islander11

While you undergo Informatica’s (NYSE:INFA) profile web page on SA, you will notice a variety of actions round information, along with the same old AI and cloud providers.

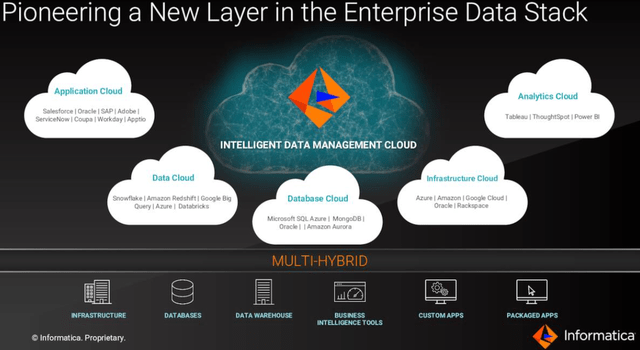

What’s totally different from others is that as a substitute of simply speaking concerning the cloud, its focus is extra to offer its providers in a Information-as-a-Service vogue utilizing its IDMC or Clever Information Administration Cloud for enterprises as pictured beneath.

IDMC (seekingalpha.com)

One other topic of curiosity is its elaborate ecosystem of partnerships. Therefore, my focus with this thesis is to point out how this method can assist generate ARR (Annual Recurring Revenues) which represents a extra secure supply of gross sales in a deteriorating financial surroundings as excessive inflation grinds in company disposable earnings. I can even have a look at the sustainability of the working mannequin by wanting on the Capex and money move ratios.

I begin by offering insights as to why companies want information administration providers within the first place.

Information-as-a-Service and Informatica’s Partnerships

With the event of a mess of applied sciences, there isn’t a scarcity of functions to assist staff carry out varied features like advertising and marketing or accounting, however the problem is now care for the underlying information, together with capturing, storing, looking out, and analyzing.

On this connection, whereas expertise together with large information have overcome among the technical points in analyzing information there are different challenges remaining within the business like quickly combine information from totally different sources for decision-making functions. On this respect, the corporate’s IDMC is designed to assist companies course of and acquire actionable insights out of their information on any platform, be it multi-cloud, or hybrid. Along with the convenience of shopping for a subscription versus the complexity of getting to put in software program, this method is termed as Information-as-a-Service.

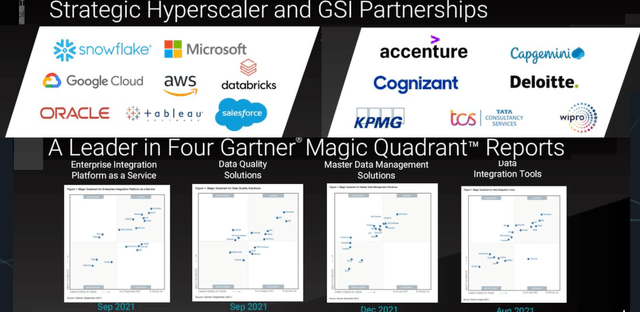

Wanting on the business, there are actually tons of corporations providing information integration providers, however, one factor which clearly distinguishes Informatica is its capacity to have solid strategic partnerships with all the main cloud suppliers like Microsoft’s (NASDAQ:MSFT) Azure, Amazon’s (NASDAQ:AMZN) AWS, Google’s (NASDAQ:GOOG) (GOOGL) GCP and Oracle (ORCL). As well as, it has partnered with international system integrators like Accenture (ACN) which permits Informatica to co-sell options to clients.

Partnerships and Gartner Magic Quadrants (www.seekingalpha.com)

Consequently, with its differentiated product providing, it has been awarded management positions by Gartner in 4 classes all associated to information as proven above.

Wanting deeper, one of many elements which have enabled it to realize such a aggressive moat is vendor neutrality for expertise. That is an usually ignored side, however the important thing to making sure that each one buyer information migration choices pertaining to transferring IT workloads from on-premise information facilities to the cloud are carried out solely based mostly on the precise necessities, not biased by the expertise for use. That is additionally the rationale Informatica’s IDMC can be utilized by clients already subscribed to service suppliers like Snowflake (SNOW) and Databricks.

Partnerships have translated into extra co-selling alternatives or a 105% enhance over the past yr.

Income Combine and Headwinds

Coming to the outcomes for the second quarter of 2022 (Q2), The uptake in Information-as-a-Service is mirrored by subscription revenues growing to represent 56% of whole gross sales in comparison with 49% a yr in the past. Furthermore, 94% of subscribers renewed their plans in comparison with 93% earlier than.

Income Combine (www.seekingalpha.com)

As seen within the above chart, along with subscription (in orange), there’s additionally migration (in blue) whereby the corporate performs maintenance-related works for corporations shifting their workloads to the cloud earlier than turning them into subscribers for its IDMC. Since subscription follows migration and it usually takes 9-12 months between the 2, it’s doable to have an concept of the long run subscriber revenues simply by wanting on the above chart.

Shifting to profitability, non-GAAP Gross margins for Q2 had been at 81% which interprets into 79.2% of GAAP gross margins. Additionally, these have diminished from the 82.2% obtained in the identical interval final yr. Now, on account of whole working bills going up by 3.41% in Q2 in comparison with 2021, Informatica has suffered from an working margin lack of -3.26% in comparison with a revenue margin of 4.22% throughout the identical interval final yr.

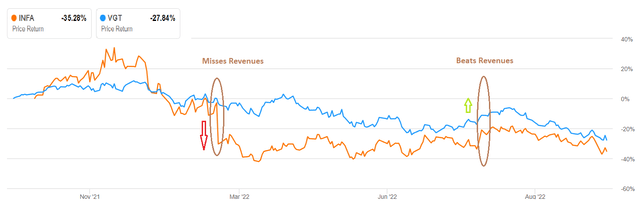

Now, given present monetary circumstances the place buyers are more and more targeted on profitability metrics, the flexibility of Informatica to ship profitability is important, however, for this to occur, it should ship a constant prime line, or danger being punished by buyers. Thus, when it missed analysts’ forecast by $1.32 million for its first quarter outcomes, it suffered from an above 20% draw back (as indicated by the crimson arrow within the chart beneath), and this, regardless of recording an 8.6% Y/Y development. I’ve additionally included the Vanguard Data Know-how ETF (VGT) in blue which incorporates many IT shares for comparability functions.

Value Efficiency (www.seekingalpha.com)

Conversely, as proven by the inexperienced arrow, when Informatica beat income expectations by $7.36M on the finish of July, it was rewarded by an upside.

At the moment, ARR had elevated by 31% to $896 million, with the cloud part (cloud ARR) growing by 42% to $373 million. Thus, the 40% in cloud ARR anticipated for Q3 and for the total yr represents a lower. This is because of forex headwinds on account of the robust dollar, which additionally explains why the entire income steering for 2022 has been introduced down by $45 million to $1.55 billion (midpoint) with free money move (unlevered) steering additionally minimize by $33 million to $300 million (midpoint). In line with the CEO, the corporate has began “to see some clients delay funds”.

Now, with the greenback having already appreciated by greater than 7.5% since July and the Federal Reserve prioritizing climbing rates of interest to deliver down excessive inflation, there’s a excessive likelihood that the corporate may miss its income steering within the third quarter with outcomes to be introduced on October 26.

Nevertheless, there are positives too.

Valuations, Cashflow-to-Capex and Conclusion

First, in case clients who’ve deferred funds carry out the identical within the fourth quarter, the corporate may see further revenues, probably prompting a income beat. Second, Informatica’s working earnings steering for fiscal 2022 is maintained as a good portion of bills is made in overseas forex, not in {dollars}. This has helped to mitigate the impact of upper prices in America.

As for valuations, regardless of its above 35% draw back within the final yr, at a value to gross sales of three.65x, the info administration play stays overvalued with respect to the median for the IT sector by almost 40%. Subsequently, this inventory doesn’t represent an opportunistic purchase.

Considering aloud, the corporate has some benefits, however lots will depend upon the way in which it is ready to drive revenues. For this function, it has considerably expanded its market measurement on account of its robust partnership ecosystem because it has entry to huge collections of buyer information units to market its Information-as-a-Service choices.

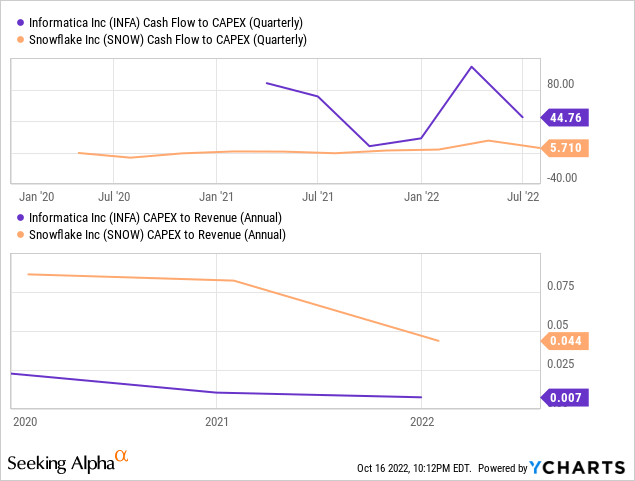

This working mannequin has generated the next working money move relative to Capex spent than Snowflake as proven within the chart beneath.

Furthermore, its annual Capex to Income ratio stays a lot decrease than Snowflake too, signifying that it doesn’t must tackle further debt to finance the enterprise with the intention to generate development. On this respect, the steadiness sheet exhibits that the IDMC firm has been in a position to cut back debt whereas growing money over the last 4 years.

Pursuing additional, with its Information-as-a-Service method, possessing an clever platform as a development engine, and a robust ecosystem of partnerships, the corporate ought to proceed delivering extra subscription ARR. Nevertheless, it’s not proof against an additional draw back in case it misses income forecasts in the course of the Q3 earnings name on October 26. On this regard, the strengthening greenback simply will increase the likelihood of one other draw back subsequent week in case there’s a income miss with respect to expectations. This may occasionally represent a possibility to purchase the inventory for long-term positioning.

Lastly, I’m optimistic for the long run as Informatica has a complete vary of information administration merchandise that permit clients to mess around with their functions with the intention to meet enterprise necessities, as digital transformation is now a secular pattern.

{kind=link}