Sunshine Seeds/iStock Editorial through Getty Photographs

Whereas I’ve executed fairly a bit of labor within the airline house (having largely picked the fitting winners and the fitting losers in my April 2020 examine of the sector in a COVID-19 restoration surroundings), I by no means had the pleasure of researching Worldwide Consolidated Airways Group (OTCPK:ICAGY) till now.

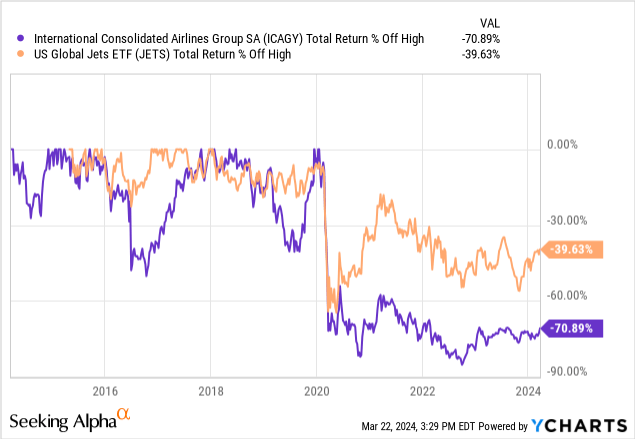

At first look, two issues stood out and immediately sparked my curiosity: (1) how far this inventory has dipped from pre-COVID ranges (see chart beneath), and (2) how strong the corporate’s fundamentals look, not less than relative to the remainder of the airline sector and to itself in 2019. Based mostly on my first evaluation and understanding that this extremely cyclical business is a dangerous one, ICAGY seems like an inexpensive buy-and-hold play at present ranges.

Worldwide Consolidated Airways: All However Absolutely Recovered

The 71% inventory value drawdown right this moment relative to early 2020 ranges may lead one to imagine that Worldwide Consolidated Airways Group (which I’ll check with as ICAG, for simplicity) is way from having recovered from the COVID-19 disaster. Nonetheless, this doesn’t appear to be the case in any respect.

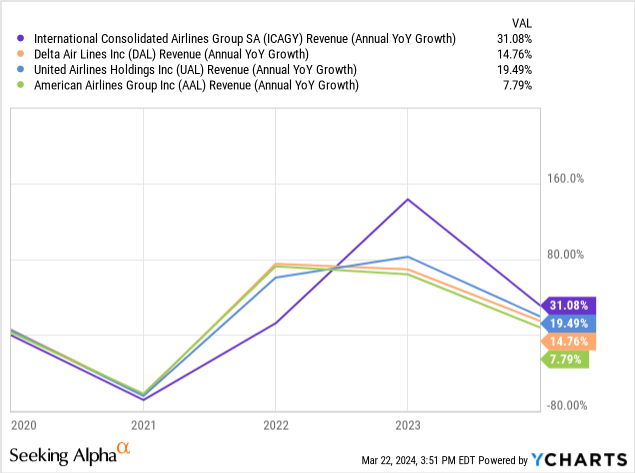

In the latest earnings launch, the airline reported full-year 2023 revenues of EUR 29.5 billion, a whopping EUR 6.4 billion increased YOY and roughly EUR 4.0 billion above 2019 gross sales. The robust top-line efficiency was supported first by capability that has nearly returned to pre-COVID ranges at 80.8 billion obtainable seat kilometers in This autumn’23 — practically 99% of the corporate’s pre-pandemic capability.

Load issue of over 85% in 2023 jumped by a wholesome 3.5 share factors YOY which, coupled with an 8% enhance in income per income passenger kilometer, helped to drive the full-year income progress of 28% in Euro phrases (31% in USD). For reference, Delta Air Traces (DAL) and American Airways (AAL) grew revenues in 2023 by 15% and eight%, respectively (see beneath).

One of many key options of ICAG’s enterprise mannequin is the diversification throughout markets and verticals (e.g., Europe home and worldwide; full-service and low-cost; leisure and enterprise) supplied by the airline portfolio that ranges from legacy names like British Airways and Iberia to ULCC manufacturers like Vueling and Stage. Nonetheless, all of the airways appear to be doing properly, with every having grown capability and occupancy in 2023 vs. 2022, and lots of having executed so relative to 2019 as properly.

Working margin final 12 months practically reached 12%, considerably higher than the prior 12 months’s 5.4%, regardless of gasoline prices per unit of capability having elevated minimally YOY. The margin enchancment was pushed by positive factors of scale from the spike in revenues; a mixture shift to worldwide and premium leisure; and the corporate’s efforts to comprise worker expense enhance to “solely” 17%.

True, working prices are anticipated to rise in 2024, even on a per-unit foundation. However this appears to be the results of ICAG’s footprint growth because it launches new routes in North and South America and will increase its plane fleet to reap the benefits of what the administration workforce sees as “demand [that] continues to be strong, with specific power in leisure journey”.

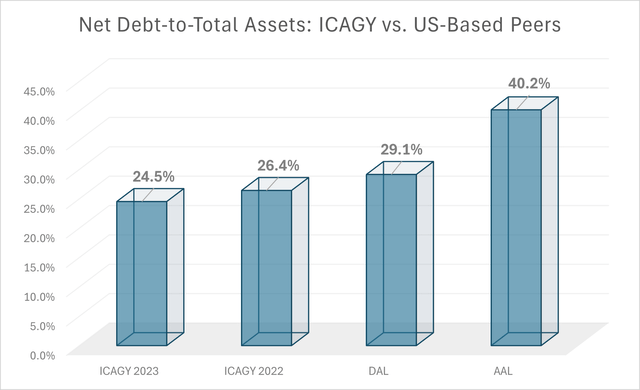

From a stability sheet perspective, ICAG additionally appears to be on respectable footing. Internet debt, not together with immaterial pension liabilities, has moved in the fitting path: from EUR 11.7 billion in 2021 to EUR 10.4 billion in 2022 and EUR 9.2 billion final 12 months. Relative to complete belongings, ICAG’s internet debt ratio of 24.5% compares favorably to 26.4% in 2022 and even to Delta’s 29.1%, which I think about to be a US-based airline with a stable stability sheet (see beneath).

DM Martins Analysis

ICAGY’s Low Valuation Is Attractive

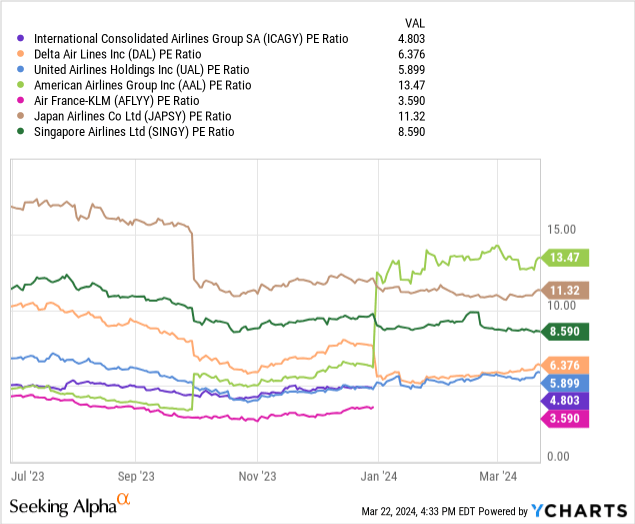

From my first evaluation of the corporate, all appears to be going properly with Worldwide Consolidated Airways Group, aside from its inventory. That is mirrored in valuations that look overly de-risked, for my part (see beneath), at a trailing P/E of solely 4.8x.

This isn’t to say that investing in an airline inventory will not be with out substantial dangers. Fairly the opposite: airways are uncovered to the financial cycles, totally on the income aspect, and to the ups and downs of gasoline costs on the fee aspect. By design, an airline inventory ought to commerce cheaply for these causes.

Nonetheless, I imagine that ICAGY trades at too deep a reduction relative to most of its friends, particularly given the robust fundamentals and inspiring progress prospects for 2024. Subsequently, I see ICAGY as a purchase relative to the remainder of the worldwide airline house.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}