designer491

Funding Thesis

“Workplace properties”, the title in itself is sufficient to scare traders lately. We utterly share the concern based mostly on the long-term outlook of workplace properties, however NYSE:NLOP is a particular state of affairs. We don’t have to carry these properties as a going concern.

NLOP’s sole goal is to liquidate these workplace properties whereas leveraging the asset administration experience of WPC as its advisor. Subsequently, we don’t have to fret concerning the long-term earnings potential and solely give attention to the liquidation worth of those properties.

Trying on the earlier gross sales and the implied cap. charge within the inventory, we consider the corporate is buying and selling under its liquidation worth and price a glance.

Evaluation

W. P. Carey spun off their undesirable workplace properties with the aim of liquidating that portfolio below the administration of NLOP. Since W. P. Carey retained a number of the workplace properties, the basic notion was that NLOP is getting the worst high quality property. The properties retained by W. P. Carey had a WALT (Weighted common Lease time period) of 10.85 years, 6m sqft. and $12.83 ABR (Annualised Base Lease) per sqft.

Properties spun-off to NLOP had a WALT of 5.7 years, 8.7m sqft. and $16.2 ABR per sqft. Retained Properties clearly had an extended WALT, nevertheless it’s not the one factor which impacts the valuation. NLOP Properties with increased ABR per sqft. assures us that they aren’t as unhealthy high quality as initially anticipated. Due to this, for the reason that preliminary fall within the inventory after the spinoff, NLOP has doubled in inventory worth.

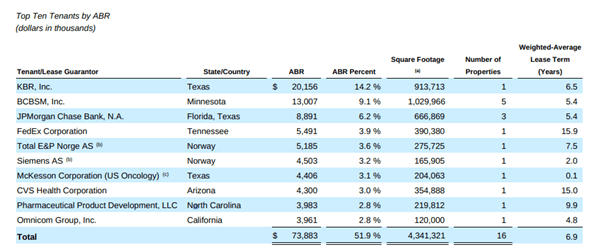

NLOP started buying and selling with 59 properties below their portfolio with 97% occupancy. These are properly diversified by each trade and geographically, with 54% of the tenants having funding grade ranking and accountable for 66% of the ABR. Since inception, the corporate has parted methods with 10 properties, 7 outright gross sales, one undisclosed UK property sale and two switch of mortgages. NLOP has 49 properties now with three of them being in Europe.

There was additionally an thought from WPC of strategically renewing sure expiring leases to extend property values. This together with the money flows from operations is one thing that the traders mustn’t overlook, NLOP’s producing $69m of cashflows annually. Since NLOP has quite a lot of mortgage commitments, we gained’t be utilizing this cashflow in our valuation.

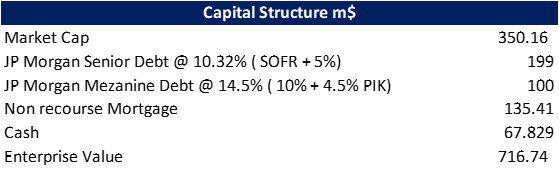

The capital construction of NLOP could be very costly and that’s why the administration is pursuing to repay that first from the proceeds of the gross sales.

Since a number of the debt has been paid for from the latest gross sales, under desk highlights our estimate of the capital construction.

Moat Investing

NLOP has a triple web lease construction and nearly all of their value construction is variable in nature, so bills lower as properties are bought.

Because the solely objective of NLOP is liquidating its portfolio, the principle query and level of research is how a lot that portfolio is value in right now’s market. That is very onerous to reply, however NLOP’s market cap implies extraordinarily pessimistic assumptions, which might create a margin of security.

Moat Investing

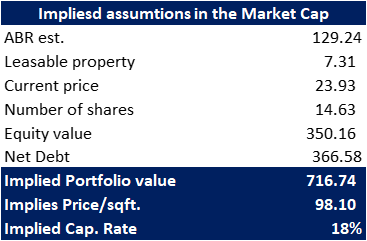

ABR, Leasable property space, and Internet debt is adjusted for the latest sale of properties. The implied cap charge available in the market is eighteen%, with a worth per sqft of $99 and a portfolio worth of $723m. Though 18% implied cap charge can increase many eyebrows, this alone isn’t sufficient, we have to examine it with the latest gross sales of properties.

Moat Investing

The latest gross sales spotlight that the implied assumptions available in the market are very unfair and pessimistic. The seven properties bought had a mean cap charge of 10% and a mean worth per sqft of $162.82. Now, an argument right here will be that these properties had been cherry-picked by the administration to spice up investor confidence. To some extent, this does appear to be the case if you take a look at the WALT and credit standing of those properties. Though there’s yet another argument right here which may give a little bit of confidence on the costs realized, JPMorgan had a mean implied valuation of $163 on its mortgage portfolio which on the time represented 68% of NLOP’s complete portfolio.

NLOP-Data Assertion

We perceive that we can not depend on JPM’s quantity, or the sale worth realized, however this highlights how depressed is the worth implied available in the market cap of $99/sqft.

To spotlight how minimal the draw back danger is, If we take a look at the earlier gross sales of properties, the best cap charge was on a property in Norway. Even in case you use that cap charge to worth all the portfolio, you’d nonetheless have an upside of 24%.

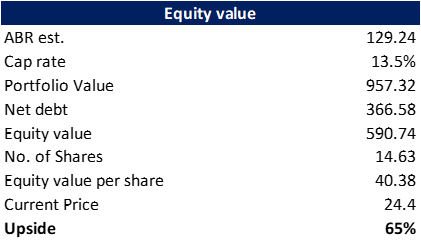

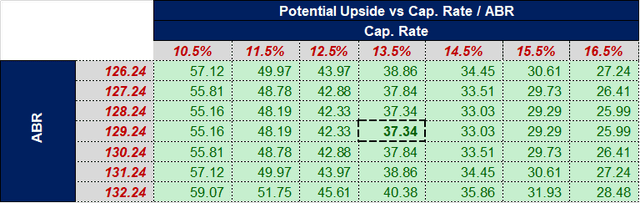

Given the dangers, we consider the cap charge of 13.5% is affordable. At 13.5% we get an upside of 60% and an implied gross sales worth per sqft. of $131.2. The desk under will take you thru the calculations.

Moat Investing

Dangers

Period danger is probably the most important danger right here. The longer they take to promote the properties, the extra the curiosity bills and reducing WALT will eat up the liquidation worth.

With 25% of the leases expiring within the subsequent two years, there’s a danger that NLOP may discover it onerous to promote or re-lease these properties.

Rate of interest danger additionally impacts the valuation. If rate of interest stays increased for longer, the residual worth of NLOP will be impacted.

Tenant focus additionally looks like a major danger initially, with 29% of ABR coming from the highest 3 tenants. However in case you take a look at the WALT of those tenants, solely McKesson was a danger which has already vacated in Q1 of this 12 months. The second and third-lowest WALT is 2 years and 4.8 years respectively. This might have been a danger if we had been valuing the corporate on a going concern foundation.

Moat Investing

Situation Evaluation

Now we have carried out a state of affairs evaluation on the principle worth driver affecting our valuation, i.e., Completely different Cap charges. Completely different ABR’s spotlight emptiness danger.

Beneath desk helps us in understanding how NLOP’s asset worth per share performs below completely different stress eventualities.

Moat Investing

Conclusion

We consider NLOP is a really fascinating liquidation play with a possible upside of 65%. Given the dangers of upper rates of interest for longer, increased cap charges and delayed gross sales, we consider the cap charge implied within the inventory worth nonetheless offers us sufficient margin of security, this can be confirmed by wanting on the sensitivity desk.

{kind=link}