Electrical vehicles are right here to remain. nrqemi/iStock Editorial through Getty Photos

To know the worth of Piedmont Lithium (NASDAQ:PLL), you have to perceive the partnerships they’ve made.

Sayona Quebec (35% Piedmont) / Sayona Mining (14.4% Piedmont) [ASX:SYA] (OTCQB:SYAXF)

Following a strategic funding and offtake settlement in January 2021, Piedmont is a partial proprietor of Sayona Quebec and its guardian firm Sayona Mining. The Sayona/Piedmont JV is ready to begin producing lithium spodumene focus in Q1 2023 from their NAL operation, which could not come at a greater time. Lithium demand has hit all-time highs and is anticipated to remain elevated for the foreseeable future.

Sayona/Piedmont NAL mine (Sayona investor presentation)

For the NAL mine, manufacturing is forecast to be 120,000 tons for 2023, with yearly nameplate capability growing to round 180,000 tons. Pilbara Minerals [ASX:PLS] (OTCPK:PILBF) not too long ago offered 5000 tons of spodumene focus at US$7100/ton. So in 2023 alone, NAL lithium gross sales at these numbers can be $852 million.

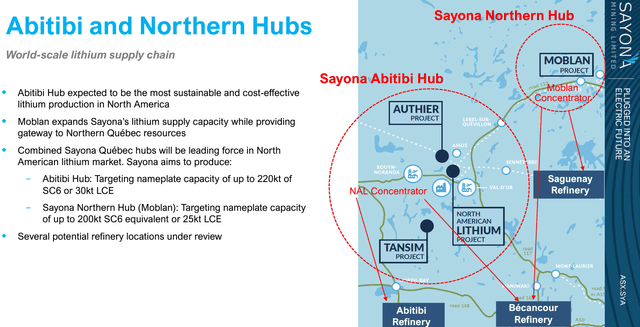

The JV intends to develop a further mine at Moblan, a deposit that’s at the moment present process a brand new drilling marketing campaign to broaden the useful resource. In parallel, the JV plans to construct a hydroxide refinery that will likely be fed from NAL and Moblan. The income from 2023 lithium gross sales will hold the JV nicely financed to execute these plans, which can enormously improve shareholder worth. See the company presentation right here.

Sayona/Piedmont JV tasks (Sayona investor presentation)

It has been a very long time since I wrote on Sayona Mining, however the premise that made me a believer in them nonetheless stands true. Administration: James Brown and Allan Buckler are administrators of Sayona Mining, and in addition the administrators of Altura Mining (now Morella). They introduced Altura from exploration stage to a completely operational lithium mine. They’re second to none for locating and growing lithium assets. Their expertise is priceless for Sayona and Piedmont.

Morella (Sayona 49%*) [ASX:1MC] (OTCPK:ALTAF)

Morella company was born out of the ashes of Altura Mining. As many know, Altura’s producing lithium mine was purchased out by Pilbara Minerals in 2021.

Altura Lithium Mine in 2020 (Altura Mining)

This was a tragic ending to an in any other case nice success story of bringing a tough rock lithium operation from exploration to manufacturing. The low spot value for lithium and financing issues led to their downfall.

Now, Morella is a lithium exploration firm as soon as once more, and have entered into an earn-in settlement with Sayona Mining to earn 51% curiosity in Sayona’s huge (1095sq km) Australian tenements positioned in prime lithium districts.

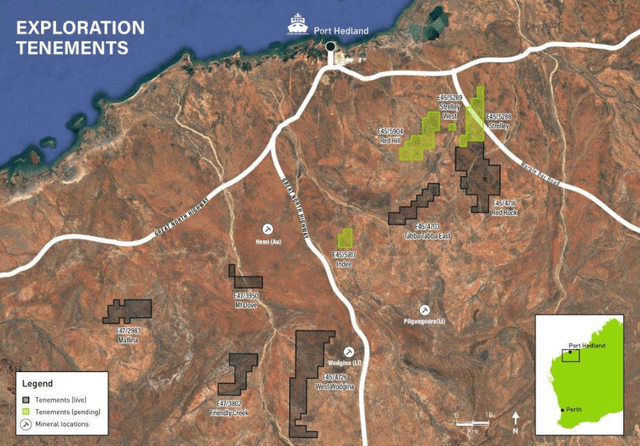

Morella Earn-in Tenements (Altura ASX announcement)

From the announcement, “Sayona will retain the remaining venture curiosity in addition to the appropriate to contribute to venture analysis and growth sooner or later.” *This can be a key piece of data. Sayona will possible assist be an offtake/finance associate for Morella within the case they uncover a lithium useful resource.

With associate Sayona, and by extension Piedmont, Morella could have the monetary and offtake help to develop into a producing mine, with possession shared between Piedmont, Sayona, and Morella. All Morella has to do now could be uncover a lithium useful resource, and there’s no higher administration workforce to do this. Some promising exploration bulletins may be seen right here, and right here.

Their company presentation may be seen right here.

Atlantic Lithium (50% Piedmont**) (OTCQX:ALLIF)

By committing monetary assets and dealing along with their JV companions, Piedmont is making what may be inconceivable for a single firm, doable with two.

They partnered with Ghana-based Atlantic Lithium with a strategic funding and future financing in July, 2021. This deal enormously derisked Atlantic Lithium by offering wanted capital. Piedmont initially invested $15 million to accumulate a 9.47% fairness curiosity within the firm, **and to realize 50% curiosity within the venture, Piedmont will spend $17 million to fund ongoing exploration and a definitive feasibility examine, and a further $70 million to fund the development of the lithium mine.

If Piedmont fulfills these obligations, they’ll obtain 50% of the longer term spodumene gross sales income when Atlantic begins producing lithium, scheduled for 2024. It will present wanted money till Piedmont’s Tennessee lithium hydroxide plant comes on-line, at which period the Ghana spodumene will likely be used as feedstock for conversion to hydroxide, which instructions a a lot larger premium. Ultimately, each corporations win.

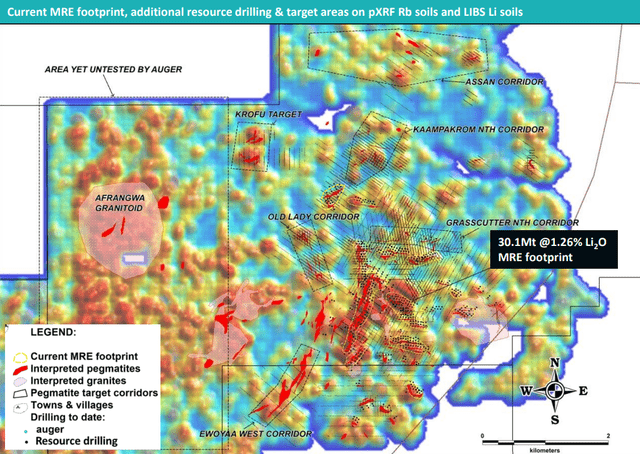

The JV continues to shock with wonderful drilling outcomes which can enhance venture economics. They’re on their strategy to delineating a a lot elevated useful resource, which already stands at a wholesome 30.1Mt @ 1.26% Li20.

Atlantic Lithium: Ghana useful resource drilling (Atlantic Lithium company presentation)

With Piedmont as their information, Atlantic will observe in NALs success. See their presentation right here.

Piedmont Lithium

Piedmont have realized that small lithium corporations are stronger collectively. Utilizing their technique of partnerships, and the close to time period money movement gained from excessive spodumene costs, their growth plan is derisked.

Piedmont growth schedule (Piedmont company presentation)

Altura had a completely practical laborious rock lithium mine producing spodumene focus. By bringing a lithium mine from idea to manufacturing, the board of administrators gained classes discovered and experience that can deliver the NAL mine to manufacturing, and to nameplate capability rapidly.

Piedmont will share on this success. When developing their lithium operations, they’ll have a blueprint to observe. It will show invaluable within the development and manufacturing of their Ghana lithium mine in 2024, and their very own Carolina lithium mine in 2025. In my thoughts, this derisks Piedmont, and units the stage for them to capitalize on excessive spodumene focus costs for the close to time period, and fund a lithium hydroxide plant that can intern unlock additional shareholder worth.

As a testomony to Piedmont and the important thing position they’ll play within the close to future, the U.S. Division of Vitality (“DOE”) awarded a $141.7 million grant to assist fund the Tennessee Lithium Hydroxide plant. America is lastly seeing the necessity for home manufacturing of battery-grade lithium hydroxide, which at the moment stands at solely 15ktpa. Piedmont, when absolutely operational, will produce 60ktpa, or 4x the overall present US output.

Money place

In response to their company presentation, Piedmont is in a really safe money place with US$118M within the financial institution. Upcoming income from NAL spodumene gross sales will add to this quantity in Q1 2023.

Dangers

Piedmont is a small-cap commodity inventory. Small-cap shares have market capitalizations between 300 million and a pair of billion. The large dangers with these shares are the lack of know-how obtainable, fluctuating commodity value, doable chapter, and low liquidity. Piedmont is at the moment a mining firm with none income. With out income, the corporate might resort to elevating capital through a rights subject, which can dilute their shares. That is unlikely as income from NAL ought to begin flowing beginning Q1, 2023.

Conclusion

Piedmont has all that’s required to develop into the centerpiece of the subsequent multinational lithium partnership. Some notable partnerships at present embody:

- Mineral Assets [ASX:MIN] (OTCPK:MALRF)/Albemarle (ALB)

- Jiangxi Ganfeng Lithium (OTCPK:GNENF)/Mineral Assets [ASX:MIN]

- SQM/Wesfarmers [ASX:WES] (OTCPK:WFAFY).

The market capitalization of those corporations begins at 10x that of Piedmont, which is a good signal for buyers.

Barron’s charges PLL as a “Purchase” primarily based on 7 analysts. The 12 month value forecast predicts a mean value of 105.61, representing a 79% improve from at present’s ranges ($59 at 11/3/22).

Within the lithium mining sector, generally you have to collaborate to succeed, and that’s exactly what Piedmont is doing.

{kind=link}