Michael Vi

It is troublesome to recollect this maxim in a frothy market surroundings, however buyers ought to at all times hold behind their heads that valuation issues. Amid all-time market highs, a rising tide won’t raise all boats: particularly costly shares which are beginning to see their robust basic efficiency unwind.

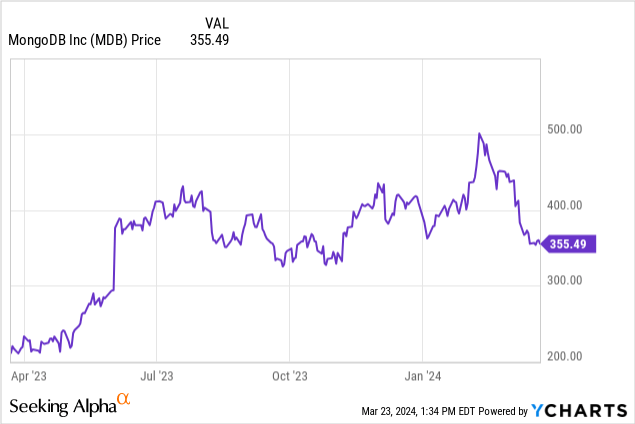

MongoDB (NASDAQ:MDB), sadly, falls into this class. The non-relational database software program vendor has been one of many few tech shares to see a year-to-date decline (albeit modest within the single digits), whereas most of its friends have seen 20%+ features. After peaking briefly in February, shares of MongoDB have slid sharply, particularly after posting disappointing This autumn outcomes and an underwhelming outlook for this 12 months.

I final wrote a bearish article on MongoDB in December, when the inventory was buying and selling nearer to the $410s. Since then, the inventory has dropped practically 20%, and the corporate has additionally launched an outlook for the present 12 months (FY25) that showcases sharp deceleration in income development. Amid these circumstances, I stay bearish on MongoDB.

This is a reminder of all the up to date dangers that I see on this title:

- Deceleration. As soon as considered an organization that would develop at a 40%+ clip indefinitely, MongoDB has surprisingly launched an FY25 outlook that requires a slippage to simply low-teens development charges.

- Weaker utilization traits. MongoDB costs by utilization and by workload, and analysts have referred to as out that MongoDB’s utilization charges haven’t seen a bounce again like some opponents have.

- Not including as many shoppers as prior to now. Leads to MongoDB Atlas have additionally sparked concern, particularly as net-new buyer additions sluggish relative to the tempo from current quarters.

- Losses on a GAAP foundation are nonetheless large, and with development slowing down, the chance to scale with working leverage had minimized. Although MongoDB has notched constructive professional forma working and web revenue ranges, the corporate remains to be burning by giant GAAP losses due to its reliance on stock-based compensation. In increase instances buyers could look the opposite method, however on this extra cautious market surroundings MongoDB’s losses could stand out.

- Competitors. MongoDB could have referred to as itself an “Oracle killer” on the time of its IPO, however Oracle (ORCL) can also be making headway in autonomous and non-relational databases. Given Oracle’s a lot broader software program platform and ease of cross-selling, this may increasingly ultimately lower into MongoDB’s momentum.

From a valuation perspective; regardless of these dangers and the current slide, MongoDB stays fairly costly. At present share costs close to $355, MongoDB trades at a market cap of $25.89 billion. After we web off the $2.01 billion of money and $1.14 billion of convertible debt on MongoDB’s most up-to-date steadiness sheet, the corporate’s ensuing enterprise worth is $25.02 billion.

In the meantime, for the present fiscal 12 months FY25, MongoDB’s steering requires simply $1.90-$1.93 billion in income, or a development vary of 13-15% y/y:

MongoDB FY25 outlook (MongoDB This autumn earnings launch)

This places MongoDB’s valuation at 13.1x EV/FY25 income – a steep ask for an organization whose development is anticipated to decelerate to the kids this 12 months.

After all, it is true that MongoDB does have a historical past of setting its bar low and beating it later: however there are a variety of macro headwinds working in opposition to the corporate, from headcount compression in G&A capabilities to a crackdown on IT spending, in addition to greater scrutiny on signing new prospects and offers. I’d flip a purchaser of MongoDB shares if it fell to 9.5x EV/FY25 income, implying a worth goal of $262: which is ~26% draw back from present ranges and roughly the place MongoDB was buying and selling in early 2023 earlier than it rallied.

The underside line right here: MongoDB’s current slide is greater than justified attributable to its expectations of deceleration. And regardless of this draw back, it isn’t fairly time to purchase the dip simply but. Stay on the sidelines and anticipate a 20%+ additional correction earlier than shopping for in.

This autumn obtain

Let’s now undergo MongoDB’s newest quarterly ends in higher element. The This autumn earnings abstract is proven beneath:

MongoDB This autumn outcomes (MongoDB This autumn earnings launch)

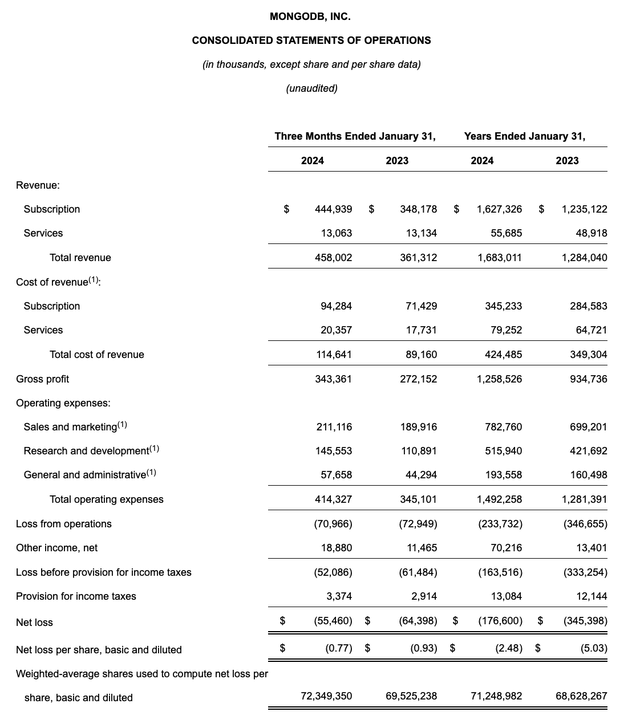

Income grew 27% y/y to $458.0 million, forward of Wall Road’s expectations of $435.6 million (+21% y/y) by a powerful six-point margin. Do observe, nevertheless, that income development decelerated from 30% y/y development in Q3.

Now, observe that MongoDB did pull again on including gross sales capability in FY23 given macro circumstances. Administration now believes it’s considerably below penetrated in its market and plans to extend its go-to-market investments in FY25. It’s particularly centered on doubling the scale of its “strategic account” program and focusing on its largest accounts.

Consumption was in-line with expectations, with a seasonal low anticipated in This autumn. Per CFO Michael Gordon’s remarks on the This autumn earnings name:

Let me present some further context on Atlas consumption within the quarter. As we shared in our steering final quarter, we have been anticipating consumption to be impacted by the seasonal slowdown in This autumn across the holidays. Week-over-week consumption development in This autumn was stronger than in This autumn of final 12 months and in step with our expectations. We have seen much less consumption variability this 12 months, and in order in Q3 we forecasted much less of a seasonal influence than in prior years and that is precisely what we noticed […]

Turning to buyer development, throughout the fourth quarter, we grew our buyer base by roughly 1,400 prospects sequentially bringing our whole buyer rely to over 47,800, which is up from over 40,800 within the year-ago interval. Of our whole buyer rely, over 7,000 are direct gross sales prospects, which compares to over 6,400 within the year-ago interval. The expansion in our whole buyer rely is being pushed primarily by Atlas, which had over 46,300 prospects on the finish of the quarter, in comparison with over 39,300 within the year-ago interval. It is vital to take into account that the expansion of our Atlas buyer rely displays new prospects to MongoDB, along with current EA prospects, including incremental Atlas workloads.”

The corporate notes that development in FY25 will face two troublesome compares. First: FY24 income benefited from $40 million (roughly 2% of annual income) of unused Atlas commitments; of which there will probably be zero in FY25. It is a results of MongoDB’s change to its gross sales incentive construction, which diminished the significance of upfront commitments. Secondly, MongoDB additionally acknowledged about $40 million in multi-year offers in FY24 that it isn’t anticipating to repeat in FY25.

It is also value noting that since these powerful compares got here in at a excessive margin in FY24, the corporate is anticipating professional forma working margins to scale back in FY25. Its excessive finish steering vary requires $201 million of professional forma working revenue, or a ten% margin of its excessive finish income: versus a 16% professional forma working margin in FY24.

Key takeaways

We have now to ask ourselves critically: why pay a premium valuation a number of for an organization that faces powerful comps in FY25, and expects each income development and working margins to say no from FY24 ranges?

In my opinion, there’s extra danger right here that can materialize. Control this inventory on your watch listing, however be affected person and anticipate an extra slide earlier than shopping for in.

{kind=link}