With the 2023 Market Open Enrollment now underway in all states, many are centered on the roll out of the so-called “household glitch” repair as one of many new adjustments to look at on this tenth Market Open Enrollment. Some shoppers with entry to employer-sponsored household protection with excessive premiums will for the primary time be capable of enroll in Market plans with monetary help (premium tax credit and value sharing reductions) that may make this protection extra inexpensive to them than their employer-sponsor protection. Nevertheless, navigating Market eligibility and enrollment necessities is sophisticated even with out the brand new guidelines on the household glitch. This Difficulty Temporary appears to be like at a number of the challenges shoppers can anticipate to face in deciding whether or not to benefit from the household glitch repair.

Affordability and Employer Protection

Eligibility for premium tax credit within the Market relies on an individual’s family revenue and whether or not they have a suggestion of “inexpensive” employer-sponsored protection (amongst different elements). Nevertheless, for relations of working people, affordability till now was primarily based solely on the price of self-only protection obtainable to the employee; the added premium for relations was not thought-about. That interpretation, adopted in 2013, is usually known as the “household glitch.” In 2022, the common annual premium for employer-sponsored household medical insurance is $22,463, whereas the common value of self-only protection is $7,911. Underneath the “household glitch”, if, for instance, an employer had paid the whole premium for staff’ self-only protection however contributed nothing towards the added value of enrolling relations, the employees’ relations would nonetheless have been thought-about to have an inexpensive supply of employer-sponsored protection, stopping them from getting monetary help for Market protection.

Underneath new federal rules revealed this fall, the employee’s required premium contributions for self-only protection and for household protection will probably be in comparison with the affordability threshold of 9.12% of family revenue. If the price of self-only protection is inexpensive, however the fee for household protection isn’t, the employee won’t be eligible for Market monetary help, however her relations can apply for this help. If employers supply a alternative of plans, the bottom value choice with an actuarial worth of at the least 60% (the ACA “minimal worth” normal) is used to judge affordability. (An actuarial worth of 60% means the plan covers 60% of the price of coated advantages on common for a typical group of enrollees, with the rest being paid by sufferers by means of deductibles, copays, and coinsurance.)

People decided eligible for Market premium tax credit may also apply for value sharing reductions in the event that they enroll in a Silver plan and usually have a family revenue between 100 and 250 p.c of the poverty degree (between $23,030 and $57,575 for a family of three for 2023). Value sharing reductions will decrease a shopper’s out-of-pocket prices comparable to deductibles, copayments or coinsurance. The quantity of the fee sharing discount is set on a sliding scale primarily based on revenue. These in value sharing discount plans will even have a decrease annual out-of-pocket restrict than the utmost quantity allowed beneath ACA guidelines ($9,100 particular person and $18,200 household for 2023).

KFF estimated that greater than 5.1 million individuals fell within the ACA household glitch. KFF additionally estimates that 85% of those individuals (4.4 million) are at present enrolled by means of employer-sponsored insurance coverage and are possible spending extra for protection than people with related incomes would pay in premiums for backed Market protection. Customers affected by the household glitch may very well be spending on common 15.8% of their revenue on their employer-based protection in keeping with one examine. Against this, the ACA affordability threshold for employer protection in 2023 is 9.12% of revenue—a person spending greater than 9.12% of their revenue in premium contributions for her employer protection is taken into account to have unaffordable protection and is eligible for Market subsidies.

Implementing the Household Glitch Repair

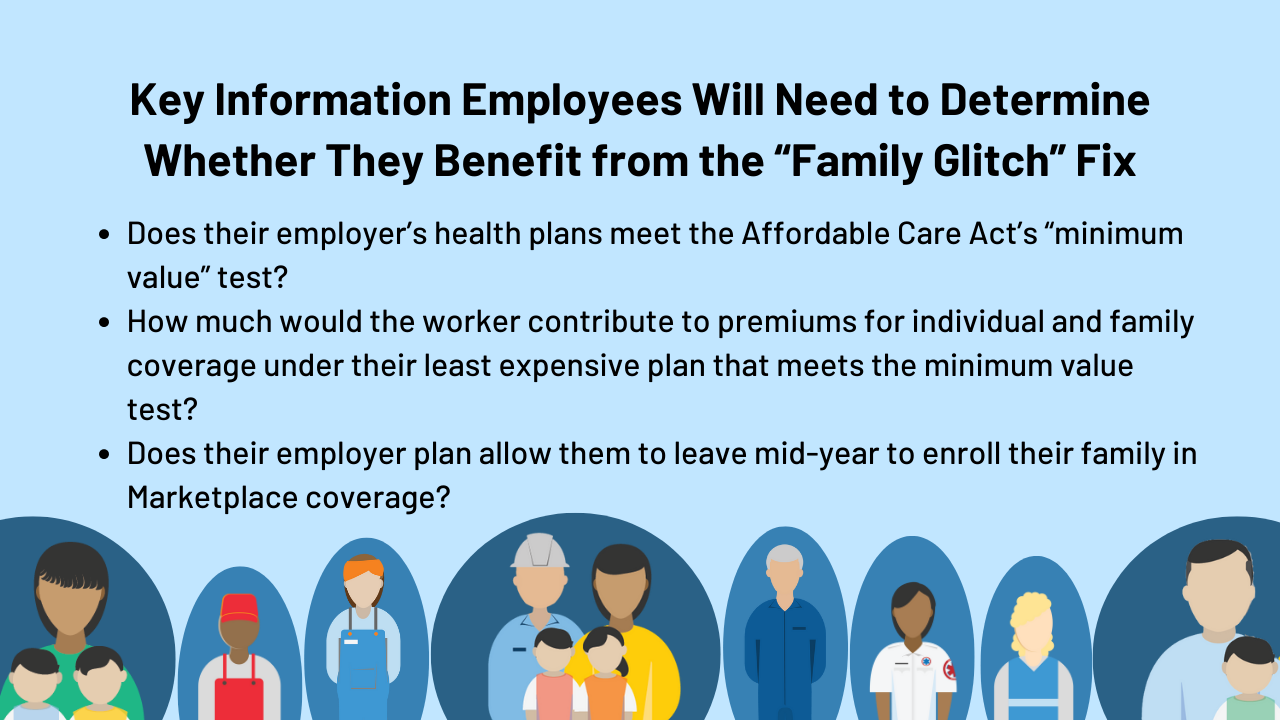

Now that the ultimate regulation has been modified and the worker contribution towards household protection is taken under consideration to find out affordability, what can shoppers anticipate as they contemplate enrolling in a Market Plan with monetary help?

Customers want info from their employer

One stumbling block for some staff would be the want to hunt particular info from their employer earlier than they will even consider whether or not it is smart to enroll their households in Market protection with monetary help. There isn’t a requirement for an employer to supply this info to their staff, placing the onus on staff to attempt to collect it. To help shoppers in gathering a few of this info, the federal trade has up to date its “Employer Protection Instrument,” which staff can take to their employer and request them to supply details about protection eligibility, value and minimal worth. Customers can use this software to finish their Market software. (Desk 1)

| Info Wanted | Why Wanted? | The place can shopper get it? |

| Do employer-sponsored well being plan choices meet the check of “minimal worth” | The ACA affordability check is barely utilized to employer plans that provide “minimal worth,” that means they’ve an actuarial worth of at the least 60% and supply substantial protection for hospitalization and doctor companies | Customers can ask their employer for this info. Alternatively, the Abstract of Advantages and Coated (SBC) for the related plan choice, should point out whether or not it meets the minimal worth threshold |

| What’s the worker’s premium contribution (for self-only and for household protection) for the bottom value plan choice that meets minimal worth | This info is required to find out whether or not a employee must pay greater than the affordability threshold —9.12% of family revenue for 2023—for household protection | The employer is the one supply for this info. Many corporations publish the required worker contribution for all plan choices in the course of the employer’s open enrollment interval. Different employers may not present this info mechanically, requiring the worker to ask for it |

| Will the employer-sponsored plan enable an worker to revoke protection for his or her household mid-year in an effort to enroll the household in a Market plan | Workers and/or relations enrolled in employer protection might want to disenroll in an effort to enroll in Market protection for 2023 | Every employer plan sponsor decides whether or not they’ll enable staff to revoke protection. Customers might want to discover out what guidelines their employer makes use of. If the employer doesn’t enable disenrollment, the relations can’t entry monetary help for Market protection |

IRS guidelines usually require employer-plan members to pick their protection choice earlier than the start of the plan 12 months. After that, employers are solely required to allow mid-year adjustments following particular qualifying occasions. This may make it troublesome to coordinate Market enrollment with employer protection disenrollment. For example, an employer might have a plan 12 months that doesn’t start in January (a non-calendar 12 months plan), through which case Market open enrollment wouldn’t coincide with the employer’s open enrollment. New and current IRS steerage give employers the selection (whether or not they have a calendar 12 months or non-calendar 12 months plan) to permit the worker or family members to revoke their employer protection and disenroll mid-year if, because of the household glitch repair, they’re newly eligible for Market monetary help. Employers would wish to amend their well being plans to permit this disenrollment.

Many employers may not know that they need to take motion to permit staff to revoke protection in an effort to benefit from the glitch repair for his or her households. Whereas employers wouldn’t have to permit this revocation, in most circumstances it will not adversely have an effect on the employer. Permitting a partner and a dependent to enroll in backed Market protection, for example, doesn’t trigger an employer to violate the ACA’s employer mandate. Some employers might discover value financial savings in permitting these relations to disenroll since they’re now not overlaying these relations.

Customers have complicated decisions to judge

Even when a shopper can get the data that they want in a well timed method, a extra inexpensive premium for Market protection is just one merchandise to think about in deciding to enroll:

- “Break up” households. The glitch repair doesn’t have an effect on the affordability rule for the employee, just for the employee’s family members. If employer protection is inexpensive for the worker however not relations, the worker would possibly nonetheless keep in her employer protection, whereas her dependents enroll in a Market plan. This “break up” household state of affairs means the household may have two plans, with separate (and certain completely different) deductibles and out-of-pocket limits and completely different supplier networks. Additionally, an worker may determine to enroll alongside together with her household in Market protection. Nevertheless, as a result of the worker wouldn’t be eligible for premium tax credit, her share of the household premium wouldn’t be backed. As well as, if her household would in any other case be eligible for value sharing reductions, the relations must enroll in a separate Silver market plan from the worker beneath current value sharing discount guidelines.

- Networks and value sharing.

- Variations in plan supplier networks. The breadth of supplier networks for Market protection may not be as strong as these in a typical employer plan. Customers might want to examine whether or not they can nonetheless see their current suppliers of their new Market plan.

- Variations in cost-sharing: These not eligible for value sharing reductions can also discover greater deductibles and out-of-pocket maximums then they’d of their employer protection. For instance, the common per-person deductible in job-based plans in 2022 was $1,763, in comparison with $4,753 beneath the common Market Silver plan that 12 months.

Concerns going ahead

CMS has already ramped up outreach to related stakeholders to supply coaching on the household glitch repair. Time will inform whether or not extra is required to guarantee that the household glitch repair is carried out in order that affected people can entry this profit. Simpler methods to entry details about employer value and protection could also be one space to judge to alleviate the present complexity. As policymakers consider how finest to make inexpensive protection extra accessible in our fragmented well being protection system, implementation of the household glitch is one clear space the place educated help is clearly vital to assist shoppers.

{kind=link}