Scott Olson/Getty Photos Information

Opening ideas

DraftKings Inc. (NASDAQ:DKNG) has been a polarizing inventory in recent times. The corporate’s inventory climbed above $70/share in early 2021 as demand soared and sentiment surrounding the trade was extraordinarily optimistic. Since then, shares of the web playing firm have plummeted, and nearly all good points made because the begin of the pandemic have been erased. The pullback has stemmed from a wide range of components, each company-driven and macroeconomic-related. As headwinds like rate of interest hikes and the Russia-Ukraine disaster proceed to rattle the financial system, traders have gotten more and more risk-averse. And on condition that DraftKings remains to be years away from reaching profitability, the corporate stays a dicey long-term play.

DraftKings shares are down 66% this previous yr, and lots of traders are actually displaying curiosity within the inventory. Whereas the corporate’s valuation has grown extra enticing, there are higher alternatives out there for traders who need to exploit the market’s insanity at the moment. I believe DraftKings’s risk-to-reward ratio is unfavorable, and I do not suggest shopping for the inventory right now.

Sturdy income development and market potential

We’re witnessing a paradigm shift within the playing trade in direction of on-line betting. At the moment, 18 states enable cell sports activities betting, and solely six authorize on-line casinos. As mainstream adoption expedites and extra states proceed to approve laws, the market potential for firms like DraftKings ought to develop exponentially. The worldwide on-line playing market is projected to develop at a compound annual development fee (CAGR) of 12% by way of 2027, as much as $127.3 billion. Since DraftKings has captured practically 30% of the web sports activities betting market within the U.S., the corporate is in a agency place to get pleasure from sturdy development transferring ahead.

Up so far, DraftKings has skilled spectacular top-line growth. In 2021, the corporate generated $1.3 billion in gross sales, translating to 111% development yr over yr. Ahead projections look promising as properly – analysts are modeling $2 billion in gross sales for 2022, representing 54% development from a yr in the past. By 2025, DraftKings income is forecasted to climb to $3.9 billion, implying a median annualized development of 25% from 2021 income.

The corporate’s gross sales development has been excellent, however it comes at a value for traders. DraftKings continues to spend aggressively with the intention to broaden its operations, which in flip has led to monstrous losses. Progress is essential, however profitability is simply too. DraftKings is much away from reaching that milestone.

Profitability is out of sight

DraftKings’ present enterprise mannequin depends intensely on substantial spending to develop its attain. This previous yr, the corporate’s complete working bills elevated 99%, as much as $2.8 billion. In consequence, DraftKings generated an EBITDA lack of $1.4 billion, notably greater than the $729 million EBITDA loss in 2020. Shifting backwards – though many say this may be vital for the longevity of DraftKings’ enterprise – isn’t optimum from a shareholder’s standpoint.

In its most up-to-date earnings announcement, administration indicated that it expects a internet loss between $825 million and $925 million in 2022, a variety greater than what Wall Road analysts had been initially forecasting. In keeping with Searching for Alpha knowledge, analysts aren’t modeling a full-year of profitability for DraftKings till 2027, that means traders must wait the till the latter half of the last decade for the corporate to comprehend a optimistic bottom-line.

There are not any guarantees that DraftKings will ultimately flip a revenue, both – the web playing market is turning into extraordinarily crowded, and there are nonetheless regulative query marks in a lot of states. As a long-term investor, I am completely effective having to attend a number of years for an organization to turn out to be worthwhile. That mentioned, it is essential that an organization present materials progress. I do not suppose DraftKings has been in a position to do this in latest quarters.

DraftKings remains to be costly

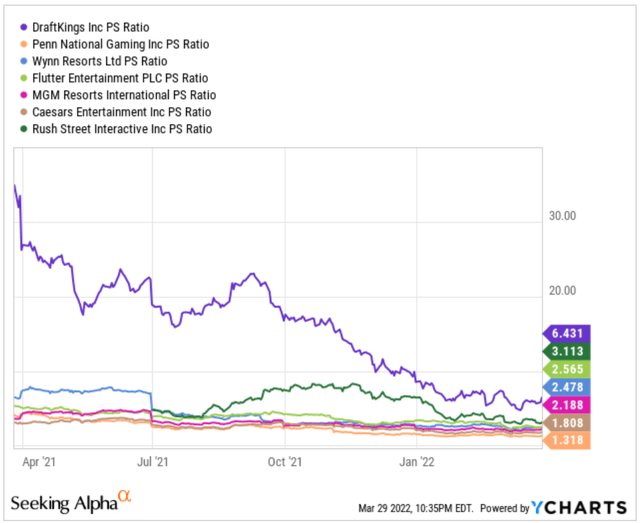

In March 2021, DraftKings was buying and selling round 30 occasions gross sales. Immediately, the corporate bears a price-to-sales a number of of 6.4x, practically 5 occasions lower than a yr in the past. This has led many to consider the inventory is undervalued, and thus, presents traders an advantageous alternative to amass the web playing firm at a cut price value.

However not so quick. DraftKings’ valuation has normalized, however the inventory remains to be costly in comparison with opponents. DraftKings’ 6.4x price-to-sales a number of is patently greater than shut trade friends like Penn Nationwide Gaming (NASDAQ:PENN), Flutter Leisure (OTCPK:PDYPY), and MGM Resorts Worldwide (NYSE:MGM), which carry multiples of 1.3x, 2.6x, and a couple of.1x, respectively.

It is a fallacy to suppose that DraftKings shares are actually low-cost. Sure, the corporate’s inventory is extra moderately priced than earlier than, however it’s nonetheless costly relative to trade friends. Traders ought to wait till DraftKings’ price-to-sales a number of approaches the 2x-3x vary earlier than contemplating a stake within the on-line playing firm.

YCharts

Keep on the sidelines for now

DraftKings’ unpromising path to profitability and comparatively excessive valuation creates an unfavorable risk-to-reward ratio for traders. In at the moment’s market, many individuals see inventory costs falling drastically and robotically assume that they’re cheap. The reality is that many tech shares soared to unjustifiable highs in recent times, and now the market is doing its half in correcting their once-outrageous valuations.

Until you’ve got an especially excessive danger tolerance, I might keep away from DraftKings in any respect prices. Wait till the corporate is ready to show that its enterprise mannequin is sustainable and presents a transparent path to profitability. I counsel traders to remain away from DraftKings for now – there are extra favorable funding alternatives at our disposal at the moment.

{kind=link}