Based mostly on marketing campaign pledges, President Biden is predicted to reopen Market enrollment, for instance, by way of a COVID-19 particular enrollment alternative (SEP), and his administration can also be anticipated to direct considerably extra sources to advertising and outreach efforts. Thousands and thousands of individuals stay uninsured regardless of being eligible totally free or decreased price protection by way of the ACA Marketplaces or Medicaid Enlargement.

In most states, the Open Enrollment interval for 2021 Market protection ended on December 15, 2020. Plan choices in states that use the federally facilitated trade (HealthCare.gov) have been up by about 6% in comparison with the earlier 12 months, due largely to excessive charges of customers renewing their protection. Plan choices amongst new customers have been down relative to the earlier 12 months, although, which was considerably shocking given the sustained ranges of unemployment in the course of the pandemic. In truth, enrollment amongst new customers has decreased annually since 2016, akin to substantial Trump Administration cuts to funding for ACA advertising and outreach actions.

In an earlier evaluation, we estimated that the general uninsured price had not modified dramatically as of September 2020, largely as a result of losses in employer protection seem to have been offset by beneficial properties in Medicaid protection. Whereas this means the ACA is working as a security web in the course of the present financial disaster, a comparatively flat uninsured price suggests there are nonetheless doubtless tens of thousands and thousands of Individuals with out medical health insurance throughout a worldwide pandemic.

On this evaluation, we look at key demographic traits of the uninsured eligible to purchase Market protection, estimating the numbers of people that may profit from an SEP and the way outreach actions is likely to be greatest focused. We focus particularly on the roughly 15 million uninsured individuals who may store for protection on the Marketplaces, together with those that are and aren’t eligible for a subsidy. We exclude people who find themselves eligible for Medicaid or Medicare, in addition to those that are undocumented immigrants. We additionally exclude individuals who fall into the Medicaid protection hole, since Market protection is usually unaffordable to folks with incomes beneath poverty.

In comparison with the final U.S. non-elderly inhabitants, we discover that Market eligible uninsured persons are considerably extra prone to be male (56% vs. 50%), Hispanic (29% vs. 20%), younger adults (38% vs. 25%), and/or working within the fields of arts, leisure, recreation, or building. We establish three major teams of Market eligible uninsured folks – these eligible totally free bronze plans, these eligible for partial subsidies, and people ineligible for subsides – and spotlight a number of the key traits of every group that might inform advertising, outreach, and enrollment help actions.

Findings

This transient makes use of 2021 premiums from HealthCare.gov and KFF evaluate of state price filings. Information on inhabitants, earnings, and eligibility for subsidies come from KFF evaluation of the Census Bureau’s 2019 American Group Survey (ACS). The 2019 ACS collected earnings and protection knowledge from respondents earlier than the pandemic, however there are numerous causes that the info are nonetheless an inexpensive foundation for present uninsured eligibility analyses. First, the nationwide uninsured price has stabilized in recent times and expectations are that it has remained comparatively flat to this point in the course of the pandemic. Second, the variety of uninsured folks eligible and ineligible for subsidies have additionally stayed usually constant. KFF has estimated the variety of uninsured folks eligible totally free bronze plans has fluctuated between 4.2 and 4.7 million the previous three years.

Nationally, sure teams are overrepresented among the many uninsured who’re Market eligible: 29% are Hispanic (in comparison with 20% of non-elderly folks within the U.S.), 53% have a highschool diploma or much less (in comparison with 36% of non-elderly adults within the U.S.), and 38% are younger adults (in comparison with 25% of non-elderly folks within the U.S.). The appendix contains detailed tables with the traits of the uninsured Market eligible inhabitants, in addition to the subcategories we establish beneath.

In our evaluation of the roughly 15 million uninsured folks nationally who may very well be get protection on the Market, we look at three teams individually (Desk 1):

- 4.0 million uninsured folks may get a free bronze plan (with a $0 premium fee, after accounting for subsidies). As defined in our earlier transient and in some element beneath, folks on this group would clearly profit from getting Market protection quite than persevering with to go with out protection.

- 4.9 million uninsured folks may buy Market protection for a decreased premium, partially lined by a subsidy. Though subsidies for this group don’t cowl the total premium, they could considerably decrease the premium and/or out-of-pocket legal responsibility. Even so, some folks on this group should still discover Market protection unaffordable or unattractive as a result of excessive deductibles.

- 6.0 million uninsured persons are eligible to purchase Market plans however are ineligible for monetary help. Of this group, 2.6 million (43%) have incomes that may qualify them for a subsidy, however their unsubsidized premium will not be excessive sufficient to advantage monetary help below the present ACA subsidy construction. The remaining 3.4 million (57%) folks on this group are ineligible for subsidies as a result of their earnings exceeds 400% of poverty. Individuals on this closing group are sometimes priced out of protection below the ACA’s present subsidy construction.

| Complete Uninsured Market Eligible* | Uninsured Eligible for Free Bronze Plan | Uninsured Eligible for Subsidies That Do Not Cowl Full Value of Bronze Plan | Uninsured Ineligible for Monetary Help** |

| 14.9 Million (100%) |

4.0 Million (27%) |

4.9 Million (33%) |

6.0 Million (40%) |

| NOTES: *Uninsured Market eligible inhabitants doesn’t embody folks with incomes beneath poverty who fall into the Medicaid protection hole or these eligible for a Fundamental Well being Plan in MN or NY. **The uninsured ineligible for monetary help class contains folks with incomes above 400% of poverty or who stay in counties the place the Benchmark plan prices lower than the relevant premium cap for his or her family earnings (see right here for extra element on the ACA subsidy construction). SOURCE: KFF evaluation of 2019 American Group Survey. |

|||

Free Bronze Eligible Uninsured: Key Traits

We estimate that 4.0 million uninsured folks within the U.S. may get a bronze plan on the ACA Market with a $0 premium contribution, after accounting for his or her subsidy. As we have now defined in earlier analyses, many people who find themselves eligible for a free bronze plan are additionally eligible for a low-cost silver plan with a considerably decrease deductible (as a result of cost-sharing reductions, or CSRs). Almost two thirds (62%) of the uninsured eligible for a free bronze plan have family incomes between 100-200% of the poverty degree, making them eligible for considerably decrease deductibles in the event that they buy a silver plan as a substitute of getting a free bronze plan. The typical annual deductible for folks with incomes between 150-200% of poverty who select to enroll in a silver plan with a CSR is $800, dropping to $177 for folks with incomes between 100- 150% of poverty. Many individuals on this group, subsequently, may very well be higher off shopping for a silver plan than a bronze plan.

Even so, all of the uninsured eligible for a free bronze plan can be higher off making the most of that bronze protection as a substitute of remaining uninsured. Individuals on this group might need assistance understanding the tradeoff between silver and bronze protection (i.e. affordability of the premium and deductible), in addition to assist understanding the advantages that even a high-deductible bronze plan affords over being uninsured (i.e. free preventive care, restricted out-of-pocket legal responsibility, decrease negotiated fee charges to suppliers, and sometimes not less than some lined advantages earlier than having to satisfy the deductible).

Relative to the final non-elderly inhabitants within the U.S., uninsured folks eligible totally free bronze plans usually tend to be:

- Highschool educated: 62% of free bronze eligible adults have a highschool schooling or much less, in comparison with 36% of non-elderly adults within the U.S.

- Younger Adults: 39% of free bronze eligible uninsured persons are ages 19-34, in comparison with 25% of the non-elderly U.S. inhabitants.

- Working half time or unemployed: 49% of free bronze eligible adults work part-time or are unemployed, in comparison with 39% of non-elderly U.S. adults. (Notice that that is primarily based on pre-pandemic knowledge.)

- Hispanic: 32% of free bronze eligible uninsured persons are Hispanic, in comparison with 20% of the non-elderly U.S. inhabitants.

- Non-English speaker at house: 34% of free bronze eligible uninsured folks communicate a language apart from English at house, in comparison with 23% of the U.S. non-elderly inhabitants. Of the free bronze eligible uninsured who communicate a language apart from English at house, 79% communicate Spanish (although many are proficient in English and/or have a member of the households who speaks English proficiently).

- Working in arts/leisure or building: 25% of free bronze eligible uninsured adults who’re working are within the arts/leisure/recreation/different companies business, in comparison with 15% of non-elderly adults within the U.S. Moreover, 14% of the free bronze eligible uninsured who’re working are within the building business, in comparison with 7% of non-elderly working adults within the U.S. (Notice that that is primarily based on pre-pandemic knowledge.)

- Residing in rural areas: 19% of free bronze eligible uninsured folks stay in non-metro areas, in comparison with 13% of the non-elderly U.S. inhabitants.

- Missing web entry: 14% of free bronze eligible uninsured folks wouldn’t have web entry at house, in comparison with 6% of the non-elderly U.S. inhabitants.

- See Appendix for extra particulars and different demographic traits.

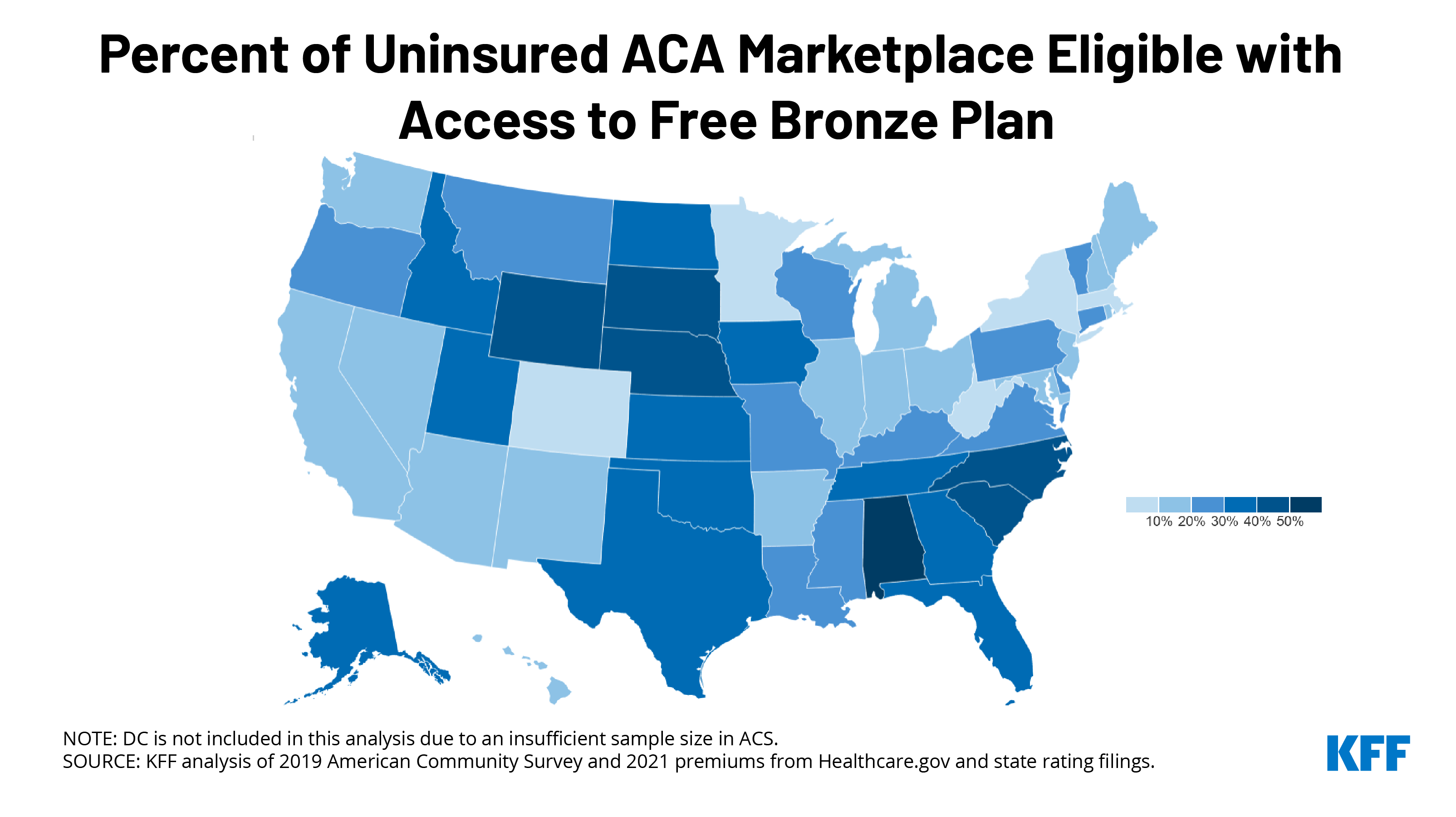

Greater than half of the uninsured who may get a free bronze plan stay in Texas, Florida, North Carolina, or Georgia. Different states with giant shares of uninsured residents who may join a no-premium bronze plan embody Alabama (53%), Wyoming (49%), South Dakota (47%), and Nebraska (46%) (Determine 1).

Partial Subsidy Eligible Uninsured: Key Traits

Along with the 4.0 million uninsured folks eligible for a subsidy masking the total price of a bronze plan, one other 4.9 million uninsured persons are eligible for Market subsidies that may decrease their premiums and/or out-of-pocket prices. (We discuss with this group as “partial subsidy eligible” as a result of their subsidy wouldn’t cowl the total price of their plan). Usually talking, folks on this group of potential Market enrollees have greater incomes than the individuals who can qualify for a free bronze plan. Most (69%) of the partial subsidy eligible uninsured have incomes between 200-400% of poverty.

The quantity of economic help obtainable to folks on this group can subsequently differ fairly a bit, with some folks eligible for pretty low-cost protection and modest cost-sharing reductions, and others eligible for under small month-to-month premium subsidies. As a result of most individuals on this group are ineligible for the substantial cost-sharing help obtainable to lower-income Market customers, and since silver plan premiums are inflated as a result of a follow generally known as “silver loading,” folks on this group might need assistance understanding why silver plans are an unattractive possibility and find out how to determine between bronze and gold protection.

Relative to the final non-elderly inhabitants within the U.S., uninsured folks eligible for partially backed Market plans usually tend to be:

- Male: 58% of partial subsidy eligible uninsured persons are male, in comparison with 50% of the non-elderly U.S. inhabitants.

- Highschool educated: 54% of partial subsidy eligible uninsured adults have a highschool schooling or much less, in comparison with 37% of non-elderly adults within the U.S.

- Younger Adults: 47% of partial subsidy eligible uninsured persons are ages 19-34, in comparison with 25% of the non-elderly U.S. inhabitants.

- Hispanic: 31% of partial subsidy eligible uninsured persons are Hispanic, in comparison with 20% of the non-elderly U.S. inhabitants.

- Non-English audio system at house: 34% of partial subsidy eligible uninsured folks communicate a language apart from English at house, in comparison with 23% of the U.S. non-elderly inhabitants. Of the partial subsidy eligible uninsured who communicate a language apart from English at house, 77% communicate Spanish (although many are proficient in English and/or have a member of the households who speaks English proficiently).

- Working in arts/leisure or building: 22% of partial subsidy eligible uninsured people who find themselves working are within the arts/leisure/recreation/different companies business, in comparison with 15% of non-elderly working folks within the U.S. Moreover, 14% of the partial subsidy eligible uninsured who’re working are within the building business, in comparison with 7% of non-elderly working folks within the U.S. (Notice that that is primarily based on pre-pandemic knowledge.)

- Missing web entry: 9% of partial subsidy eligible uninsured folks wouldn’t have web entry at house, vs. 6% of the U.S. non-elderly inhabitants.

- See Appendix for extra particulars and different demographic traits.

Subsidy Ineligible Uninsured: Key Traits

The ultimate group of uninsured folks eligible to purchase Market protection contains 2.6 million people who find themselves ineligible for a subsidy as a result of their premiums are too low and three.4 million who’re ineligible for a subsidy as a result of their incomes are too excessive below the present ACA subsidy construction.

The two.6 million who’re ineligible for a subsidy as a result of their premium will not be excessive sufficient to advantage monetary help below the present subsidy construction are usually comparatively younger with incomes within the higher finish of the subsidy vary (200-400% of poverty). As a result of younger folks have decrease unsubsidized premiums, they don’t all the time qualify for a subsidy even when their earnings would in any other case make them eligible. This group can also be largely ineligible for cost-sharing help, that means they doubtless face excessive deductibles that make their full-priced protection look much less enticing.

The remaining 3.4 million uninsured people who find themselves eligible to purchase on the Market are ineligible for subsidies as a result of their earnings exceeds 400% of poverty. Individuals on this group are usually somebody older, making their unsubsidized premiums much more costly. This group has been the main target of a lot of the criticism of the ACA, as a result of this group is basically ignored of the ACA’s protection expansions. As we have now proven in different analyses, older Market customers with incomes simply above 400% of poverty can see premiums that quantity to twenty% or extra of their pre-tax earnings.

Each kinds of potential Market enrollees who’re ineligible for subsidies below present legislation would profit from Biden’s plan to extend the quantity of economic help. Biden’s plan would enhance subsidies for these whose incomes are beneath 400% of poverty and broaden eligibility above the present 400% cliff. Biden’s plan would additionally peg subsidies to a gold plan, making it simpler to afford lower-deductible protection. Nevertheless, if Congress doesn’t act to make these adjustments, expanded advertising or outreach to uninsured folks with incomes over 400% of poverty can be unlikely to yield a lot greater enrollment due to the numerous affordability challenges they face.

Demographically, the subsidy ineligible uninsured who may purchase on the Market are remarkably just like the final U.S. inhabitants. Nevertheless, relative to the final inhabitants, they’re considerably extra prone to be male, middle-aged, and/or childless. 13% report self-employment earnings, in comparison with 6% of the non-elderly grownup inhabitants, and they’re additionally extra prone to work in building. Extra particulars can be found within the Appendix.

Dialogue

We estimate there are about 15 million uninsured individuals who may very well be buying Market protection, however aren’t taking it up. The explanations behind their lack of protection are various, doubtless starting from a lack of knowledge about obtainable choices, to being discouraged by excessive deductibles, or being priced out all collectively from excessive unsubsidized premiums.

Of the 15 million, we discover most (60%, or 8.9 million) qualify for monetary assist, together with 4.0 million (27%) who may get lined totally free with a $0 bronze plan. Bronze plans usually include steep deductibles, averaging near $7,000 in 2021. Nonetheless, for uninsured people who qualify totally free bronze plans, the advantages of taking-up protection as a substitute of remaining uninsured are clear, notably throughout a pandemic. Most individuals is not going to have well being spending that reaches a $7,000 annual deductible, however Market plans provide helpful monetary safety in opposition to surprising medical bills. A typical inpatient admission for folks with employer-sponsored insurance coverage prices upwards of $20,000 (non-negotiated charges for uninsured sufferers would doubtless be greater), and an inpatient admission for COVID-19 remedy may price rather more. As well as, all plans bought on the Market cowl preventive companies together with immunizations well being screenings freed from cost, and lots of plans cowl sure different companies with out making use of a deductible.

Greater than two-thirds of uninsured individuals who qualify for a free bronze plan additionally qualify for cost-sharing reductions (CSRs) that considerably decrease the utmost quantity an enroll can spend out-of-pocket in a 12 months. CSRs can be found to Market enrollees with incomes between 100% to 250% of the poverty, although the enrollee should select a silver plan. Since enrollees can apply their premium subsidies in the direction of a plan on any metallic degree, many uninsured individuals who qualify for a free bronze plan, particularly these in lower than excellent well being, may very well be higher off enrolling in a silver plan with a small or modest premium.

Uninsured people who find themselves eligible for subsidies to purchase Market plans could also be unaware of those choices or need assistance understanding the tradeoffs. The complexity of the ACA’s subsidy construction, made much more confounding by the follow of “silver loading,” could make it very troublesome for Market customers to know which metallic degree is greatest for them. The excessive deductibles in bronze plans might lead some uninsured folks to mistakenly imagine they may as nicely stay uninsured even when they’re eligible for a $0 premium bronze plan.

President Biden is predicted to extend the quantity of sources dedicated to outreach, advertising, and enrollment help applications below the ACA. Commercial and outreach alternatives for these functions have been restricted in the course of the Trump presidency, which can have suppressed Market enrollment. KFF researchers discovered that greater than $1 billion in unspent federal consumer payment income has gathered and may very well be used to put money into adjustments that may make it simpler for customers to enroll in well being protection.

The findings of this evaluation can inform authorities businesses, insurers, or Navigators tasked with outreach and advertising tasks, serving to them to focus on particular teams which can be extra prone to be uninsured however eligible for vital monetary help. Comparatively giant shares of uninsured folks eligible for vital help to purchase Market protection are younger adults with out faculty educations, Hispanic, non-native English audio system, and dealing within the fields of leisure, recreation, and building. Most individuals eligible totally free bronze protection are concentrated in a handful of states (Texas, Florida, North Carolina, and Georgia).

Along with the findings highlighted above, the appendix of this transient contains detailed demographics concerning the uninsured Market eligible inhabitants and, inside this group, the completely different traits throughout the assorted ranges of backed protection obtainable to them.

Strategies

2021 Premiums come from KFF evaluation of premium knowledge from Healthcare.gov and state ranking filings. Information on inhabitants, earnings, and eligibility for subsidies come from KFF evaluation of the Census Bureau’s 2019 American Group Survey (ACS). The ACS features a 1% pattern of the US inhabitants and permits for exact state-level estimates. The ACS asks respondents about their medical health insurance protection on the time of the survey. Respondents might report having multiple kind of protection; nevertheless, people are sorted into just one class of insurance coverage protection.

This evaluation doesn’t embody people who’re over the age of 65, who’re eligible for Medicaid in 2021, who’ve incomes beneath poverty, or are undocumented immigrants. We embody people who’re uninsured however turned down a proposal of employer-based protection. Beneath the present ACA construction, employees and their members of the family are ineligible for tax credit if any employee within the family is obtainable “reasonably priced” medical health insurance by way of their employer. Employer protection is taken into account reasonably priced if the employee’s premium contribution for self-only quantities to lower than 9.78% of family earnings. For the needs of this evaluation, people who find themselves uninsured however turned down a proposal of employer-coverage are categorized as “uninsured ineligible for monetary help,” although a few of them are prone to have affords of protection that exceed 9.78% of their earnings, and therefore can be eligible for subsidies to assist buy Market plans.

Unsubsidized premiums used on this evaluation are the total worth of plans, quite than particularly the portion that covers important well being advantages (EHB). Since premium tax credit can solely be used to cowl the EHB portion of premiums, a number of the people denoted as gaining access to a “free” bronze plan may really should pay a really small premium for non-essential well being advantages in the event that they enrolled in a bronze plan with added advantages. The ACA doesn’t allow federal subsidies to pay for abortion protection and requires plans to gather a minimum of $1.00 per 30 days for this protection. In CA, IL, NY, ME, OR, and WA, state legislation requires that that each one state regulated plans embody abortion protection. Policyholders who stay in these states should pay the abortion surcharge although they could qualify for subsidies that present the total price of premiums in the event that they choose a bronze plan. Windfall Well being Plans in OR and WA have a non secular exemption permitting them to exclude abortion protection.

{kind=link}