Hinterhaus Productions

The Pioneer Excessive Earnings Fund, Inc. (NYSE:PHT) is a closed-end fund, or CEF, that income-focused buyers should buy in pursuit of their targets. As is often the case with closed-end bond funds, the Pioneer Excessive Earnings Fund has a fairly enticing yield. Not less than, its yield could be very affordable in comparison with the extremely low bond yields that buyers and savers have needed to put up with over many of the twenty first century. As of the time of writing, this fund yields 8.96%. Right here is how that compares to a few of its friends:

|

Fund Identify |

Morningstar Classification |

Present Yield |

|

Pioneer Excessive Earnings Fund |

Mounted Earnings-Taxable-Excessive Yield |

8.96% |

|

Allspring Earnings Alternatives Fund (EAD) |

Mounted Earnings-Taxable-Excessive Yield |

9.81% |

|

BNY Mellon Excessive Yield Methods Fund (DHF) |

Mounted Earnings-Taxable-Excessive Yield |

9.13% |

|

BlackRock Company Excessive Yield Methods Fund (HYT) |

Mounted Earnings-Taxable-Excessive Yield |

9.90% |

|

Neuberger Berman Excessive Yield Methods Fund (NHS) |

Mounted Earnings-Taxable-Excessive Yield |

13.66% |

|

PGIM Excessive Yield Bond Fund (ISD) |

Mounted Earnings-Taxable-Excessive Yield |

10.29% |

|

Western Asset Excessive Earnings Alternative Fund (HIO) |

Mounted Earnings-Taxable-Excessive Yield |

11.41% |

As we will instantly see, the Pioneer Excessive Earnings Fund just isn’t the highest-yielding fund within the house. This isn’t essentially a nasty signal, as outsized yields generally are typically an indication that the market believes {that a} fund is participating in unsustainable actions. A typical instance for a closed-end fund can be the distribution of monies far exceeding the precise funding earnings which are earned by the portfolio. A yield that’s considerably decrease than its friends doesn’t essentially imply that the fund is safer than different funds in the identical class, although, so we must always not have a look at yield alone. With that mentioned, income-focused buyers do often contemplate a fund’s yield as one issue of their evaluation, and this one clearly doesn’t look fairly pretty much as good as its friends.

As common readers can doubtless bear in mind, we beforehand mentioned the Pioneer Excessive Earnings Fund in August 2023. The bond market atmosphere on the time was similar to the one which we have now right this moment as buyers started to imagine that the Federal Reserve was in no hurry to scale back charges and that it could preserve them at ranges far exceeding these of the “free cash” period that dominated most of this century’s monetary panorama. As such, bond costs have been quickly declining and bond yields rose. There was a interval in late 2023 by which the alternative occurred, and buyers started to cost in a major diploma of rate of interest cuts in 2024. Nonetheless, the market is now not anticipating far more than fifty foundation factors of rate of interest cuts by December and the bond market has declined up to now this yr. As such, we will most likely assume that the fund’s efficiency for the reason that date of our prior dialogue has been comparatively flat. Nonetheless, that has not been the case, as shares of the Pioneer Excessive Earnings Fund have appreciated by 6.74% since that date:

Searching for Alpha

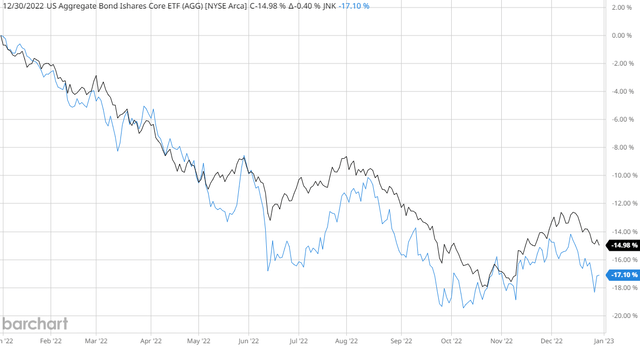

As we will clearly see from the chart above, this fund’s share worth has carried out a lot better than both the Bloomberg U.S. Combination Bond Index (AGG) or the Bloomberg Excessive Yield Very Liquid Index (JNK) that tracks junk bonds. Of the 2 indices, the junk bond index is a greater benchmark for this fund, because the Pioneer Excessive Earnings Fund additionally invests in high-yield bonds. The curious factor right here is that the junk bond index has really outperformed investment-grade company and sovereign points over the intervening interval. We might ordinarily anticipate junk bonds to say no extra quickly than investment-grade bonds throughout a time period by which long-term rates of interest are rising. For instance, that’s what occurred again in 2022:

Barchart

That is being pushed by the yield premium that’s demanded by buyers for taking over the upper default danger of junk bonds being decrease than it was again in August. In brief, the yield of junk bonds is nearer to that of investment-grade bonds than it was eight months in the past. It’s unsure how lengthy it will final, and it’s a very actual danger for anybody who buys the Pioneer Excessive Earnings Fund right this moment. In any case, any enlargement of the yield premium will trigger the fund’s internet asset worth to say no until all yields start falling (which is unlikely within the close to time period as a result of feedback made by Chairman Powell of the Federal Reserve earlier this week). That occasion would trigger the fund’s share worth to say no and hand losses to buyers buying at right this moment’s degree.

As I’ve identified in varied earlier articles, the share worth efficiency of a closed-end fund doesn’t essentially inform us how nicely buyers in a given fund really did. It is because funds such because the Pioneer Excessive Earnings Fund distribute most or all of their funding earnings to their shareholders. The essential enterprise mannequin is to maintain the scale of the portfolio comparatively steady whereas giving the buyers all of the earnings earned by mentioned portfolio. That is the explanation why these funds are likely to have larger yields than absolutely anything else available in the market. The distribution additionally offers an actual return that ends in the buyers really doing a lot better than the share worth efficiency alone would recommend.

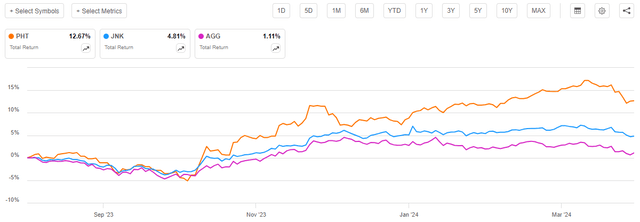

As such, we must always take the fund’s distributions into consideration in any evaluation of its efficiency. After we do this, we see that buyers within the Pioneer Excessive Earnings Fund have benefited from a 12.67% achieve for the reason that date that my earlier article on this fund was printed:

Searching for Alpha

As we will see, the inclusion of the coupon funds and distributions paid out by each the Pioneer Excessive Earnings Fund and each index funds was adequate to offset the losses that buyers suffered from the worth decline of investment-grade bonds. That is good, however clearly, no bond has come wherever near beating widespread shares. That’s the normal state of affairs, although, and as such we must always not fear an excessive amount of. In any case, no one invests in bonds as a result of they anticipate to beat widespread shares. In fact, within the quick time period, there could possibly be some causes to anticipate that bonds will outperform widespread shares. Specifically, a few of the largest shares within the S&P 500 Index (SP500) proper now have considerably stretched valuations that can take a number of a long time for the businesses in query to develop. Rising bond yields may make them extra enticing than ready for an prolonged interval for a corporation’s earnings to develop into its valuation.

As we will see from the charts above, the current efficiency of the Pioneer Excessive Earnings Fund has been good relative to its indices. This sturdy efficiency will nearly definitely be enticing to buyers, together with these whose major aims revolve across the technology of revenue. Nonetheless, previous efficiency isn’t any assure of future outcomes, so allow us to check out this fund’s holdings and monetary scenario right this moment in an try to find out the place it’ll go from right here.

About The Fund

The Pioneer closed-end funds are comparatively uncommon in that they don’t have a devoted web site. This fund isn’t any exception as the one factor that the fund sponsor offers is an internet site that exhibits all of the funds within the household in addition to offers some documentation for every respective fund. Happily, the fund’s truth sheet, which may be downloaded from that web site offers an outline of the fund’s technique and aims. Here’s what the actual fact sheet states:

Pioneer Excessive Earnings Fund, Inc. is a closed-end fund that invests for a excessive degree of present revenue by investing in a portfolio of below-investment-grade bonds and convertible securities. It additionally seeks capital appreciation as a secondary goal.

The rest of the outline is just a disclaimer outlining the assorted dangers of investing in a junk bond fund. I believe that the majority people who’re studying this are nicely conscious of the potential for default-related losses, market-driven declines, and comparable dangers, so I cannot waste house copying the remainder of the fund’s description. It may be freely considered within the downloadable truth sheet in any case. The one actual factor of significance that’s talked about within the disclaimer that could possibly be comparatively uncommon or stunning is that the fund can make investments as much as half of its belongings in illiquid securities which may be troublesome to eliminate. As these securities are usually not traded on any trade, it may be troublesome to worth them in addition to to acquire an applicable worth given their traits and the issuing entity’s fundamentals. This could possibly be a possible concern for potential buyers because it ends in the fund’s reported internet asset worth doubtlessly being uncovered to errors. In any case, simply because the fund’s managers or auditors say that an asset has a selected worth doesn’t imply that it may really be bought at that worth.

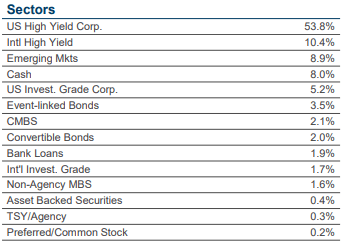

Whereas the fund’s documentation states that it may possibly have as much as half of its belongings invested into illiquid securities, the actual fact sheet doesn’t state what share of its belongings are at the moment invested in such securities. The one asset allocation that it offers is that this:

Fund Reality Sheet

The fund’s semi-annual report is equally opaque. It repeats the actual fact sheet’s assertion that as much as half of its belongings could be invested in these securities, nevertheless it doesn’t outright state what share of complete belongings the fund at the moment has invested in such securities. Reasonably, the semi-annual report offers the next asset allocation:

|

Asset Kind |

Proportion of Whole Holdings |

|

Senior Secured Floating-Fee Mortgage Pursuits |

4.2% |

|

Widespread Inventory |

0.3% |

|

Collateralized Mortgage Obligations |

2.4% |

|

Business Mortgage-Backed Securities |

3.5% |

|

Convertible Company Bonds |

2.5% |

|

Company Bonds |

119.7% |

|

Convertible Most well-liked Inventory |

0.4% |

|

Insurance coverage-Linked Securities |

6.2% |

|

Overseas Authorities Bonds |

0.1% |

|

U.S. Authorities and Company Obligations |

5.3% |

|

Brief-Time period Investments |

1.8% |

The international authorities bonds are obligations of the Russian Federation, which could appeal to some concern from American or European buyers. In any case, that nation has been the goal of financial sanctions for some time now. These sanctions may, in truth, be inflicting this asset to be illiquid and principally power the fund to easily maintain on to it. It’s a tiny proportion of the fund’s complete belongings in any case, and as such, we most likely don’t want to fret about it.

There could be some eagle-eyed readers who discover that a few of the asset allocation figures offered within the semi-annual report differ from the actual fact sheet’s statements. The semi-annual report offers a full accounting of all of the belongings that have been held by the fund on September 30, 2023. The actual fact sheet offers a abstract of its holdings on February 29, 2024. As such, the actual fact sheet is the newer doc and is due to this fact extra authoritative in areas by which the 2 paperwork differ. Nonetheless, the Pioneer Excessive Earnings Fund solely has a 24% annual turnover, so its belongings won’t be altering that always. As such, there could possibly be a spot for each info sources in figuring out what this fund at the moment holds in its portfolio.

The essential takeaway, although, is that it doesn’t seem that the fund is offering a concrete determine for the share of its portfolio that’s at the moment invested in illiquid securities. As such, it’s unsure how correct the fund’s reported internet asset worth really is, because it won’t have the ability to really promote all the pieces in its portfolio on the worth that it claims in an emergency. Because of this, as buyers, we can’t be utterly sure how applicable the worth that we pay for the fund’s shares is given its underlying belongings. Any potential investor ought to preserve this in thoughts when contemplating buying shares of the fund.

The asset allocation information that’s offered in each the fund’s truth sheet and its semi-annual report state that the fund is primarily invested in high-yield company bonds, that are colloquially known as “junk bonds.” These bonds are so named as a result of they’ve a a lot larger danger of default than abnormal investment-grade bonds. As such, buyers demand a a lot larger price of curiosity than can be required from investment-grade company or sovereign bonds as compensation for the elevated danger of default. Traditionally, this premium has ranged from 4% to six% relying on the concern issue and normal willingness of market members to tackle danger. This may ordinarily recommend that these bonds ought to decline together with investment-grade bonds to keep up that historic premium. Nonetheless, apparently, junk bonds have been outperforming authorities bonds year-to-date:

This chart exhibits the iShares 7-10 12 months Treasury Bond ETF (IEF) towards the junk bond SPDR over the year-to-date interval:

Searching for Alpha

That is very fascinating because it means that up to now this yr, buyers have been extra keen to carry junk bonds than medium-term U.S. Treasury securities. Mainly, the yield premium of junk bonds has been narrowing. Admittedly, this might additionally recommend a decreased willingness of buyers to carry longer-dated bonds because the junk bond index has a 4.93-year common time to maturity, which is a bit lower than the treasury bond fund. Brief-term (1–3-year Treasuries) have held up higher than junk bonds over the identical interval. Nonetheless, check out the iShares 3-7 12 months Treasury Bond ETF (IEI) over the year-to-date interval:

Searching for Alpha

As soon as once more, we see that junk bonds are holding up higher than U.S. Treasury securities of comparable time till maturity. This as soon as once more means that the yield premium is lowering. It’s doable that that is being attributable to perceptions of U.S. Treasury security proper now, as QTR identified on the Fringe Finance Substack:

Now it’s unfair to annualize this as a result of there’s some lumpiness within the month-to-month information; nevertheless, with three hundred and sixty five days in a yr this suggests a deficit of $3.65 Trillion/yr. Within the first Federal quarter that ended December 31, 2023, the deficit was $500 Billion implying a $2.0 Trillion annual deficit. Q2, which ended March 3, was simply reported, and the deficit was $600 Billion. For the primary half of fiscal 2024 the U.S. Federal Authorities recorded a $1.1 Trillion greenback deficit. Clearly, the present run price is way larger.

Remember that that is all with a comparatively wholesome economic system and inventory market. If the debt have been to proceed to develop at this price, it could be similar to a beginning debt of $34 Trillion on December 31, 2023. It (a deficit run price of $3.65T) would suggest an annualized progress price of 10.7% within the complete debt burden. Annual debt progress of 10.7% compares very unfavorably to estimated GDP progress of two.0-2.5%. GDP funds the curiosity funds on the debt and that is why the maths is unrelenting. One thing has to offer. And by the best way, the pattern in this doesn’t look good, the Biden Administration simply proposed a spending funds of $7.3 Trillion for fiscal 2025, which represents a 13% improve in spending. Remember that tax revenues in fiscal 2023 have been solely $4.4 Trillion. The place are they going to seek out the cash?

Thus, it’s doable that at the very least some portion of the obvious narrowing of the junk bond danger premium is being attributable to buyers re-evaluating their earlier assumptions of U.S. Treasury debt as risk-free. If that debt is riskier than was beforehand believed, then it solely is smart that such re-evaluation would trigger it to underperform junk bonds which have all the time been thought of to be very dangerous belongings. Nonetheless, junk bonds nonetheless usually pay their coupons in U.S. {dollars} and plenty of have an inherent hyperlink to the American economic system. As such, there’s a danger right here that the danger premium compression will reverse and return to its historic ranges. In such an occasion, anybody shopping for junk bonds, or a junk bond fund, right this moment may endure some worth declines.

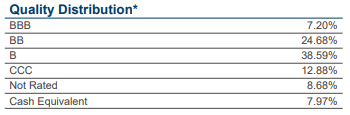

A have a look at the credit score scores of the securities within the fund’s portfolio exhibits that the danger of default-related losses shouldn’t be too dangerous:

Fund Reality Sheet

An investment-grade safety is something rated BBB or larger, in addition to cash-equivalent securities. As we will instantly see, that accounts for 15.17% of the fund’s complete belongings. That is clearly a minority, however it’s nonetheless larger than many different junk bond funds possess. Specifically, the fund’s money place is way larger than most funds possess.

Up to now, that will have been an unacceptable drag on a fund’s efficiency. Money has really outperformed most bonds up to now this yr as a result of it has not declined, and cash market funds are literally offering affordable yields. Nonetheless, we will nonetheless see that 76.15% of the fund’s belongings are invested in speculative-grade securities. The proportion could be larger than this, because it appears doubtless that the 8.68% weighting to unrated securities additionally consists of speculative-grade securities. In any case, just about any entity that’s able to getting an investment-grade credit standing will most likely undergo the time and expense to take action as a result of that can reserve it a considerable sum of money on curiosity funds over time.

As such, we will assume that 84.83% of the fund’s belongings are invested in junk debt. That is really decrease than we might anticipate from a junk bond fund, however it’s definitely larger than a extremely risk-averse investor may want.

Nonetheless, we will see that 63.27% of the fund’s belongings are invested in securities that carry both a BB or a B credit standing. These are the 2 highest doable scores for speculative-grade debt. Based on the official bond score scale, entities that may situation bonds with these two scores have adequate monetary power to deal with all of their present debt and will have the ability to proceed to take action even within the occasion of a short-term financial shock. Their steadiness sheets are usually not almost as sturdy as an investment-grade entity, however the total default danger ought to not likely be too excessive. That could possibly be a supply of consolation when mixed with the truth that the fund’s portfolio contains securities from 289 distinctive issuers. In any case, the excessive variety of issuers implies that each single issuer solely accounts for a small share of the portfolio, and thus a single default mustn’t have a noticeable influence on the portfolio as a complete.

The most important danger right here is that many corporations will default , however that typically solely occurs when the economic system is going through some form of disaster. In such conditions, most of us may have larger issues to fret about than some losses in a given bond fund in our portfolios. As such, we will see that we most likely don’t have to fret an excessive amount of about shedding cash as a result of defaults. The most important danger right here is that junk bonds will decline in worth as a result of both rates of interest remaining excessive for an prolonged interval or the at the moment compressed danger premium returning to common ranges.

Leverage

As is the case with most closed-end funds, the Pioneer Excessive Earnings Fund employs leverage as a way of boosting the efficient yield that it receives from the belongings in its portfolio. I defined how this works in my earlier article on this fund:

In brief, the fund is borrowing cash and utilizing that borrowed cash to buy junk bonds and comparable belongings. So long as the bought belongings have the next yield than the rate of interest that the fund has to pay on the borrowed cash, the technique works fairly nicely to spice up the efficient yield of the portfolio. This fund is able to borrowing cash at institutional charges, that are significantly decrease than retail charges. As such, it will often be the case. Nonetheless, it is very important be aware that this technique just isn’t as efficient right this moment with charges at 6% because it was three years in the past when charges have been primarily 0%. It is because the distinction between the speed at which the fund can borrow and the yield on the bought securities is way narrower than it as soon as was.

As of the time of writing, the Pioneer Excessive Earnings Fund has leveraged belongings comprising 31.50% of its portfolio. This represents an enchancment over the 32.07% leverage ratio that the fund had on the time of our earlier dialogue. Nonetheless, neither ratio is very dangerous, as I typically contemplate something underneath a 3rd of belongings to symbolize an affordable steadiness between the dangers and the potential rewards of utilizing leverage.

Right here is how this fund’s leverage compares to that of its friends:

|

Fund Identify |

Leverage Ratio |

|

Pioneer Excessive Earnings Fund |

31.50% |

|

Allspring Earnings Alternatives Fund |

30.30% |

|

BNY Mellon Excessive Yield Methods Fund |

28.78% |

|

BlackRock Company Excessive Yield Methods Fund |

25.61% |

|

Neuberger Berman Excessive Yield Methods Fund |

30.10% |

|

PGIM Excessive Yield Bond Fund |

20.74% |

|

Western Asset Excessive Earnings Alternative Fund |

0.00% |

(all figures from CEF Knowledge.)

As we will clearly see, not one of the funds that spend money on junk bonds are notably extremely leveraged. Not less than, they don’t seem to be anymore as a number of of them did use pretty important ranges of leverage again when rates of interest have been at 0%, and shopping for bonds with substantial quantities of leverage was the one technique to earn an affordable yield from a junk bond portfolio. The Pioneer Excessive Earnings Fund does have the best leverage right here, which might ordinarily recommend that the fund is taking over extreme quantities of danger relative to its friends. Nonetheless, in fact, the distinction between this fund’s leverage and that of its friends just isn’t very nice, so we will overlook it. General, it does seem that the Pioneer Excessive Earnings Fund is hanging an affordable degree of steadiness between the danger and the potential rewards of utilizing leverage.

Distribution Evaluation

As talked about earlier on this article, the first funding goal of the Pioneer Excessive Earnings Fund is to supply its buyers with a really excessive degree of present revenue. This is smart given the fund’s technique of investing its belongings in junk-rated bonds and comparable belongings as a result of these securities ship the majority of their complete returns within the type of direct funds to their buyers. The fund collects the coupons that it receives from these securities and combines them with any buying and selling earnings that it manages to earn by exploiting the bond worth actions that accompany adjustments in rates of interest.

This fund then takes issues a step additional by borrowing cash and utilizing that cash to buy and obtain coupon funds from extra bonds than it may management just by counting on its fairness capital. In the end, the fund distributes all of this cash to its shareholders, internet of its personal bills. After we contemplate the truth that bond costs are at the moment affordable for the primary time in a technology, we will anticipate that this enterprise mannequin would offer the fund’s shares with a really enticing yield.

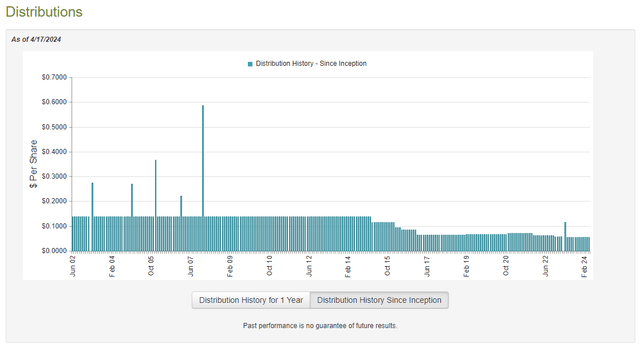

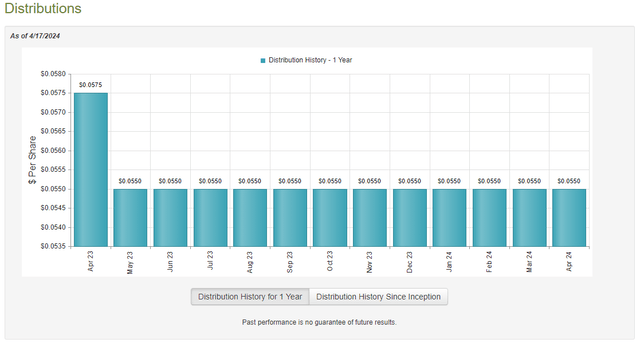

That is certainly the case, because the Pioneer Excessive Earnings Fund pays a month-to-month distribution of $0.0550 per share ($0.66 per share yearly), which supplies it an 8.96% yield on the present share worth. As we noticed within the introduction to this text, this yield is barely decrease than that of lots of the fund’s friends, however it’s not totally out of line with the sector. Nonetheless, this fund has not been notably constant concerning its distributions through the years. The truth is, the fund has each raised and lowered its distribution a number of instances since its inception:

CEF Join

The current pattern, sadly, has been for the fund to chop its distribution, and it’s at the moment a lot decrease than the $0.1375 per share month-to-month distribution that the fund had a decade in the past. The latest distribution reduce got here final Could, when the fund decreased its month-to-month distribution from $0.0575 per share to $0.0550 per share:

CEF Join

That is one thing which will turn into a turn-off for these buyers who’re in search of to earn a secure and constant revenue from the belongings of their portfolio. This can be a group that features many retirees in addition to these people who’re attempting to complement their salaries with some funding revenue in right this moment’s inflationary atmosphere. Talking of an inflationary atmosphere, a distribution discount is the very last thing that we actually wish to see as a result of we want larger incomes to keep up a sure way of life than we did just a few years in the past. The truth that this fund has been chopping its distribution has the alternative impact.

Nonetheless, as I’ve identified previously, the fund’s distribution historical past just isn’t essentially an important factor for an investor right this moment. It is because anybody who purchases the fund’s shares right this moment will obtain the present distribution on the present yield. This particular person won’t be adversely affected by occasions that occurred previously. As such, we must always check out the fund’s funds to see how nicely it may possibly maintain its present distribution.

Sadly, we don’t have a very current doc that we will seek the advice of for the needs of our evaluation. As of the time of writing, the newest monetary report for the Pioneer Excessive Earnings Fund is the semi-annual report that corresponds to the six-month interval that ended on September 30, 2023. As such, this report will embody no details about the fund’s efficiency over the previous seven months. That is disappointing, as there have been a number of issues that occurred throughout the intervening interval, together with each the epic bond market rally within the remaining two months of final yr and the decline in bond costs that we have now seen this yr.

Because the monetary report ends earlier than both of those occasions occurred, we have now no method of realizing how nicely the fund carried out in both of them. Nonetheless, it does embody at the very least a part of the summer season and autumn of 2023, which was a bear marketplace for junk bonds. Throughout that interval, we typically noticed rising yields and falling bond costs. That would have brought about this fund to take some realized or unrealized losses. Additionally it is extra indicative of the standard of a fund’s administration and the way it performs throughout a difficult interval than a bull market. In any case, anybody can make cash when the worth of each asset available in the market is rising.

For the six-month interval that ended on September 30, 2023, the Pioneer Excessive Earnings Fund acquired $13,875,751 in curiosity and $487,487 in dividends (internet of international withholding taxes) from the belongings in its portfolio. This offers the fund a complete funding revenue of $14,363,238 for the interval. The fund paid its bills out of this quantity, which left it with $9,689,018 out there for shareholders.

This was, sadly, not adequate to cowl the $9,756,094 that the fund paid out in distributions throughout the interval. Nonetheless, it did handle to get very shut to completely masking its distribution out of internet funding revenue. We might ordinarily want {that a} fixed-income fund merely pay out its internet funding revenue to the buyers, so it is a good signal, though it could be preferable if its internet funding revenue have been barely larger.

With that mentioned, there are different strategies by which a fund can get hold of the cash that it requires to cowl its distributions to the shareholders. For instance, it would have the ability to earn some cash by the sale of bonds that go up in worth when rates of interest decline. These are realized capital beneficial properties and are due to this fact not included in internet funding revenue for tax or accounting functions. Nonetheless, they clearly do symbolize cash coming right into a fund that may be paid out to the buyers.

Happily, this fund managed to do okay right here. It reported internet realized losses of $6,956,242, however this was absolutely offset by $8,587,838 internet unrealized beneficial properties. General, the fund’s internet belongings elevated by $1,564,520 after accounting for all inflows and outflows within the interval. Because the fund’s internet belongings elevated, it absolutely coated all of its payouts throughout the interval.

That is most likely sustainable going ahead. As we will see, the fund got here very shut to completely masking its distributions solely out of internet funding revenue. The fund really reduce its distribution part-way by the interval, so we will assume that its distribution payouts are a bit decrease now. Thus, assuming that the fund’s internet funding revenue remained steady, it must be absolutely paying the smaller distribution solely with its internet funding revenue. Bond coupons don’t change over time, so it’s most likely the case that its internet funding revenue is comparatively steady. As such, all the pieces might be okay right here.

Valuation

As of April 17, 2024 (the newest date for which information is out there as of the time of writing), the Pioneer Excessive Earnings Fund has a internet asset worth of $8.06 per share, however the shares at the moment commerce at $7.34 every. This offers the fund’s shares an 8.93% low cost to internet asset worth on the present worth. That is fairly a bit extra enticing than the 6.24% low cost that the fund’s shares have had on common over the previous month. Thus, the present worth appears excellent for those who want to add this fund to your portfolio.

Conclusion

General, the Pioneer Excessive Earnings Fund appears like a fairly good junk bond fund. There are solely two issues that I’ve right here, and certainly one of them will apply to any junk bond fund proper now. The priority that’s distinctive to this fund is that it may need a major share of its portfolio invested in illiquid securities that can not be quickly disposed of. As such, we have no idea how correct its said internet asset worth really is.

The second concern is that junk bonds could be overpriced as a result of they haven’t declined in worth as a lot as U.S. Treasury securities year-to-date. This might expose the Pioneer Excessive Earnings Fund to losses if the market corrects and permits the junk bond danger premium to return to historic ranges. General, although, Pioneer Excessive Earnings Fund, Inc. could possibly be an affordable technique to get an 8.96% yield right this moment.

{kind=link}