A number of hospital telehealth distributors loved nice success in 2020 as they benefitted from unprecedented demand for his or her IT and providers through the pandemic. However as lockdown restrictions had been lifted and the pressure on hospitals’ in-house capability throughout the ICU and different acute care wards eased into the second half of 2021, had been the distributors in a position to preserve their development? With full-year outcomes from a number of of the main hospital telehealth distributors now printed, right here’s our tackle the lately introduced monetary and enterprise developments for these distributors.

Amwell

Amwell has established itself as one of many main telehealth suppliers globally. Because the telehealth market matures in the direction of enterprise-scale demand, it’s important that suppliers to the market evolve their choices to deal with this, and Amwell has finished this nicely through product growth and acquisition. Since its strategic acquisition of Avizia in 2018, Amwell’s quickly expanded its buyer base to suppliers utilizing telehealth for inpatient and digital clinic purposes. Amwell’s most up-to-date acquisitions (July 2021) embrace SilverCloud Well being, a digital psychological well being platform supplier, and Conversa Well being, a supplier of automated digital healthcare. By integrating these latest additions onto Amwell’s platform, the seller shall be higher positioned to boost its personal behavioral well being providing and scale its providers throughout completely different settings.

Amwell’s platform helps each telehealth consultations supplied by its personal physicians and people supplied by its supplier clients instantly. The Avizia acquisition introduced with it the Avizia One platform, focused extra at provider-to-provider telehealth, into its portfolio alongside buyer endpoints reminiscent of its “Carepoint” carts and peripherals. The above platforms had been outdated in April 2021 with the launch of Amwell’s Converge platform, making certain a single interface and in depth third-party vendor integration. Additional, the Amwell Change permits its companions and clients to attach as a way to present further assist providers. The mixing of Avizia into its legacy platform signifies that its in a position to provide suppliers a whole enterprise-scale platform that can be utilized to deal with practically all of the potential telehealth wants of a supplier. As of December 2021, 53 of its shoppers had deployed Converge, and the intention is to ramp up adoption in Q3 2022 to transition all current shoppers by the primary half of 2023.

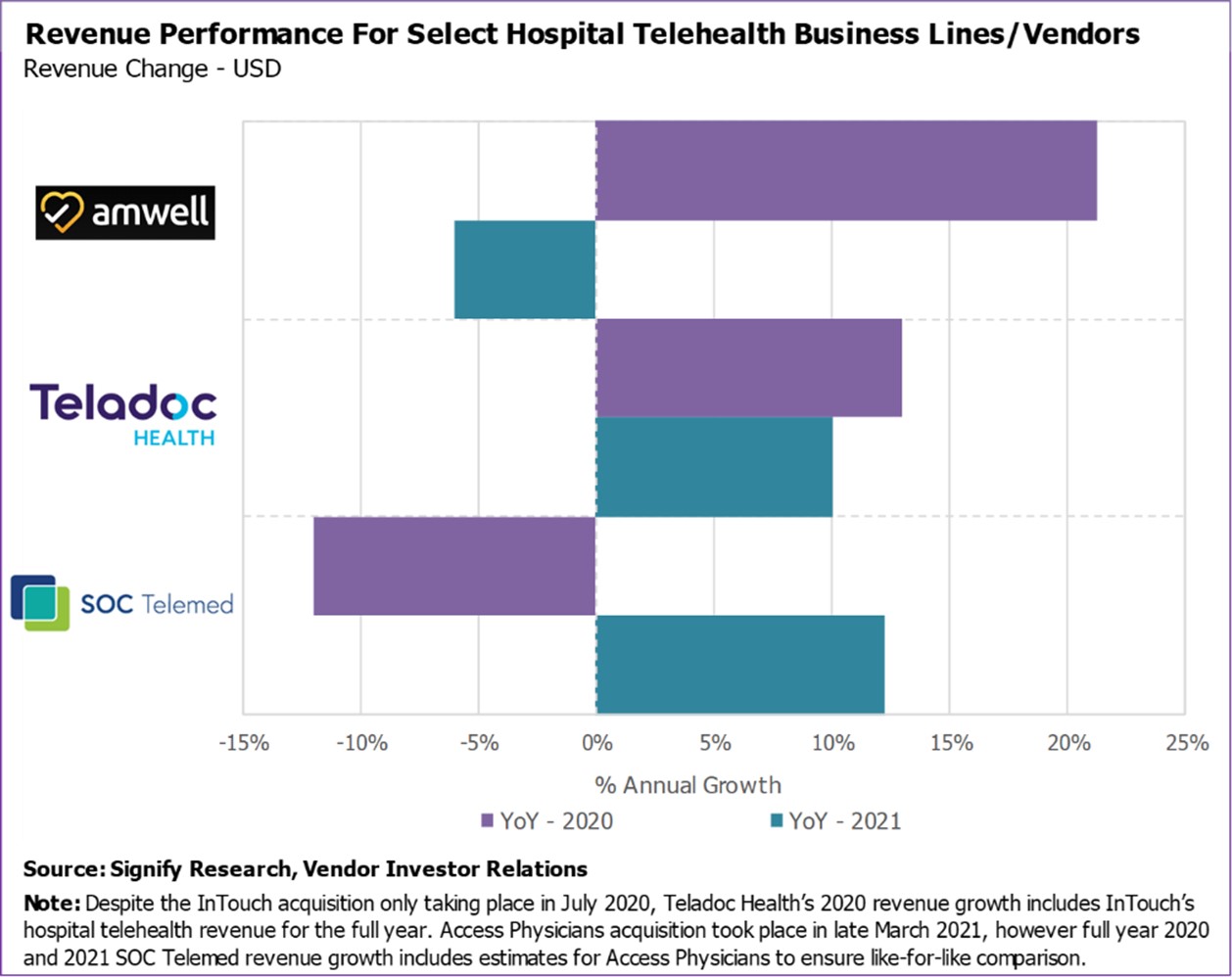

Diving into Amwell’s financials, the seller reported development in its general telehealth enterprise income of 65% in 2020 to USD $245m, though its 2021 revenues had largely flattened (+3%, USD $253m). To some extent, the dearth of development in its hospital telehealth enterprise in 2021 displays the efficiency of the general enterprise. Its Carepoint enterprise, which incorporates revenues for its {hardware} and providers to assist provider-to-provider hospital telehealth consultations, rose by 21% to $USD 29.7m in 2020, pushed by the elevated gross sales quantity of its {hardware} and consultations to assist suppliers through the pandemic. Nevertheless, it was unable to keep up development throughout 2021 as revenues fell by 6% and consultations dropped to an estimated 1.1m volumes. While a return to the annual development fee achieved throughout 2020 is unlikely, it’s anticipated that the Carepoint and providers enterprise, which represents roughly 10% of its general firm revenues, will proceed to witness the expansion and characterize a comparatively steady proportion of Amwell’s enterprise.

Teladoc Well being

US-based Teladoc Well being is a number one enterprise-scale supplier of options throughout all telehealth settings. Through a number of acquisitions, it has expanded by way of merchandise supplied and the vertical markets focused. The USD $600m InTouch Well being deal in July 2020 created a market-leading firm with an providing that spanned most areas of telehealth, and likewise expanded Teladoc’s worldwide footprint considerably. The lacking piece in Teladoc’s portfolio was Distant Affected person Monitoring (RPM), one thing it addressed with arguably its most vital deal to this point, the USD $13.9bn acquisition of Livongo Well being in October 2020. It’s considered one of c. 50 distributors are profiled in Signify Analysis’s new devoted report on the RPM – World – 2022 market publishing this month.

In relation to hospital telehealth particularly, the InTouch acquisition has enabled Teladoc to construct on the success the previous achieved in serving US well being methods in inpatient purposes, notably within the areas of emergent consultations (Scientific Examinations/Medical Assist) and ongoing affected person administration (Tele-ICU/Scientific Surveillance). Regardless of the InTouch acquisition solely going down in July 2020, Teladoc Well being’s 2020 income and consultations in Signify Analysis’s evaluation under embrace InTouch’s hospital telehealth income for the complete yr.

Throughout the hospital telehealth setting, Teladoc was the world’s main supplier of Scientific Examinations and Medical Assist IT ({hardware}, platform, IT providers) in 2021 with an estimated income of c. USD $100m, up by round 10% versus 2020. It was additionally the biggest supplier of consultations, with 4.1m volumes reported in 2021, up by 4.2%. The slowdown in development, illustrated in its quarterly platform enabled periods (consultations) throughout 2021 was anticipated and proved laborious to match, because of the robust comparable quarters within the earlier yr. Nevertheless, as highlighted within the first graphic earlier on this perception, Teladoc was the one vendor to attain income development in consecutive years. Because the impact of the pandemic fades additional into 2022, Teladoc is nicely positioned to construct on its main market place and can really feel assured in sustainable development.

SOC Telemed

The Doctor Assist Companies phase of Signify Analysis’s Hospital Telehealth evaluation is led by SOC Telemed. The seller had its origins in offering providers addressing telehealth necessities in neurology. Nevertheless, development lately has accelerated through M&A exercise, beginning in August 2018 with the acquisition of JSA Well being, a supplier of behavioral well being telehealth providers. SOC’s M&A technique picked up tempo through the pandemic, initially in October 2020 with the completion of its merger with Healthcare Merger Corp, permitting SOC to start buying and selling as a public firm.

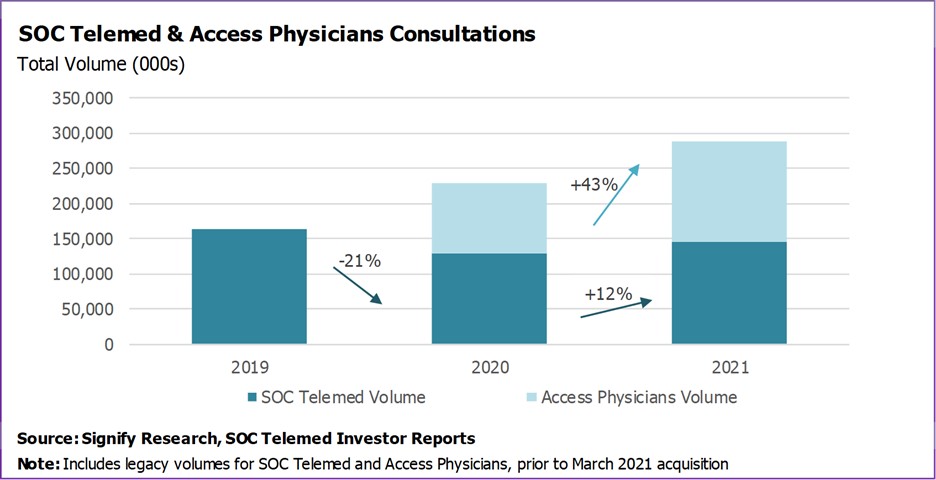

SOC enhanced its place as a number one supplier of hospital telehealth with the acquisition of Entry Physicians in March 2021, diversifying its service line providing from emergency to inpatient with the addition of seven service traces together with cardiology, infectious illness, maternal-fetal drugs, nephrology, and endocrinology, and trebling the scale of its worker community to 750+. The acquisition solidifies SOC’s standing as the biggest devoted acute telehealth doctor assist service supplier within the US.

Many main hospital telehealth distributors reported constructive financials in relation to their hospital telehealth enterprise in 2020, nevertheless, SOC Telemed was one of many main anomalies as a consequence of its heavy reliance on producing revenues from its core enterprise of doctor assist providers (surgical/medical consultations represented 98% of SOC’s general income in 2019 – USD $66m). This suffered lowered utilization throughout 2020; session volumes fell by 21% and SOC’s general revenues dropped by 12% to USD $58m. Nevertheless, it did expertise rising demand for its Telemed IQ platform-only enterprise through the pandemic, which doubled in absolute revenues to USD $2m in 2020, albeit from a small base.

Acquisition fuels the rebound

While 2021 noticed a return to development in SOC’s legacy consults (145,000, up by 12% Y-o-Y), this was nonetheless shy of pre-pandemic volumes (163,000 in 2019). Nevertheless, factoring in consults contributed by Entry Physicians, it generated a further 110,000 volumes in 2021 (26th March -31st December), bringing the overall determine to 255,000 for the reason that acquisition. SOC’s legacy annual 2021 income (USD $65m) was additionally simply in need of its pre-pandemic degree, though as soon as extra the Entry Physicians contribution (nearly one-third of further income) propelled the overall determine to $94m (+63% Y-o-Y, though +12% adjusted to incorporate like-for-like comparability).

Diving deeper into the financials, nearly $100 was trimmed off the general enterprise’ 2021 income per seek the advice of ($333) in comparison with SOC’s legacy 2020 determine ($430). Entry Physicians traditionally generated a a lot decrease determine as a consequence of its large service line combine and large variation between the period of every seek the advice of, so it’s no enormous shock that SOC’s new, broader portfolio and technique pursuing cross-selling of providers and new income streams resulted in a trade-off with its 2021 income per seek the advice of.

Valuation Reset

It’s value noting that SOC’s market valuation has suffered important turbulence since its October 2020 IPO (valuing the seller at USD $720m); in early February 2022, its worth had plummeted by 90%. Additional, the general public itemizing lasted simply 18 months as SOC was acquired by Affected person Sq. Capital in an all-cash transaction final month (April 2022), valuing the enterprise at USD $304m. Nevertheless, SOC’s not alone in experiencing a plunge since its preliminary IPO valuation; Teladoc and Amwell are simply another high-profile examples of digital well being distributors experiencing a placing distinction in fortunes between the start of 2021 and 2022. Excessive values pushed by sturdy revenues through the top of the pandemic have been offset by components reminiscent of fixed losses and missed targets. Additional, exterior of the distributors’ management are enormous world financial uncertainties attributable to rate of interest hikes – notably problematic for Teladoc and Amwell as they continue to be unprofitable and can doubtless face elevated borrowing prices – and Russia’s assault on Ukraine, badly damaging investor sentiment and contributing in the direction of a mass-market sell-off in latest months.

Market Optimism Stays

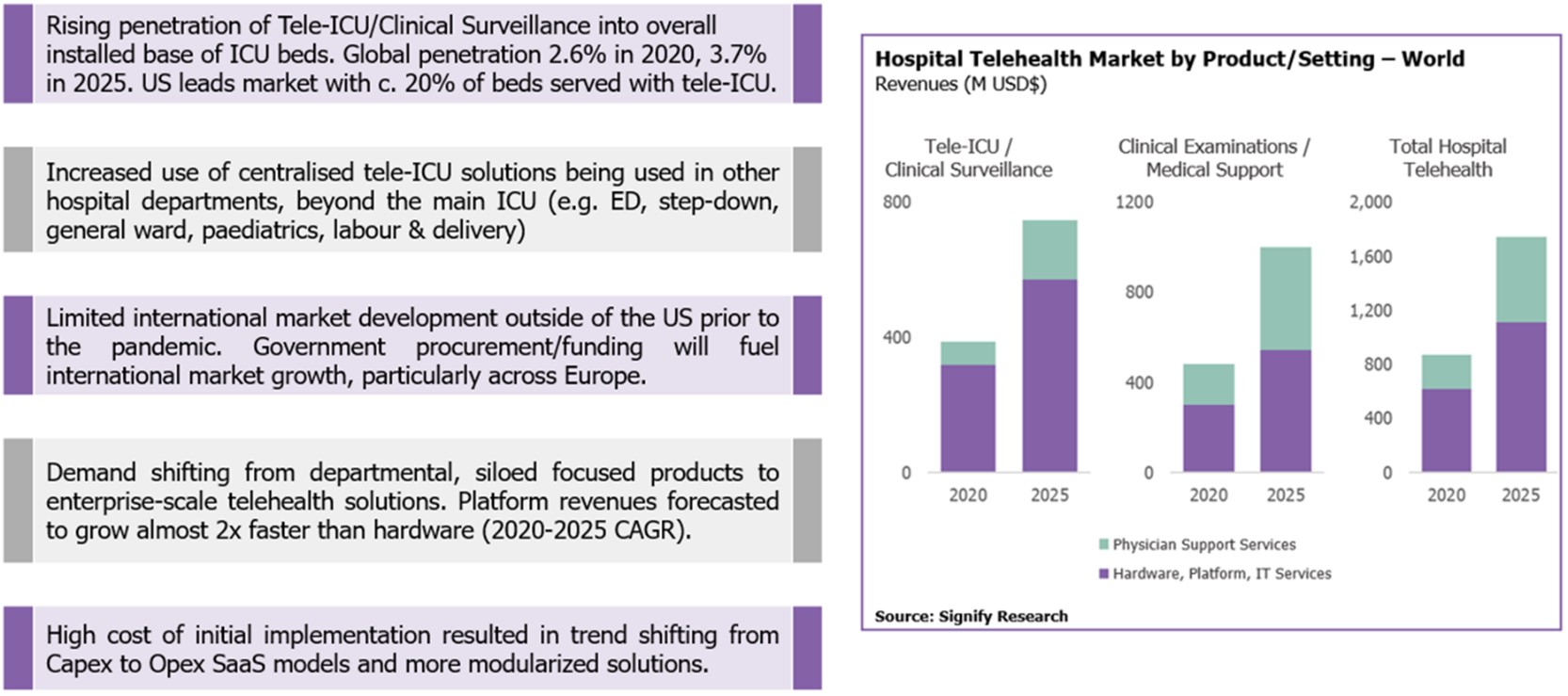

Nonetheless, with a 2020-2025 CAGR of 14% and 16% respectively projected throughout the Tele-ICU/Scientific Surveillance and Scientific Examinations/Medical Assist market revenues, the outlook seems to be promising. There are a lot of causes for distributors to stay optimistic in relation to the hospital telehealth market growth, as beforehand highlighted in a complimentary pattern of the Hospital Telehealth – World – 2022 report, and summarised under.

About Arun Gill, Senior Analyst at Signify View

Arun Gil is a Senior Market Analyst at Signify Analysis, a UK-based market analysis agency specializing in well being IT, digital well being, and medical imaging. Arun joined Signify Analysis in 2019 as a part of the Digital Well being workforce specializing in EHR/EMR, built-in care expertise, and telehealth. He brings with him 10 years expertise as a Senior Market Analyst overlaying the buyer tech and imaging trade with Futuresource Consulting and NetGrowth Consultants.

{kind=link}