JamesYetMingAu-Images/iStock Editorial by way of Getty Photos

After falling almost 50% for the reason that begin of the yr, Howard Hughes (NYSE:HHC) shares have bounced 15% because it was introduced that Invoice Ackman’s Pershing Sq. would tender for one more 12.7% of the shares at $60. Ought to the tender succeed, this is able to convey Pershing’s curiosity in HHC to 40%. Many buyers are questioning whether or not they need to comply with Ackman’s lead and provoke or enhance their stake in HHC shares.

Whereas I perceive the deserves of the bull case (recapped beneath), I do not need confidence that this time is completely different – HHC share have traded at a big low cost to theoretical NAV for years and I lack conviction that this can change any time quickly.

Recap of the Bull Case

The bull case for proudly owning HHC shares contains:

1/ HHC is comprised of a singular assortment of grasp deliberate group (MPC) belongings in sunbelt markets that are experiencing a inhabitants growth. Here’s a video of Invoice Ackman describing HHC’s MPC enterprise. In a MPC, one entity owns a contiguous parcel of land the place it’s the de facto municipality (actual life Sim Metropolis). MPC have the potential for important worth creation for buyers with very long time horizons as:

A) As a result of all of the land is owned by one entity, undertaking development might be coordinated to optimize land use/get the optimum mixture of retail, workplace, residential, industrial, and so on.

B) Whereas oversupply can depress CRE markets/submarkets, by a managed improvement program – to an extent (inside the submarket) the MPC proprietor can restrict improvement and scale back the danger of extra provide which ought to bolster rents and property costs – even in downturns.

C) MPCs can deal with creating upscale single household residential communities with excessive family incomes that enhance the worth of surrounding retail, workplace, and multifamily rents and property values.

2/ HHC trades at a deep (65%) low cost to the corporate’s printed NAV estimate. SA Contributor Noor Darwish does an ideal job of strolling by HHC’s NAV estimate and discussing changes buyers could wish to think about.

3/ Invoice Ackman has a powerful investing monitor file as head of Pershing Sq. and as Chairman he’ll guarantee worth creation for HHC shareholders.

What has gone improper?

Regardless of the aforementioned positives, an investor who bought HHC shares 10 years in the past could be down 14% on his buy whereas having acquired zero dividends over the previous decade. By comparability, an investor within the Vanguard REIT Index/ETF (VNQ) would have earned simply over 6% complete annualized return over the previous decade. You will need to perceive that Invoice Ackman has been Chairman of the Board your complete time (since 2010).

Here is a have a look at a number of the issues which have gone improper at Howard Hughes previously 10 years:

1/ Slightly than deal with its core MPC enterprise, the corporate has made a foray into an ill-conceived speculative improvement undertaking referred to as Seaport in New York. Whereas HHC has sunk over $1 billion into this undertaking since 2014. Regardless of completion in 2019, right now Seaport is producing no web working revenue (it’s really nonetheless burning money). Honest to say this undertaking has been a complete bust.

2/ The majority of HHC’s MPC belongings are situated within the larger Houston MSA (Bridgeland & the Woodlands). Houston’s financial system is closely depending on the power sector which suffered a big downturn from 2015-2020. Past cyclical elements, Houston is a structurally challenged business actual property market, largely attributable to a scarcity of zoning (provide, provide -there’s at all times loads of provide). Whereas HHC’s belongings are considerably insulated from provide (as a result of HHC controls the provision inside a number of miles), Bridgeland and the Woodlands are competing with decrease value properties within the surrounding space. That is unlikely to vary.

3/ Nearly half of HHC’s stabilized (revenue producing) belongings are workplace properties in Houston. Workplace values have plummeted for the reason that onset of the pandemic and have fallen additional as rates of interest have soared in 2022. HHC’s NAV relies on cap charges within the 6-7% vary whereas most workplace REITs are buying and selling with implied cap charges of 8-10%.

A few of these had been bought in late 2019 (to some extent unfortunate as COVID hit months after the deal closed). However it may be argued that purchasing present workplace properties as outdoors the core competency of an MPC developer/operator -especially given the scale of the transaction (was ~11% or so of complete belongings on the time).

4/ Failed gross sales course of in 2019 – In June 2019, HHC introduced it was reviewing its strategic options to maximise shareholder worth. Whereas this despatched the shares up 40% to ~$135 on the day of the announcement, the evaluation concluded and not using a sale (no rumored bids), buyers started to query the true worth of HHC and its belongings, and the inventory worth plummeted.

5/ The onset of the pandemic coincided with the big workplace buy pressured HHC to promote fairness at $50/share in 1H20 to shore up its steadiness sheet.

6/ Howard Hughes has incurred ~$1.2 billion ($20+/share) in overhead bills over the previous decade. Improvement operations are way more pricey to run than stabilized actual property operations (accomplished buildings).

Why I am Not Shopping for the Inventory right now

Lots of the aforementioned elements which have prompted the huge underperformance over the previous decade stay in place right now:

1/ Invoice Ackman stays Chairman. With 27+% possession (probably going to 40%) he’s firmly in command of HHC. Whereas Ackman has been an excellent investor total, his magic has not labored at Howard Hughes and it’s unclear what would trigger this to vary.

2/ Houston will stay a troublesome market – a scarcity of zoning is an ongoing invitation for oversupply in surrounding areas. Whereas HHC is considerably insulated from this (larger revenue submarkets with the flexibility to regulate provide) the town stays depending on the power financial system (which is admittedly offering a lift nowadays).

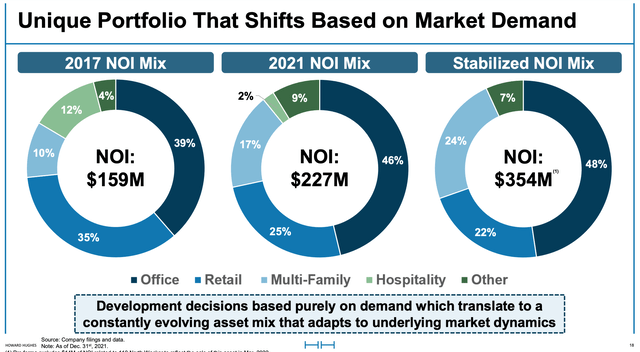

3/ Almost half of NOI (see beneath) comes from workplace properties. That is forecast to extend – HHC has extra new workplace properties in improvement. The way forward for workplace is unsure given the double whammy of make money working from home pressures in addition to an financial downturn.

NOI by Property Sort (Howard Hughes Investor Presentation)

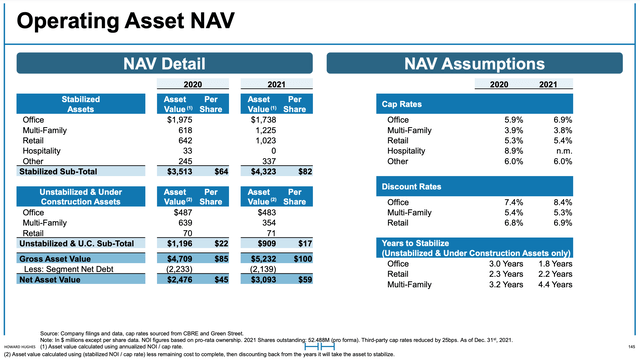

4/ Cap charges are too optimistic. Beneath I present cap charges assumed by HHC in its NAV estimate:

Cap charge assumptions (Investor Presentation )

As I discussed, implied workplace cap charges are meaningfully larger than these assumed above. The identical holds true for multifamily, retail and different.

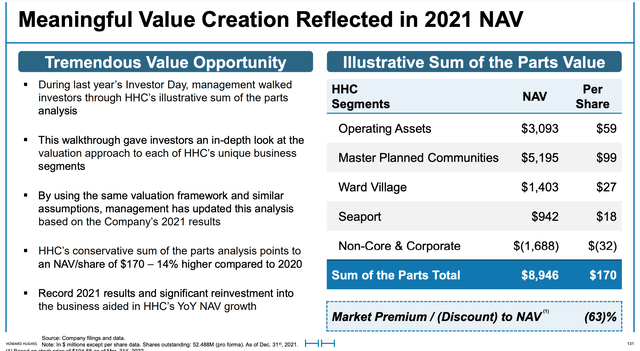

5/ Undeveloped land is a troublesome place to be in an financial downturn -Given the dramatic rise in rates of interest, we’re already seeing a dramatic slowdown in new dwelling development and are seeing the start of a slowdown in business actual property improvement. As proven beneath, over half of HHC’s estimated NAV comes from properties for improvement (Grasp Deliberate Communities within the NAV slide beneath). Undeveloped land is mostly thought-about the best danger/most speculative sort of property funding. The explanation for it is because whereas leased/stabilized properties generate constructive money flows for homeowners, undeveloped property requires money movement (with no certainty of payback). An financial downturn additional will increase this danger because it lengthens the interval buyers must put in money and pushes out the last word receipt of that money.

Howard Hughes Administration’s NAV Estimate (Investor Presentation)

Conclusion

I’m not satisfied that HHC’s future can be materially completely different from its previous given the structural challenges of lots of its belongings and my perception that the corporate will fare poorly in an financial downturn. Additional, with most prime quality REITs buying and selling at significant reductions to NAV and paying 3.5+% and rising dividend yields (I’ve written up a handful right here on SA over the previous few weeks which supply enticing upside), I see no motive to get entangled with Howard Hughes. Whereas HHC is probably going undervalued, advanced sum-of-the-parts NAV tales (with no dividend as land represents a lot of the worth) have a tendency to remain low cost.

{kind=link}