Yuji Sakai

The Excessive Revenue Securities Fund (NYSE:PCF) is a closed-end fund that many income-focused traders make use of as a technique of attaining their objectives of receiving a big quantity of present earnings from their property. On the floor, the fund actually seems to do very effectively right here, as its 11.64% present yield is likely one of the highest yields out there out there immediately. The fund’s yield compares fairly effectively to that of its friends:

|

Fund Identify |

Morningstar Classification |

Present Yield |

|

Excessive Revenue Securities Fund |

Fastened Revenue-Taxable-Convertibles |

11.64% |

|

Creation Convertible & Revenue Fund (AVK) |

Fastened Revenue-Taxable-Convertibles |

11.78% |

|

Calamos Convertible & Excessive Revenue Fund (CHY) |

Fastened Revenue-Taxable-Convertibles |

10.73% |

|

Ellsworth Progress and Revenue Fund (ECF) |

Fastened Revenue-Taxable-Convertibles |

6.65% |

|

Virtus Convertible & Revenue Fund (NCV) |

Fastened Revenue-Taxable-Convertibles |

12.63% |

I’ll admit that I’m not sure that calling the Excessive Revenue Securities Fund a convertible securities fund is suitable. As we are going to see on this article, this fund invests in quite a lot of completely different high-yielding securities that aren’t convertible bonds or convertible preferreds. Nevertheless, the identical can in all probability be stated about just a few of the opposite funds on this listing and I’ve at all times used Morningstar’s classification system for conducting peer comparisons of closed-end funds, so there isn’t any motive to cease that now. As we are able to see, the Excessive Revenue Securities Fund at present has a yield that’s similar to that of its friends, however it’s actually not the highest-yielding fund right here. After all, the Virtus Convertible & Revenue Fund, which is the one one which beats the Excessive Revenue Securities Fund by a big margin, has quite a few issues and has typically dissatisfied most of its traders over the previous few years. As such, risk-averse traders and retirees may favor the Excessive Revenue Securities Fund regardless of its decrease yield.

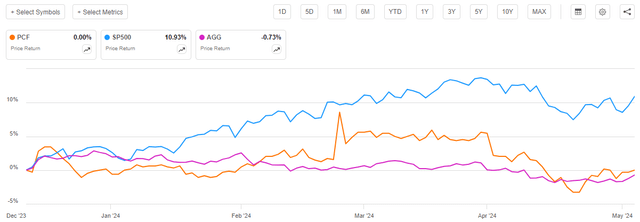

As common readers can possible keep in mind, we beforehand mentioned the Excessive Revenue Securities Fund in the course of December. The market since that point has typically been weak for many bond funds, however widespread equities have held up fairly okay, as have most closed-end funds. For its half, the Excessive Revenue Securities Fund has been utterly flat for the reason that date that the prior article was printed:

Looking for Alpha

Admittedly, the share worth has bounced round a bit since that date, but it surely has not been practically as unstable because the S&P 500 Index (SP500). It did, nevertheless, considerably underperform the index when taking a look at share worth alone. This isn’t actually shocking although, since earnings securities typically will normally underperform widespread shares in a bull market. The fund did handle to outperform investment-grade bonds, although, which is actually good to see.

Nevertheless, as I identified in a earlier article:

A easy have a look at a closed-end fund’s worth efficiency doesn’t essentially present an correct image of how traders within the fund did throughout a given interval. It is because these funds are inclined to pay out all of their web funding earnings to the shareholders, reasonably than counting on the capital appreciation of their share worth to offer a return. That is the explanation why the yields of those funds are usually a lot larger than the yield of index funds or most different market property.

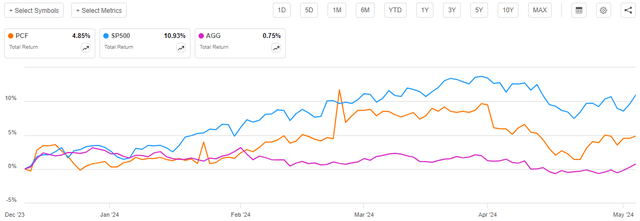

We noticed the excessive yield of this fund mirrored within the first paragraph of this text. The Excessive Revenue Securities Fund’s 11.64% present yield is considerably larger than the 1.31% trailing twelve-month yield of the S&P 500 Index (SPY). The fund’s distribution is even larger than the 6.59% trailing yield of the home junk bond index (JNK). Thus, we are able to anticipate that it’s going to enhance the funding return that traders obtain by fairly a bit. Certainly, once we embody the results of the fund’s distributions within the above chart, we get this one:

Looking for Alpha

As we are able to clearly see, traders within the Excessive Revenue Securities Fund realized a 4.85% whole return for the reason that date that my earlier article on this fund was printed. That is, undoubtedly, nonetheless worse than the overall return that would have been realized by buying an S&P 500 Index fund on the identical date, but it surely is much better than investment-grade bonds delivered. The fund even managed to beat investment-grade bonds once we included the influence of the coupon funds made by these bonds over the identical interval. Thus, the fund might be a more sensible choice for traders than a secure bond fund, however the fact is that investment-grade bonds have been fairly poor investments for fairly a while, as we are able to see by trying on the whole return of all three of those investments over the previous ten years:

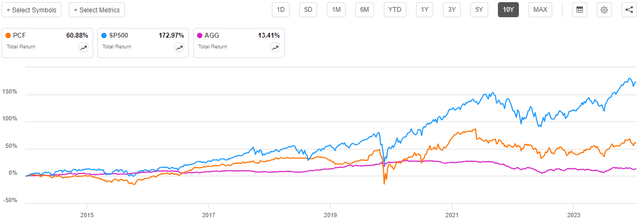

Looking for Alpha

As anticipated, widespread shares considerably beat the Excessive Revenue Securities Fund over the previous decade, even once we embody the distributions that have been paid out by this fund. Nevertheless, it as soon as once more proves that it is much better than investment-grade bonds, which have traditionally been one of the vital fashionable investments for conservative traders.

About The Fund

As I identified in my earlier article, the fund’s webpage is extraordinarily spartan. From the earlier article:

The web site for the Excessive Revenue Securities Fund will be discovered right here, but it surely consists of very restricted details about the fund. The truth is, that is in all probability the one fund that doesn’t publish a truth sheet on the web site, nor does it embody any details about the fund’s efficiency. It does nonetheless have the fund’s monetary statements and quarterly holdings studies which might be required by Securities and Trade Fee rules. We’ll subsequently be pressured to depend on these paperwork in addition to exterior sources for our evaluation.

On the time that the earlier article was printed, the newest monetary report that was out there was the fund’s annual report for the full-year interval that ended on August 31, 2023. The fund has since launched a more moderen doc, which corresponds to the six-month interval that ended on February 29, 2024. Clearly, the time limit on the monetary statements and holdings data that may be discovered listed below are solely two months outdated, so it ought to have the ability to present us with an excellent replace on what this fund is doing with the cash that its traders have entrusted to it.

The fund’s semi-annual report describes its technique thusly:

Typically, the fund invests in securities of discounted shares of income-oriented closed-end funding firms, enterprise growth firms and Particular Objective Acquisition Automobiles.

The acknowledged technique of investing in different closed-end funds at a reduction is just like the technique utilized by a few of the fashionable Saba Capital funds just like the Saba Capital Revenue & Alternatives Fund (BRW). For essentially the most half, it’s a technique that income-oriented traders can admire. In spite of everything, as I identified within the introduction to this text, many closed-end funds are inclined to have far larger yields than anything out there. These excessive yields present this fund with a considerable stage of earnings that may then be paid out to its personal shareholders. As well as, by buying the fund at a reduction, the Excessive Revenue Securities Fund may have the ability to notice some capital good points merely by means of the closing of the low cost. The Saba Closed-Finish Funds ETF (CEFS) explains on its web site how this may work:

CEFS seeks to outperform index-based closed-end fund merchandise by actively buying and selling the portfolio to seize the widening and narrowing of reductions to web asset worth.

As we now have seen in quite a few earlier articles, closed-end funds sometimes commerce at a market worth that’s decrease than the worth of the property contained within the underlying portfolio. The distinction between the market worth and the underlying portfolio worth steadily adjustments. For instance, there have been a number of income-focused funds which have delivered a share worth efficiency that has far exceeded the efficiency of the particular portfolio over the previous six months. I’ve pointed this out in just a few articles on funds during which this has occurred. The Excessive Revenue Securities Fund is presumably making an attempt to reap the benefits of this situation, which permits it to earn some capital good points along with the efficiency of the underlying portfolio of the respective closed-end funds during which it invests. In spite of everything, the Excessive Revenue Securities Fund is an actively managed fund, so it is a logical technique for it to make use of.

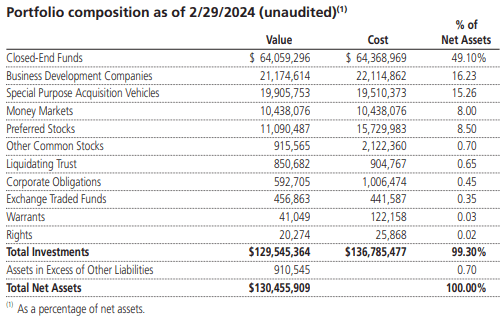

Right here is how the fund’s asset allocation regarded on February 29, 2024:

Fund Semi-Annual Report

We will see that different closed-end funds accounted for the biggest single weighting within the portfolio of the Excessive Revenue Securities Fund. Nevertheless, different closed-end funds are nonetheless a minority holding within the fund, as there isn’t any single place right here that accounts for greater than 50% of the fund’s holdings. The fund has considerably elevated its weighting to closed-end funds in comparison with the final time that we mentioned it, although. Right here is how the fund’s asset allocation immediately compares to the way it regarded again in August:

|

Asset Sort |

February 29, 2024 |

August 31, 2023 |

|

Closed-Finish Funds |

49.10% |

44.88% |

|

Enterprise Improvement Corporations |

16.23% |

18.50% |

|

Particular Objective Acquisition Automobiles |

15.26% |

13.08% |

|

Cash Markets |

8.00% |

12.21% |

|

Most well-liked Shares |

8.50% |

9.55% |

|

Different Widespread Shares |

0.70% |

1.03% |

|

Liquidating Belief |

0.65% |

0.23% |

|

Company Obligations |

0.45% |

0.45% |

|

Trade-Traded Funds |

0.35% |

N/A |

|

Warrants |

0.03% |

0.07% |

|

Rights |

0.02% |

0.01% |

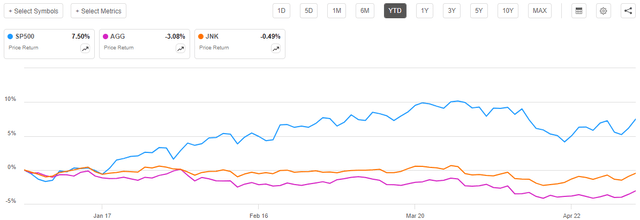

The largest adjustments that we see listed below are that the fund considerably decreased its cash market property and elevated its weighting to closed-end funds. This isn’t shocking in any respect. A cash market fund yields 5.20% or so at finest, and there are many closed-end funds with considerably larger yields. As such, it makes little or no sense to be holding money in a cash market versus closed-end funds besides within the case of a widespread bear market (during which the cash market holdings are merely an try to scale back losses). On the finish of August, the value of most issues within the capital market was declining whereas yields have been rising. A big allocation to money might need made sense in such an atmosphere, because it was higher than making an attempt to catch a falling knife. Nevertheless, since that point the market has typically improved and whereas yields have been rising year-to-date, we now have not seen a widespread sell-off like we did in the course of the summer time of 2023. The truth is, the one factor that’s actually down year-to-date is investment-grade bonds:

Looking for Alpha

Thus, it makes a lot much less sense to favor money over a higher-yielding closed-end fund immediately than it did again in August.

The opposite vital change that we see within the fund’s portfolio over the August to February interval is that the fund decreased its place in enterprise growth firms with a purpose to enhance its weighting to particular function acquisition autos. I’ve a lot much less confidence on this change than I did within the earlier one.

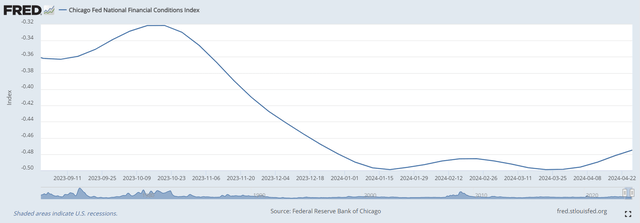

The discount in enterprise growth firm holdings may make sense given the notion of Federal Reserve coverage that existed in the course of the interval during which the change occurred. Many enterprise growth firms make loans to their shopper firms on a floating-rate foundation that’s normally based mostly on some unfold above short-term U.S. Treasury securities. As such, a discount within the federal funds charge will usually scale back the earnings of enterprise growth firms and even scale back the distributions that they’re able to pay out. The Federal Reserve has been telegraphing that rate of interest reductions can be coming for some time now, regardless of the inflation knowledge suggesting that rate of interest cuts can be a really dangerous thought. The market has reacted to the Federal Reserve’s statements although and loosened monetary circumstances considerably over the interval:

Federal Reserve Financial institution of St. Louis

This could counsel {that a} fixed-income closed-end fund might need been in a position to outperform a enterprise growth firm over the interval. Nevertheless, that concept doesn’t seem to have essentially performed out the best way that the fund’s administration hoped.

For instance, allow us to check out the overall returns (together with dividends and distributions) produced by two of the most well-liked enterprise growth firms, Ares Capital (ARCC) and PennantPark Funding Company (PNNT) over the interval:

Looking for Alpha

The chart above compares every of those enterprise growth firms to the BlackRock Core Bond Belief (BHK) and the BlackRock Company Excessive Yield Fund (HYT), which ought to give a good suggestion of how the enterprise growth firms in comparison with investment-grade and junk bond closed-end funds. We will see clearly that the investment-grade bond fund considerably underperformed, however the junk bond fund and Ares Capital have been fairly shut when it comes to whole return. PennantPark Funding Company, which just about totally offers floating-rate financing, outperformed all the different property by quite a bit.

Thus, it seems that the Excessive Revenue Securities Fund’s divestment of enterprise growth firms within the hopes of getting higher returns elsewhere could not have performed out in addition to administration hoped once they made that commerce.

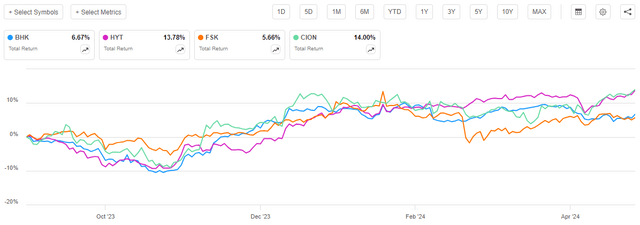

With that stated, the precise efficiency offered by varied enterprise growth firms diverse rather a lot over the interval. The enterprise growth firms held by the fund additionally delivered vastly completely different performances. The 2 largest enterprise growth firm positions within the fund’s portfolio on February 29, 2024, have been FS KKR Capital (FSK) and CION Funding (CION). Right here is how these two firms carried out over the interval:

Looking for Alpha

CION Funding actually did alright, because it roughly matched the efficiency of the junk bond closed-end fund. Nevertheless, FS KKR Capital was not holding for the fund. It underperformed even an investment-grade closed-end bond fund, not to mention considerably underperforming CION Funding and PennantPark (which was not within the fund’s portfolio on February 29, 2024).

Thus, the fund might need benefited from eliminating a few of the enterprise growth firms that it might need had in its portfolio in some unspecified time in the future over the interval. In spite of everything, a few of them underperformed income-producing closed-end funds. In fact, this seems to solid a shadow over the fund administration’s potential to select enterprise growth firms. The concept of switching away sure enterprise growth firms could have made sense if the Federal Reserve had truly minimize rates of interest as quickly because the market anticipated again in December, however that was at all times a pipe dream as the info by no means supported the thought of speedy charge cuts.

Distribution Evaluation

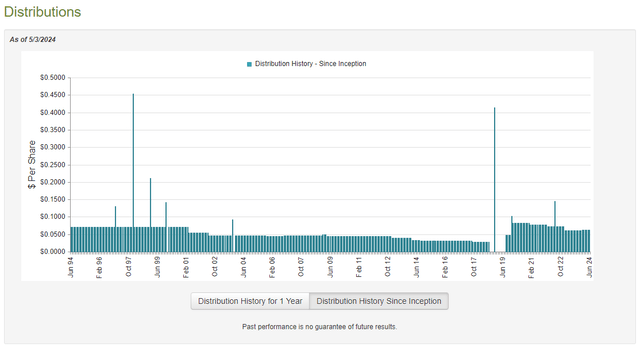

The first motive for anybody to buy shares of the Excessive Revenue Securities Fund is due to the excessive yield that the fund pays out. As of the time of writing, the fund pays a month-to-month distribution of $0.0622 per share ($0.7464 per share yearly), which supplies it an 11.64% yield on the present worth. The fund’s distribution traditionally has been everywhere, although, because it has each raised and lowered it quite a few occasions over its historical past:

CEF Join

The fund’s semi-annual report features a assertion explaining the rationale for this:

The Fund at present pays month-to-month distributions at an annualized charge of at the least 10% (or 0.8333% monthly) of its share web asset worth as of the final enterprise day of the earlier calendar 12 months. Every of the primary two month-to-month distributions in calendar 12 months 2024 have been $0.0622 per share. Please be aware that in some calendar years, adhering to the Fund’s managed distribution coverage could require some capital to be returned to shareholders. The Fund won’t know what share, if any, of its distributions can be characterised as a return of capital till after the tip of the calendar 12 months during which they’re made.

Principally, the distributions are going to closely rely upon the overall return of the property that the fund holds. As lots of this fund’s property present a considerable share of their whole return within the type of dividends and distributions, there could possibly be an oblique hyperlink between rates of interest and the fund’s distributions. In spite of everything, the fund will embody closed-end funds that spend money on floating-rate securities in addition to enterprise growth firms that sometimes pay out bigger distributions when short-term rates of interest are excessive. That might naturally have a optimistic influence on the earnings of the Excessive Revenue Securities Fund, which raises its web asset worth as money is available in. Nevertheless, fixed-rate bond funds normally shoot up in worth when rates of interest decline, which might even have a optimistic influence on the fund’s web asset worth to the diploma to which the fund is holding such property.

Allow us to take a look on the fund’s semi-annual report for the interval that ended on February 29, 2024, in an try to find out how effectively it’s overlaying its distribution that was simply raised in January.

For the six-month interval ending February 29, 2024, the Excessive Revenue Securities Fund acquired $4,268,692 in dividends and $860,009 in curiosity from the securities in its portfolio. This provides the fund a complete funding earnings of $5,128,701 for the six-month interval. The fund paid its distributions out of this quantity, which left it with $4,495,841 for the shareholders. That was, sadly, not ample to cowl the $6,416,150 that the fund paid out in distributions. I’ll admit although that this fund did handle to get nearer than I anticipated to realize full distribution protection solely with web funding earnings.

The fund did handle to make up the distinction by means of capital good points. For the six-month interval, the Excessive Revenue Securities Fund reported web realized good points of $727,924 and web unrealized good points of $1,339,539. The fund’s web property elevated by $147,154 after accounting for all inflows and outflows within the interval.

Thus, this fund did handle to totally cowl the distributions that it paid out in the course of the interval and had cash left over. This actually explains why the fund raised its distribution in January. Nevertheless, the fund did have to depend on unrealized capital good points to cowl its distributions, so there isn’t any assure {that a} market correction won’t render it unable to cowl its payouts. After all, that may be a drawback with a managed distribution coverage typically.

Over the previous ten years, the fund has failed to totally cowl the distributions in mixture:

Barchart

That chart exhibits the web asset worth of the Excessive Revenue Securities Fund over the previous ten years. As we are able to see, it has declined by 21.26% over the interval. This tells us that the fund did not cowl all the distributions that it paid out. Nevertheless, practically all of its issues got here from a failure to totally cowl payouts in 2021 and 2022. Whereas the fund did encounter some issues in 2015, it managed to right them over the subsequent few years. General, although, the long-term historical past of the fund means that traders who’re searching for a secure and constant earnings to make use of to pay their payments could also be higher off trying elsewhere.

Valuation

As of the time of writing, the Excessive Revenue Securities Fund trades at a 13.73% low cost to web asset worth. It is a far more enticing worth than the 9.37% common low cost that the shares have had over the previous month. As such, the present worth appears like a reasonably good entry level.

Conclusion

In conclusion, the Excessive Revenue Securities Fund is a reasonably attention-grabbing fund that seeks to offer a really excessive yield always. The fund seeks to realize this aim by investing in different closed-end funds and enterprise growth firms, each of which normally have fairly excessive yields themselves. Sadly, the fund has typically did not cowl its distributions over the long run and in consequence, its portfolio has misplaced some huge cash. The fund did handle to cowl its distribution throughout the newest six-month interval, nevertheless.

General, the fund might be price holding on to in case you already personal it. The latest report exhibits that the fund has improved rather a lot since our prior dialogue, particularly relating to growing the yield of its property. The truth that it managed to cowl its distribution throughout the newest interval is useful too, even when the long-term pattern is unfavorable.

{kind=link}