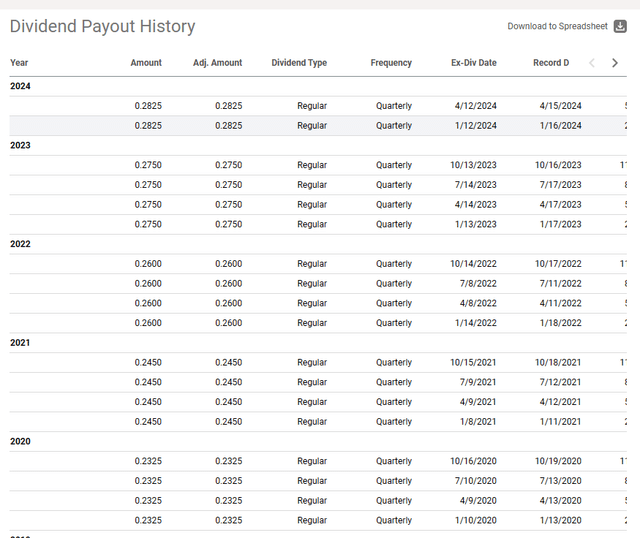

3) Dividend Progress Story Possible To Gradual Down Significantly

HRL placed on a courageous face and hiked its dividend as soon as for 2024.

Looking for Alpha

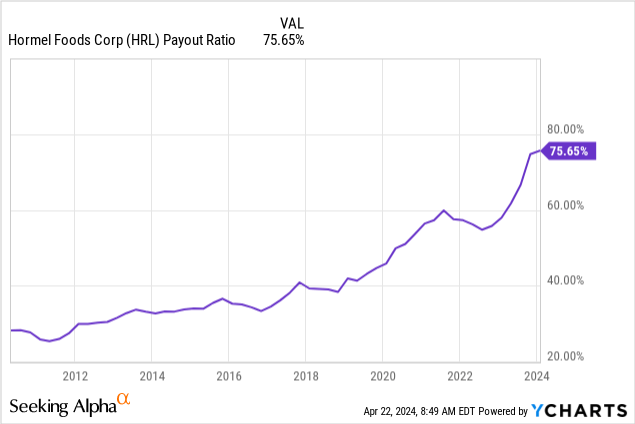

The payout ratio is now prone to be round 70%-75% (relying on the way you calculate it). That is prone to be at or above the consolation zone for administration. The majority of the dividend progress story was pushed by an increasing payout ratio. This ratio went from 25% to 75% over the 13 years.

For sure, no one is silly sufficient to imagine that we will go from 75% to 225% over the past 13 years. This increasing payout ratio impression has been most notable since 2016. Throughout this time, earnings have been flat (sure, over 8 years) and dividends have roughly doubled. From this level on, the dividend is prone to develop by 3% at finest, and a freeze shouldn’t be out of the query.

Verdict

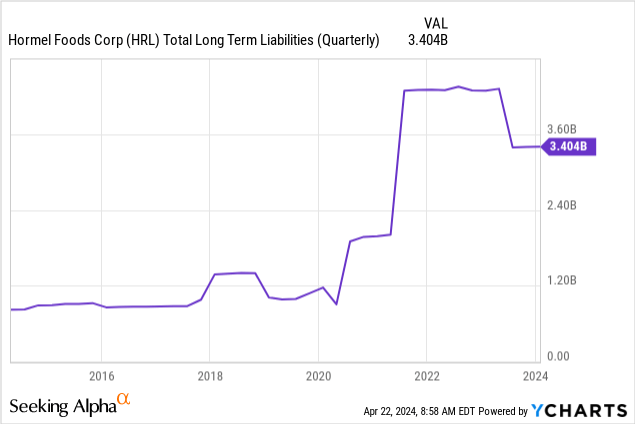

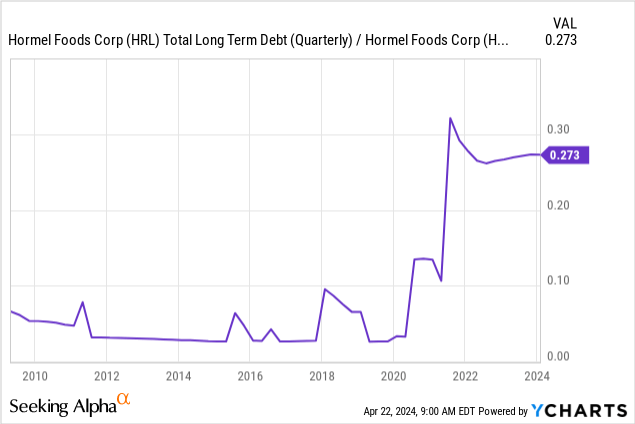

HRL has used up all its key playing cards. The Planters acquisition is within the bag, and earnings look worse than they had been earlier than that. The steadiness sheet, which was the most effective within the enterprise, has now moved to only barely above common.

One different technique to visualize that is to see the debt in relation to gross sales.

S&P (which downgraded Hormel in 2023 from A to A-) continues to be optimistic that the corporate can maintain underneath 2.0X debt to EBITDA.

Leverage will stay modestly elevated in fiscal 2024. Hormel’s EBITDA (S&P World Scores-adjusted) declined about 10% in fiscal 2023 (ended Oct. 29) on account of a mix of things, together with commodity turkey market volatility, rising shopper value elasticity, weak spot in China, and fixed-cost under-absorption. Because of the revenue decline and the corporate’s $400 million funding in Garudafood in December 2022, leverage has been sustained within the high-1.0x space over the previous yr (in contrast with 1.5x on the finish of fiscal 2022). Though first-quarter fiscal 2024 efficiency exceeded our expectations, supported by stronger-than-expected volumes and decrease logistics bills, we count on profitability will stay pressured in fiscal 2024 on account of still-weak commodity turkey costs, elevated model funding, and prices related to the corporate’s transformation and modernization program. Consequently, we now count on leverage will likely be sustained at about 1.8x in fiscal 2024 (in contrast with our earlier expectation that the corporate would deleverage to about 1.5x). However, we proceed to imagine Hormel will generate good free working money circulate (FOCF) that can exceed shareholder returns and help deleveraging over the long run.

Supply: S&P

This lack of cushion additionally means these payout bumps are going to require a microscope to see.

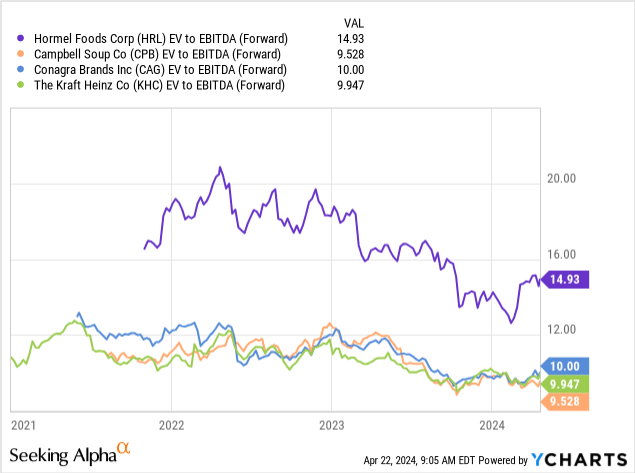

You might argue for a premium a number of for HRL prior to now as a result of it used so little debt within the 2012-2021 period relative to Conagra Manufacturers, Inc. (CAG), Campbell Soup Firm (CPB), and The Kraft Heinz Firm (KHC). That has modified. Whereas it nonetheless makes use of much less debt, the relative benefit right here is crumbling. Regardless of that smaller benefit, HRL nonetheless trades 5 multiples vast on ahead EV to EBITDA. That’s insanely excessive and provides huge dangers to the draw back.

We’d look decrease for this one over the subsequent 12 months, particularly as buyers come to grips once more with “greater for longer.”

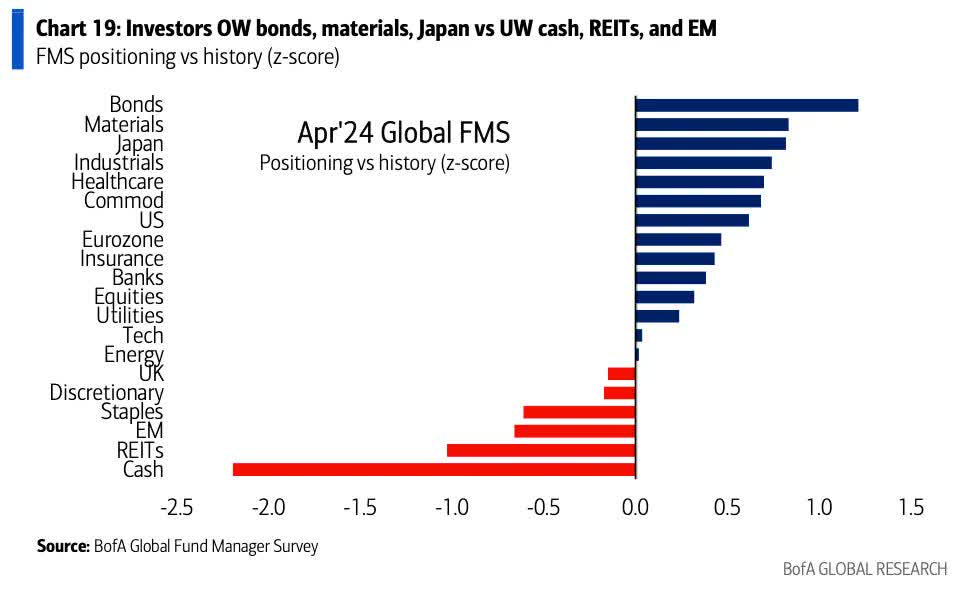

As we shut off right here, one risk holds that HRL might shock on the upside, not less than over the subsequent 3-6 months earlier than the wheels come off. In our expertise, main market tops are inclined to kind with defensive sectors like utilities and staples main the cost. The positioning in staples, specifically, can also be conducive for a bounce.

BofA

This might extend the transition right down to honest worth a bit bit longer. We’d nonetheless keep away from Hormel Meals Company inventory, and if we get $37-$39, we might look to ascertain a brief place.

Please word that this isn’t monetary recommendation. It might seem to be it, sound prefer it, however surprisingly, it’s not. Buyers are anticipated to do their very own due diligence and seek the advice of knowledgeable who is aware of their aims and constraints.

{kind=link}