Chip Somodevilla/Getty Photos Information

Introduction

The Fed’s Jerome Powell spoke on Wednesday, releasing the March FOMC abstract, which will be discovered right here.

On the press convention that adopted, the opening assertion of which will be discovered right here, Powell made a number of factors very clear:

- We’re certainly at peak charges (one thing I known as again in December)

- There are three projected price cuts this yr

- Sturdy financial knowledge could not halt the cuts

I’m adjusting my fixed-income holdings accordingly, positioning out additional on the yield curve and taking over extra length. On this article, I’ll focus on the Fed’s route, and steerage, and the way we would revenue off the tonal shift we noticed Wednesday.

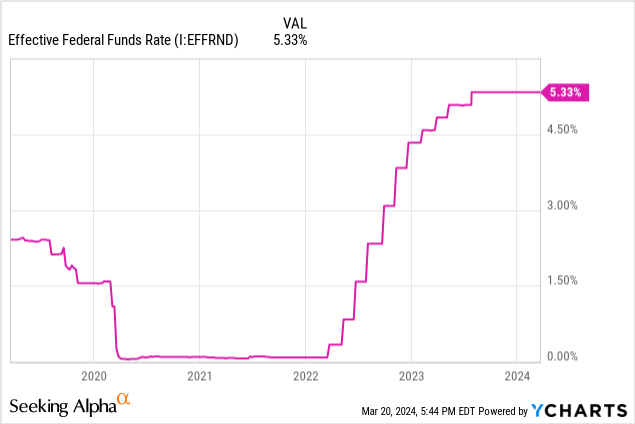

Peak Charges

The efficient Fed Funds price has been on a plateau for the higher a part of a yr and it appears that evidently we’ve been at peak charges because the final hike in July 2023.

That was confirmed by Powell at Wednesday’s assembly when he outright stated it:

We consider that our coverage price is probably going at its peak for this tightening cycle and that, if the economic system evolves broadly as anticipated, it should probably be applicable to start dialing again coverage restraint sooner or later this yr. The financial outlook is unsure, nevertheless, and we stay extremely attentive to inflation dangers. We’re ready to take care of the present goal vary for the federal funds price for longer, if applicable.

It was an actual “have your cake and eat it too” second when Powell proclaimed each the top of price hikes and the start of price cuts in the identical sentence. That is excellent news for bond buyers who’ve time to load up on treasuries on the highest they’re set to go for this cycle.

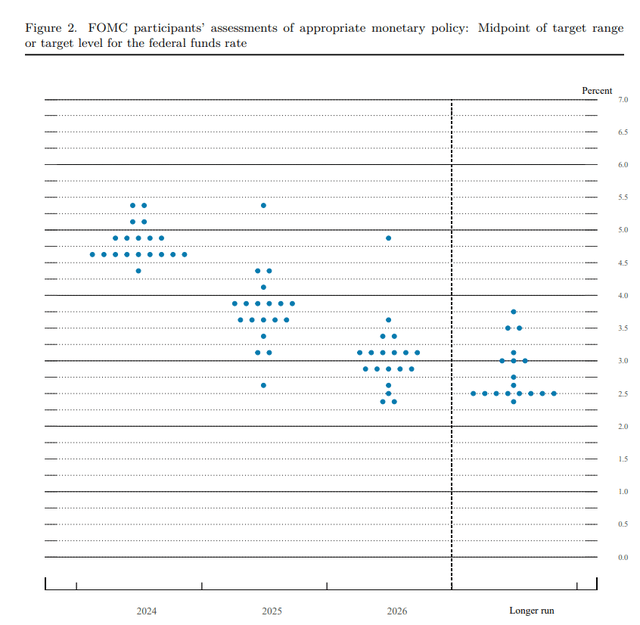

Right here is the “dot plot” the FOMC publishes exhibiting their price projections for the longer term. Every dot is a member of the committee’s projection for that yr’s goal price.

Determine 1 (FOMC)

Lengthy Bondholders Rejoice

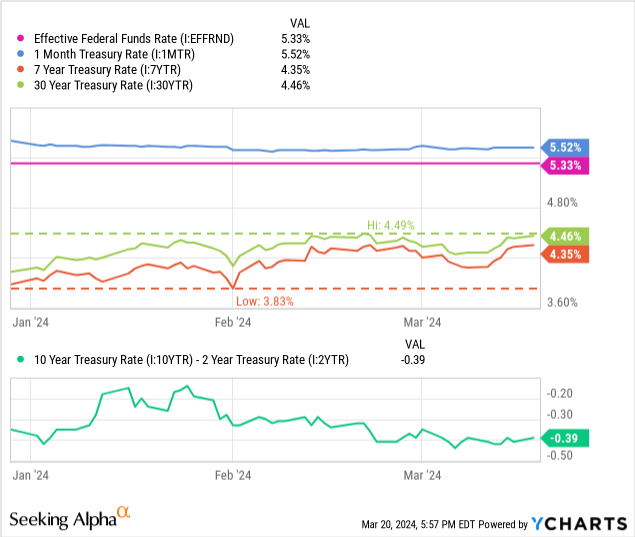

Which means that we’re prone to see lengthy bonds mood their yields within the coming months, probably driving costs again up. The chart under exhibits the YTD adjustments in yields for the 1mo, 7yr, and 30yr US Treasuries. Be aware how the charges are nonetheless round their YTD peaks.

The unfold of the 10yr and 2yr bonds remains to be destructive, that means that our yield curve remains to be inverted. It’s unlikely to invert any additional, since that might require an expectation of even larger short-term charges than 5.52%.

Determine 2 (US Treasury)

That is the best purchase sign that buyers can count on within the US bond market. Powell is telling us that charges won’t rise and that he intends to, inside this yr, take us down a minimum of three notches.

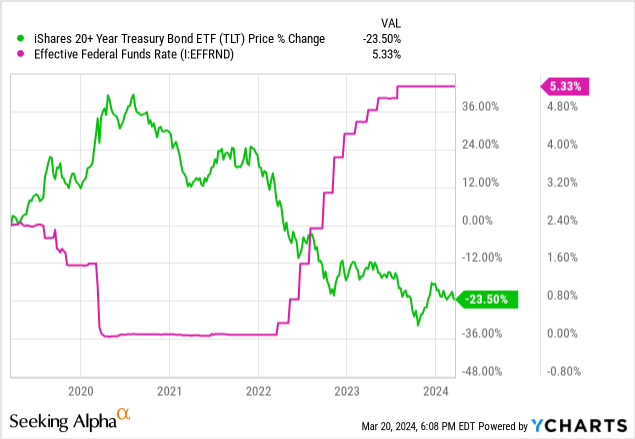

That may take the efficient price down from 5.25 – 5.5% to 4.5% – 4.75%. This sort of lower would push lengthy bonds up fairly a bit. With a length of 16.5 years, funds just like the iShares 20+ 12 months Treasury Bond ETF (TLT) stand to realize virtually 20% in worth if all goes in line with the Fed’s plan.

This restoration might be welcome for long-term holders and presents a shopping for alternative within the current.

Dovish Confidence On Inflation

The Fed’s main focus for this cycle has been on inflation, and till now, they’ve used the phrase “totality of knowledge” to explain the necessity for extra than simply good CPI readings to justify decreasing charges.

At Wednesday’s assembly, Powell’s tone modified. Powell appeared way more assured in regards to the Fed’s capability to curb inflation, rebutting a query about larger CPI and PCE readings:

I believe [the higher CPI and PCE readings] have not actually modified the general story, which is that of inflation shifting down steadily on a generally bumpy highway towards 2%…We’re not going to overreact to those two months of knowledge, nor are we going to disregard them.

To indicate his confidence, Powell evoked the markets by predicting that the Fed would attain its 2% inflation purpose.

The markets consider that we’ll [get inflation to 2% p.a.]. They need to consider that, as a result of we’ll obtain that purpose.

No matter what the markets are pricing in, the Fed guarantees to nonetheless base their choices on knowledge however is making it clear that they would wish notably unhealthy knowledge to steer them from this course.

The opposite factor is, within the second half of the yr, you had some fairly low readings, so it could be tougher to make that 12 month window ahead…Nonetheless, we’re searching for knowledge that affirm the low readings that we had final yr…And provides us a better diploma of confidence that what we noticed was actually inflation shifting sustainably right down to 2%.

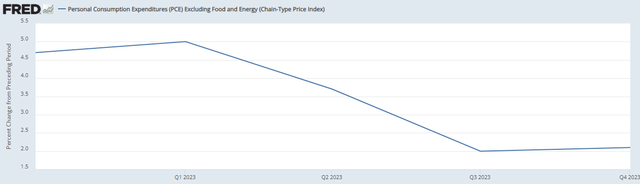

Once you have a look at one in all my most popular inflation metrics, “sticky CPI,” which is CPI much less meals and vitality, you see a compelling story that lends to their credibility.

Determine 4 (FRED)

This downtrend can also be seen in private consumption expenditures (“PCE”) index. This tells us that customers are spending much less, which is a disinflationary strain.

Determine 5 (FRED)

Watch The Labor Market

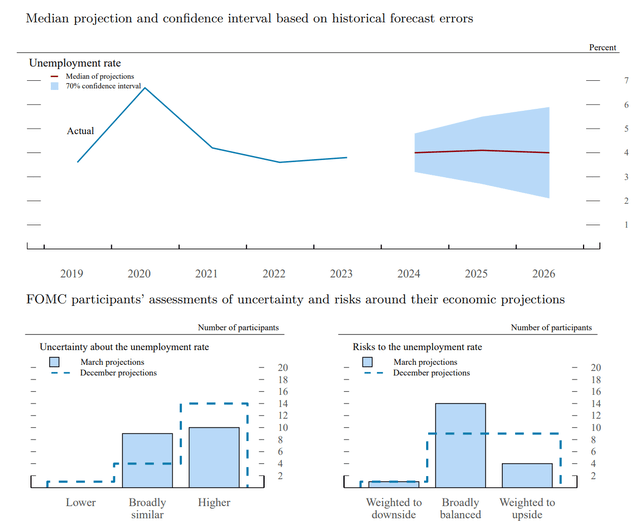

That is the one place the place Powell appeared somewhat extra hawkish on, the labor market. He said outright that unhealthy labor knowledge would hinder his plan to chop charges, however {that a} weakening within the labor market is unlikely within the Fed’s view.

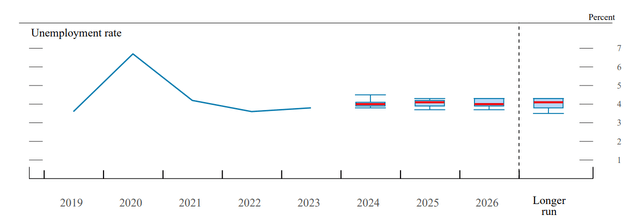

Proper now, the Fed tasks a 4% unemployment price shifting ahead, in keeping with the place we’re as we speak.

Determine 6 (FOMC)

That is the “pure price” of unemployment within the US, kind of, and the Fed tasks gradual shifts across the 4% mark for the following few years.

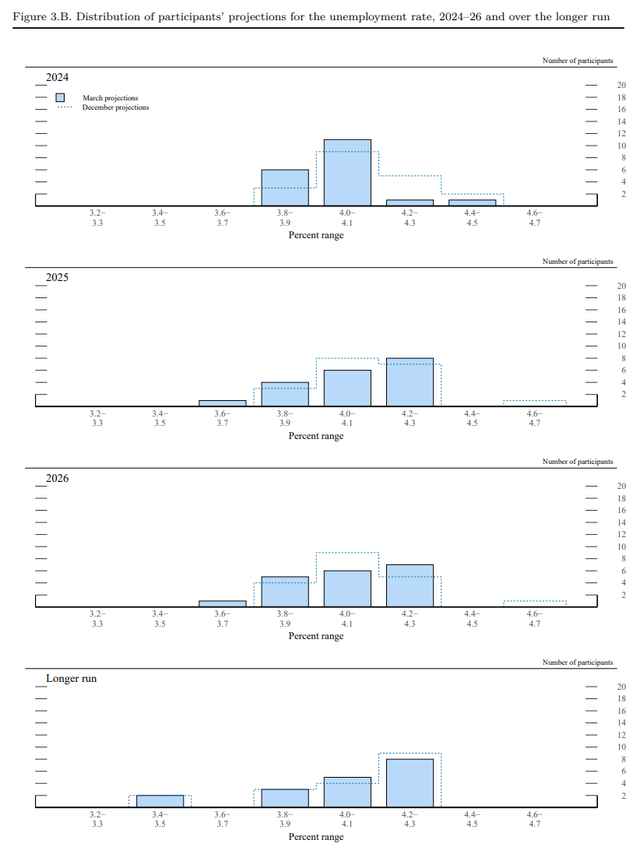

Be aware within the subsequent chart the place the dotted traces are. These are the projections from December’s assembly, and the stable bars are the present, revised projections.

Determine 7 (FOMC)

There may be much less uncertainty in regards to the labor market inside the FOMC, which is an efficient signal, and has actually led to Powell’s even-more dovish tone.

Determine 8 (FOMC)

The chart above exhibits how since December, FOMC members have turn into extra sure in regards to the unemployment price shifting ahead. This can be a good signal, as Powell has stated that the labor market is a driving issue within the FOMC’s resolution making concerning price steerage.

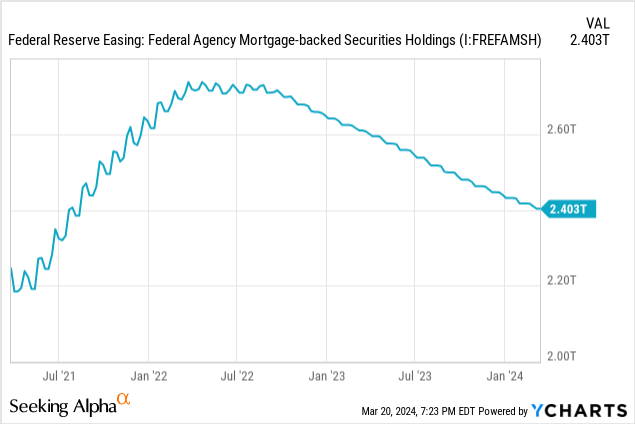

Do not Drown In The Runoff

Lastly, we have to discuss in regards to the Fed’s steadiness sheet. They maintain a variety of agency-backed mortgages and US Treasury bonds that they’ve been letting run off since their rate-hiking started.

[The] committee will proceed lowering its holdings of Treasury securities, company debt, and company mortgage-backed securities…

Powell later confirmed that together with price cuts, the Fed plans to gradual this run-off.

The final sense of the committee is that it will likely be applicable to gradual the tempo of run-off pretty quickly, according to the plans we have beforehand issued…

This can be a potential boon for bonds, because the Fed’s run-off has pushed down demand for the aforementioned securities. That is finest seen within the Fed’s ABS holdings.

If this eases and the Fed ranges its steadiness sheet off, we may see a stabilization within the treasury market. This could possibly be a catalyst for a help degree. Up to now, the Fed has used this steadiness sheet to inflate bond demand, elevating costs and decreasing yields. This can be a software that the Fed may deploy once more now that they’ve let the run-off take its course.

What’s The Commerce?

There are just a few trades I might take into account presently, given this new data.

- The Lengthy Period Play

- 20+yr bond funds like TLT are the way in which to go to benefit from falling charges as their costs rise essentially the most when charges fall.

- Buyers may be interested by Simplify’s tackle the length commerce, TUA & TYA, which I wrote about briefly right here. This can be a leveraged ETF, buyers beware!

- The Fastened Charge Play

- We all know that charges will change within the subsequent 9 months, and certain decrease. Which means that now could be the right time to lock in charges on CDs or different cash-like devices that provide fastened charges for lengthy durations of time.

- Newly-issued mortgages are providing unbelievable charges. Simplify’s MTBA invests solely in these excessive yielding mortgages, that are sometimes fixed-rates. This eliminates the decrease yielding “fluff” within the index.

- It’s time to slowly transfer out of T-Payments over the following 9 months, shifting over to longer timelines.

In December’s article, I wrote about how I have been holding each funding grade company bonds through LQD and intermediate treasuries through IEF. I’m nonetheless holding these, though I’ve moved my IEF publicity to TUA and TYA. I nonetheless advocate these for the foreseeable future as nicely, probably till we see the primary price hike.

I count on that to return in June, however it could come eventually given massive shifts in financial knowledge. Charge cuts in June, August, and November make sense to me, as it should give the Fed time between every announcement to observe the info. Usually, the Fed likes to lag a month between adjustments in charges.

Conclusion

The Fed has spoken and Powell appeared much more dovish than earlier than. This can be a good signal and may be very bullish for the bond market. Whereas we will count on price cuts coming this yr, Powell made it very clear that it’s depending on continued good knowledge.

For now, crucial indicators to observe appear to be inflation and unemployment, with the Fed giving CPI and PCE metrics some respiratory room and calling a pure 4% unemployment that ought to persist for the following few years.

To that finish, I’m recommending buyers enhance their length in anticipation of those price cuts. Additionally it is prudent to start locking in high-yield fastened charges like CDs, particular person treasury bonds, and different timed deposits.

I’m nonetheless recommending buyers take into account funding grade company bonds and intermediate-term treasuries within the present market and proceed to consider of their outperformance over the combination bond market.

Thanks for studying.

{kind=link}