The Biden Administration lately issued a proposed rule to make it simpler for members of the family of staff provided medical health insurance at their jobs to qualify for premium tax credit for Market protection. The proposal goals to deal with what has been known as the “household glitch”. Underneath the ACA, a person enrolling in a Market plan will not be eligible for a premium tax credit score if they’re eligible for job-based protection that’s thought of inexpensive and offers minimal worth (i.e., covers not less than 60% of well being bills on common). Present rules present that job-based protection is taken into account inexpensive to a employee and their dependents if the price of self-only protection for the employee is lower than 9.6 p.c of household revenue, with out regard to the price of including members of the family. The proposal would revise that interpretation by assessing the affordability of job-based protection obtainable for the members of the family of a employee by evaluating the overall price for the entire household (together with the employee) to the 9.6 p.c threshold. This evaluation would measure affordability for family members aside from the employee. Affordability for the employee himself or herself would proceed to be primarily based on the price of self-only protection.

The proposed rule explains that the present interpretation results in circumstances the place members of the family are thought of to have an inexpensive supply even once they face very excessive contribution quantities in the event that they need to enroll in that protection, which the businesses assert will not be in line with the ACA’s objective of offering entry to inexpensive protection for everybody. We beforehand estimated that 5.1 million individuals are presently caught on this ‘household glitch’.

On this evaluation, we use the KFF Employer Well being Advantages Survey (EHBS) to have a look at the shares of staff that may pay vital quantities to enroll households and the way these shares range throughout companies. These are the employees almost definitely to learn from a repair to the household glitch.

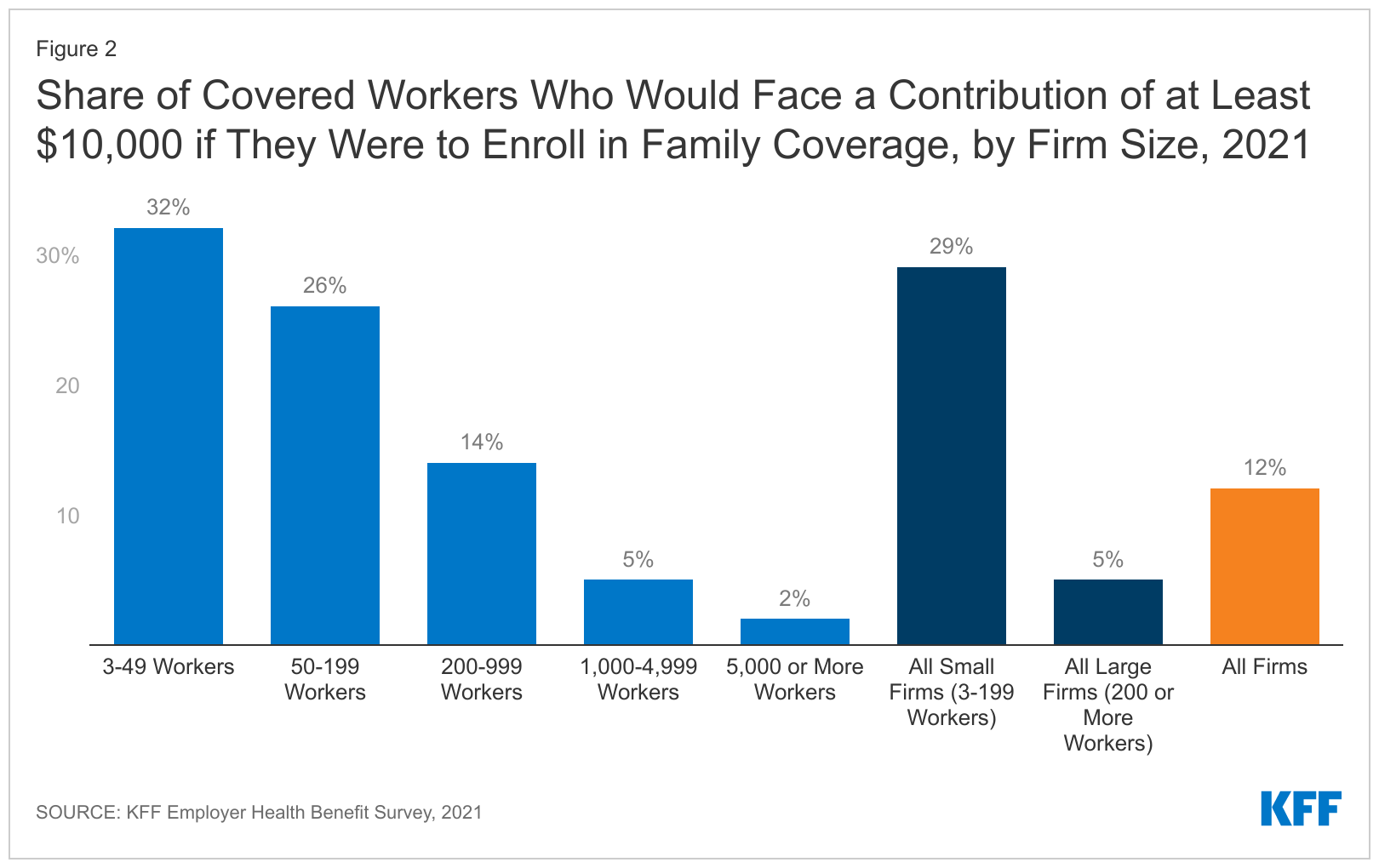

Medical health insurance is dear. The common premiums in 2021 have been $7,739 for single protection and $22,221 for a household of 4. The common contribution quantities for lined staff have been $1,299 for single protection and $5,969 for a household of 4. Importantly, there was appreciable variation round these averages: for instance, ten p.c of lined staff have been enrolled in a plan with a premium of greater than $29,000 for household protection; and 12% of lined staff have been enrolled in a plan with a contribution of not less than $10,000 for household protection. It’s the members of the family of staff in companies with excessive contributions which are almost definitely to learn from the proposed rule change.

Earlier than taking a look at among the traits of those companies and staff, we must be clear about what these percentages imply. After we say that 12% of lined staff are in a plan that has a employee contribution of not less than $10,000, we’re not saying that 12% of lined staff really enroll in household protection and pay these quantities. As a substitute, we’re saying that 12% of lined staff work at companies the place the contribution for a household of 4 for his or her largest well being plan (or generally a mean of a number of plans) is not less than $10,000. Surveys don’t accumulate details about the entire well being plans every employer might supply, nor are they capable of account for potential changes that may have an effect on particular person staff or households (smoking surcharges, reductions for filling out a well being threat evaluation, surcharge if partner is obtainable protection at one other job). So, whereas these surveys can’t give exact outcomes on precise prices, they provide a fairly good image of the magnitude of the prices staff face to enroll within the plans that the majority staff select.

Staff in small companies face increased contributions for household protection. Staff in small companies (3-199 staff) on common face increased contributions to enroll in household protection and usually tend to face very excessive contribution quantities. The common contribution for a household of 4 in 2021 was $7,710 for staff in small companies, in comparison with $5,269 for staff in bigger companies. Twenty-nine p.c of lined staff in small companies confronted a contribution of not less than $10,000 for household protection, in comparison with solely 5% of lined staff in bigger companies.

One cause household contributions could also be increased in smaller companies is that some small employers solely make a contribution towards the price of self-only protection, leaving the employee to pay the whole distinction between the premium for self-only protection and the premium for household protection. Even in companies deciding on much less complete protection, this distinction may be many 1000’s of {dollars}. We estimate that 19% of small companies providing well being advantages make little or no extra contribution in the direction of the price of household protection. These companies make use of about 17% p.c of the lined staff enrolled at small companies (3-199 staff).

Staff within the service business usually tend to face excessive contributions for household protection. Contributions for household protection range considerably by business. Coated staff in sure industries usually tend to face excessive contributions for household protection whereas lined staff in different industries (wholesale, transportation, communications, utilities, state and native authorities) are much less possible.

The proposed rule addresses the eligibility for premium tax credit in conditions the place staff face unaffordable contribution quantities to enroll their members of the family in job-based protection. Information from the KFF Employer Well being Advantages Survey demonstrates that some staff face very excessive contribution quantities for household protection, with 12% dealing with a contribution of not less than $10,000 for a household of 4. Staff with protection by small companies are notably prone to excessive contributions for household protection, and would due to this fact profit from the household glitch repair.

| The annual KFF Employer Well being Advantages Survey (EHBS) for 2021 was carried out between January and July of 2021, and included nearly 1,700 randomly chosen, non-federal private and non-private companies with three or extra workers. The complete EHBS, together with an in depth methodology part, is out there at ehbs.kff.org. EHBS collects info from employers about how a lot employers and workers contribute of their largest well being plans. |

{kind=link}